Author:区块律动

Key points summary

Michael Saylor is back to answer all of Natalie Brunell's questions—including those that most people wouldn't dare ask.

This podcast episode covers the following topics:

Why did Bitcoin fail to break $126K, and what do you think really happened?

Is price suppression truly present?

What is the biggest controversy surrounding Bitcoin?

Bitcoin was mentioned in the Epstein document.

Does quantum computing pose a real threat to the Bitcoin network?

Summary of key viewpoints

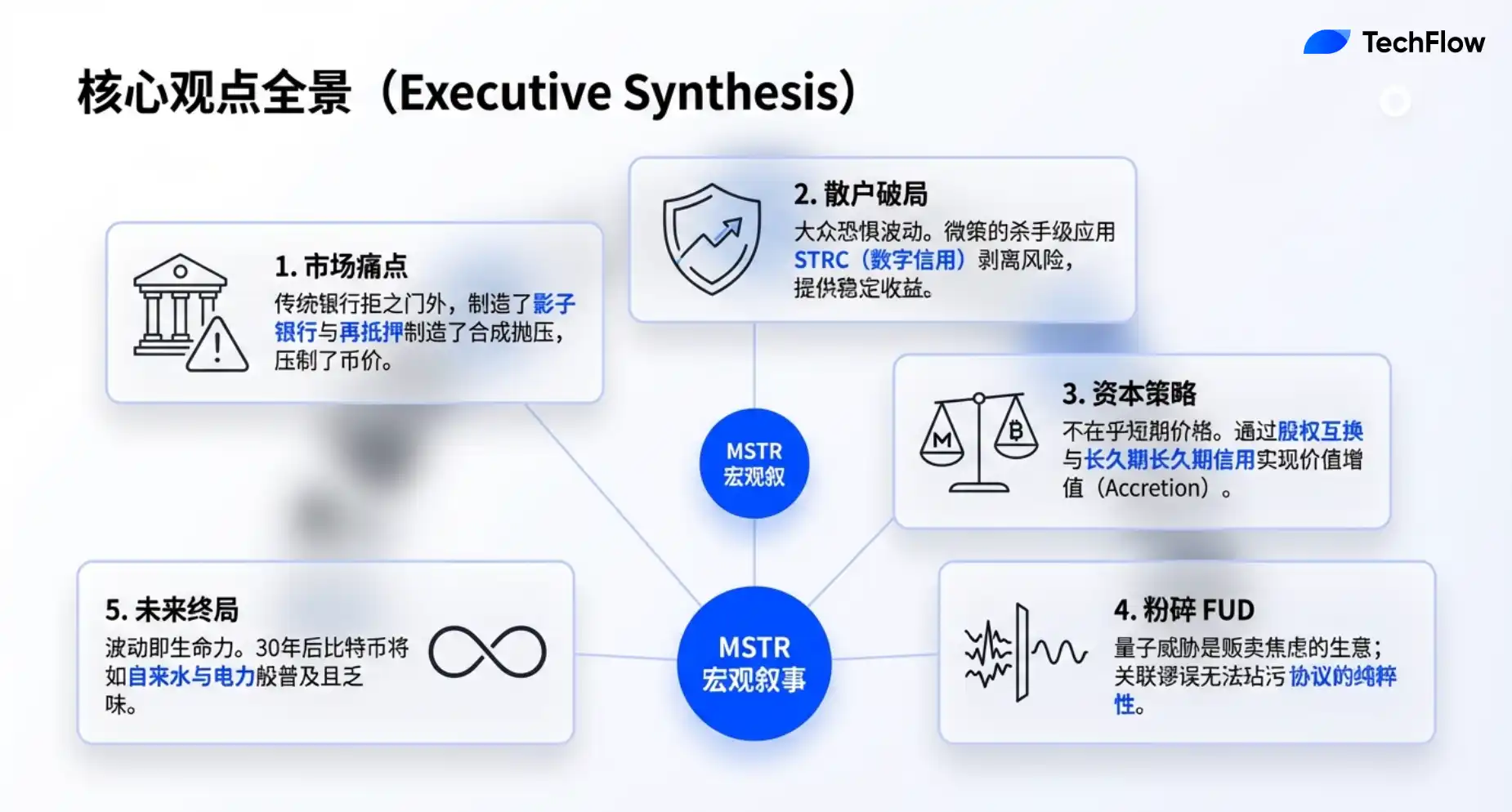

The Truth About Price Suppression: Shadow Banking and Re-mortgaging

Currently, approximately $1.8 trillion to $2 trillion worth of Bitcoin is held by retail or offshore investors, but they lack access to the traditional banking system and are forced into the shadow banking sector. The lack of a robust, non-recollateralized credit system suppresses the price of these assets.

What exactly is suppressing asset prices? I believe it's the lack of a complete, non-recollateralized credit system. Your $10 million worth of Bitcoin might be resold three or four times, which actually creates $30 to $40 million in selling pressure because shadow banks sell the assets you've pledged as collateral.

Why haven't retail investors entered the market: From "roller coaster" to "digital credit"

• Steadfast retail investors have already entered the market, and the way to attract mass investors is to offer digital credit products (such as STRC) that decouple volatility and provide stable returns.

What most retail investors want is something that's 2 to 4 times better than bond funds, or something like the S&P 500 without drawdowns. STRC strips away 80% to 90% of the risk and volatility of Bitcoin, giving investors a product with 4-5 times over-collateralization, double-digit returns, and tax-deferred features. This is a killer application for digital capital.

Commercialization process: 1,000 hours vs. 10 seconds

Bitcoin is evolving from a "tech enthusiast" stage to a "mass-market product" stage. The core of commercialization is to encapsulate complex technology into an extremely simple product experience.

Bitcoin is digital capital. I could spend a thousand hours explaining it to you, and you'd eventually understand, but you'd still have to endure a 45% crash. On the other hand, would you prefer a bank account with 11% interest and tax-deferred payments? Choose STRC. The former takes a thousand hours to explain, the latter only takes 10 seconds. The world doesn't need to read ten thousand pages of history; the world only needs products, like the iPhone.

Capital swap logic: Why is the cost of holding positions not important?

MicroStrategy invests in equity and long-term credit, not short-term loans. As long as the swap is "accretive," short-term price fluctuations will not have a substantial impact on the company.

Retail investors' only source of credit is "margin credit," which is credit available in one minute; if they're wrong, they're liquidated over the weekend. The credit we use, however, allows us to be wrong for 30 years. When exchanging equity for Bitcoin, the price doesn't matter; what matters is the premium or relative valuation you pay when you enter the trade. Our average cost doesn't make any substantial difference.

A Critique of "Doomsday Narratives": 99% of Narratives are Just Business

Crisis narratives surrounding Bitcoin (such as quantum threat and quantum FUD) are often commercial maneuvers that exploit panic for influence. Investors should maintain a constructive optimism.

99% of these narratives are just a business. If you insure against every tiny possibility, your income will eventually be completely depleted, leading to bankruptcy. The reality is, ten years from now, you might simply need to tap a "software update" on your iPhone to solve the problem. Don't panic.

Saylor's response to bear markets, price crashes, and negative sentiment

Natalie Brunell: Bitcoin prices are falling, market sentiment is negative, and critics believe Bitcoin's theoretical foundation is crumbling. What do you think they're overlooking?

Michael Saylor:

first,We need to look at the market from a longer-term perspective.It has only been 137 days, or about four and a half months, since the last all-time high. During this period, the price of Bitcoin has experienced a 45% pullback, which is not uncommon in the field of technology investment.

Looking back at Apple's history, when it launched the iPhone in 2007, it was not well received by the market. It wasn't until the release of the iPhone 3 in 2009 that the market gradually recognized its value.Even so, Apple's stock still experienced a 45% plunge between 2012 and 2013, consistent with Bitcoin's current decline.Apple's price-to-earnings ratio dropped from 30 to 10, and it took seven years to recover from its 2013 low to a P/E ratio of 30. Similarly, Amazon was once considered unprofitable, but eventually became the world's highest-grossing company, with an influence that even surpasses Walmart's.

So, what about Bitcoin? When can you definitively say it's global digital capital? Aren't the signs enough? The US President is telling you, the Federal Reserve's Kevin Walsh is telling you, the Treasury Secretary's Scott Bessent is telling you, even the SEC, the CFTC, and other cabinet members are telling you. BlackRock is telling you, and our company (MicroStrategy) has increased its enterprise value 100 times, and that's telling you too.In the history of capital markets, when has a company ever purchased $55 billion worth of goods and loudly proclaimed it as digital capital, the new currency of the world? Never.

So the question is, is 1 billion enough? Is 5 billion enough? When will we have a sufficiently deep understanding of this question? Long before the world generally agrees, you already have enough information to know that Amazon is unstoppable—a decade before the global consensus. As for Apple, you probably knew it was unstoppable as early as 2009, seven years, or even ten years, before the world generally agreed.Now you have enough information to know that Bitcoin is unstoppable.

Eventually, the world will reach a consensus.Those like Warren Buffett and Carl Icahn will be the ones creating this consensus. They won't be the first; they'll be the last. They won't make a fortune, maybe just two or three times their initial investment, and by the time they enter the market, the price-to-earnings ratio will have risen from 10 to 30. But if you can think independently and withstand the volatility, your investment can yield 10, 20, or even 30 times the return.

In fact, no successful technology investment goes without experiencing a 45% drawdown and navigating that "valley of despair." Our current drawdown has lasted 137 days, but you know, it could take two, three, or even four years. If it takes seven years to recover, then congratulations, it's like Apple back in the day—one of the greatest success stories of the decade.

Why Bitcoin failed to reach its predicted price?

Natalie Brunell: For those who are disappointed with this bull market, for example, that prices haven't exceeded $126,000, what do you think are the reasons?

Michael Saylor:

I believe the market is evolving, and the entire ecosystem is maturing. If you observe all the dynamics, you'll see that the derivatives market is shifting from offshore to onshore, which signifies its maturity. As the US-regulated derivatives market grows, it strips away some of Bitcoin's volatility, while also mitigating some of its upside potential. It smooths out the peaks and troughs, so what you see is no longer...

Instead of 80% drawdown and 80% volatility, it's 40% to 50% drawdown.But the more crucial point is:While the banking sector is making progress in adopting Bitcoin, it is moving slower than those with short attention spans anticipated.It may take banks four to six years to truly embrace a completely new asset class, but people are hoping to see Bitcoin accepted within four months. The reality is, what does it mean if banks haven't started offering banking services, lines of credit, custody, or trading?

This means at the top of the market,There are approximately $2 trillion, possibly 1.8 trillion, worth of Bitcoin held by retail or offshore investors.They are unable to access the traditional banking system; they exist within the shadow banking system. If you own over a trillion dollars in capital but no one is willing to lend to you, how do you liquidate it? If I pledge $10 million worth of Apple stock to JPMorgan Chase, I can get a $5 million loan with extremely low interest, but you can't even pledge $10 million worth of Bitcoin to these mainstream banks for a loan right now.

Therefore, you can only seek help from the shadow banking system or offshore channels.The only "safe" way to realize cash is to sell it, but this has limited price increases.Now a third option has emerged: you can convert Bitcoin into IBIT (a spot ETF). Some banks have started offering lines of credit for it, which is more widespread and cheaper than direct credit to Bitcoin, but we are still in the initial 12 months and the quotas are very limited.

There is a fourth way.If you go to a crypto trading platform or OTC dealer, they might even offer you loans with interest rates as low as 1% or even 0%.But there's a trap here: they ask you to transfer your Bitcoin to them so they can rehypothecation it. This means your $10 million worth of Bitcoin could be resold three or four times, effectively creating $30 to $40 million in selling pressure because shadow banks are selling the assets you've pledged as collateral.

so,What exactly is suppressing asset prices?I believe the problem lies in the lack of a complete, non-recollateralized credit system. When you mortgage your house to a bank, the bank isn't going to resell the houses on your street ten times over; if they did, the value of your house would be lower. The recollateralization phenomenon in the crypto economy smooths out price movements and allows the market to be leveraged on both sides of volatility.

We are at such a stage.The re-mortgaging has suppressed prices, and we can only wait for this process to reverse itself.

Bitcoin's Long-Term Returns: What's the Future Trend?

Natalie Brunell:You often say that "volatility is vitality."Are you worried that your prediction of a 40% annualized return on Bitcoin might change?

Michael Saylor:

Over the next 21 years, I expect the average annual return (ARR) to be around 29%. I've always believed we'll experience rallies and pullbacks, so I see it as a serpentine upward pattern, maintaining a long-term level slightly below 30%, with periods of surges and periods of stagnation.

If you listen to people talking, someone might say, "Something might happen in the Middle East this weekend, and if that happens, Bitcoin is the only asset you can sell, so the price could crash. We're very worried." And I would say,If something really happens in the Middle East, Bitcoin is indeed the only asset you can sell, but it's also the only asset you can hold.This means that many people looking to trade over the weekend are shifting their funds to crypto trading platforms, making it one of the most interesting assets in the world if you're a trader; but if you're an investor who's held for four years, what does it matter if you buy, sell, or crash this weekend?

In fact, the difference here is:Some "hot money" has flowed into this ecosystem, money that wouldn't normally be allocated here.For example, a trader with $20 billion can choose to deposit it in a bank to earn basic interest or invest it in a cryptocurrency trading platform. When Bitcoin drops by 5%, there will definitely be sellers and buyers. Some people will wake up at 4 a.m. on Sunday to buy in for that 5% discount.

These funds did not flow into New York real estate, gold, traditional derivatives, or Nvidia stock. Why? Because you can't engage in that kind of frantic panic selling, angry exits, or stop-loss buying in those markets.Bitcoin is the most volatile because it is the most useful.

There is no such thing as "fairness" in nature. Ten thousand ants attacking a centipede is possible, just like wanting to leverage Bitcoin 50 times or cross-staking a worthless token—no one can stop you. Is that smart? In 99% of cases, it's not smart; you'll lose everything. But the key point is...Those who do foolish things will be weeded out of the market, and if they don't make money, the free market will separate them from their capital.

Bitcoin represents the global capital market; there are always people doing what you wouldn't do or wouldn't want to do.It is this very utility that creates volatility, but it is also this very utility that creates gravity or a magnetic field, attracting all the financial, political, and digital energy in the world, and you must reconcile with it. If you are worried about Bitcoin's performance in the next four days, four weeks, or four months, then you are a trader, and you'd better have an excellent trading methodology. Otherwise, you are an investor with a four-year time horizon, so these fluctuations are simply irrelevant. You only need to know that it is because of those crazy traders that such a massive amount of capital and attention is pouring into this space.

Why didn't retail investors participate in the recent bull market?

Natalie Brunell:Although Bitcoin is currently mainly held by individualsBut Lynn Alden mentioned that retail investors didn't really participate in the recent bull market. What do you think is the reason?

Michael Saylor:I think thoseRetail investors who are passionate about digital capital and have a firm belief in Bitcoin have actually entered the market over the past decade.If you're looking for a non-sovereign, digital store of value asset, you've already found it in the various waves between 2010 and 2015 and bought it as much as you could.

But if you want to attract the next wave of retail investors, they don't want an asset with 40% volatility and a 40% annualized return. They want something with 10% volatility and a return of around 10%, or even something with 0% volatility and an 8% return.

One way to attract mass investors is to offer them products similar to STRC.We would say, "This is an 11% return, tax-deferred, and we've stripped away its volatility." STRC's one-year volatility is lower than the Nasdaq, S&P 500, and even gold. I'm giving you an asset with less volatility than traditional stores of value, but with a guaranteed 10% or 11% monthly return.

You can do a test yourself: Go down on the street and ask 100 people: "Would you rather have a 30% annual return for the next 20 years, but at the cost of a 40% drawdown and volatility three times that of the S&P 500, or would you rather have a bank account that pays out 10% annually and allows you to withdraw your funds at any time?"

I dare say that 95% of the market wants that 10% of bank accounts, and that 5% of retail investors are willing to hold Bitcoin and endure double the volatility of the S&P 500 for a 30% return. That’s probably too optimistic. The actual figure is probably only 1% to 2%.

Most retail investors want something that is 2 to 4 times better than bond funds, or something like the S&P 500 but without drawdowns.We can only attract them when we combine the advantages of equity, credit, and cryptocurrency.

This means that the advantages of equity are double-digit returns and tax deferral; the advantages of credit are price stability, principal protection, low volatility, and clear, consistent cash income; and the advantages of cryptocurrency (Bitcoin) are digital innovation, transformative capabilities, and productivity that is 3 to 4 times higher than that of the traditional economy.

Currently, retail investors must choose between the "Bitcoin rollercoaster" and the "S&P 500 with an annualized return of 10% but accompanied by volatility risk," or they can only accept Apple bonds with an after-tax yield of only around 2%.

That's why my passion for the past year has been focused on this:Can I use engineering methods to take an asset (Bitcoin) with a volatility of 45%, strip away 80% to 90% of its risk and volatility, and give investors a product with four to five times over-collateralization, double-digit returns, and tax-deferred characteristics?

You receive cash dividends every month, and if you want to compound the interest, you can reinvest the dividends back into your principal. When you need to pay your children's tuition or taxes, simply withdraw or sell. To do this, you can't have the drawdowns that Bitcoin does.You need a credit instrument, an issuer willing to over-collateralize, and actively manage it to create price stability—that's what STRC, or digital credit, is all about.In this way, we can attract 10 to 100 times more retail investors than we do now. If we only get 2% to 4% of retail investors in the first wave, we can reach 20% to 40% through digital credit, which is a killer application for digital capital.

How did STRC perform?

Natalie Brunell: Of all the preferred shares you've issued, you seem most interested in Stretch (STRC), and you've been using it to accumulate more Bitcoin. Is there a strategy behind this?

Michael Saylor:We are stripping away Bitcoin's volatility, extracting yields, eliminating currency risk, and eliminating capital risk. Bitcoin's volatility over the past year was approximately 45%. Through Strike, we managed to reduce it to around 38%; through Stride and Strife, we reduced it to around 20%; and through Stretch, we reduced it to around 10%, even dropping to single digits at times. All of this volatility that we stripped away then flowed into MSTR's common stock, bringing its volatility to 80%.

What people really want is a steady 10% return without any volatility.Personally, I seek zero volatility, zero interest rate risk (zero duration), and returns that are several times higher than money market rates.

To achieve this goal, we tried nearly 20 different fixed-income solutions. Currently, most similar products on the market, even with 10x or 20x over-collateralization, trade like triple-junk bonds. The credit market is distorted: even if a bond has $70 of assets backing every $1 of liability, its credit spread (risk pricing) looks like that of a failing company. This business is now like 16 people trading privately in a back alley, with bid-ask spreads as high as 300 basis points—both opaque and inefficient.

You might think:Why not just list debt instruments directly?Because listing traditional term bonds makes no sense. Suppose you sell a 5-year bond; after 4 years, it only has 12 months left to mature. This "non-perpetual" characteristic causes its value to continuously diminish over time. Since it's destined to expire and disappear, why bother making it a publicly traded security? Therefore, we must create a perpetual instrument to list on the stock exchange, which is why we issue preferred stock.

Initially, our idea was simple: offer a 10% dividend, or an 8% dividend plus conversion rights. Strike and Strife were very successful, selling 10 times more shares than other preferred stocks. But we soon realized:Ordinary people not only dislike complexity, but also dislike interest rate fluctuations.

If you ask retail investors what the value of a preferred stock with a 10% return that they can hold forever is, they simply can't calculate it. If you absolutely have to use bond mathematics, its "duration" (i.e., its price sensitivity to interest rates) is approximately 10 years, equivalent to 15 to 18-year Treasury bonds. Natalie, can you follow this mathematical logic? It's very convoluted: if the sensitivity is 10, then when market interest rates fall by 1%, the price should theoretically rise by 10%; conversely, when interest rates rise by 0.5%, the asset value should fall by 5%.

This means that the theoretical value of this tool fluctuates by 10% every time Federal Reserve Chairman Powell speaks.How many retail investors would want to see their "stable assets" shrink by 10% after a single Fed press conference? That's why we created STRC. While long-term investment can bring extremely high capital appreciation potential for professional Bitcoin lending investors (e.g., declining interest rates leading to narrower spreads, potentially doubling the value of purchased assets), explaining this clearly requires discussing the yield curve, rating agencies, and the future of Bitcoin, which is far too complex to grasp.

From the perspective of retail investors, our conversation only takes 12 seconds:"I want to put my money in the bank and get a 10% return every year, and the government won't tax me." "Deal." Don't worry about interest rate fluctuations, changes in corporate credit, or even whether Bitcoin doubles or halves—none of that matters. The only important fact is: you get an 11.25% return, and it's tax-free.

Of course, there are still risks:If Bitcoin were to go completely to zero, it would be an existential crisis. The global credit market is worth a staggering $300 trillion, but everyone is currently in a terrible situation: to earn that 5% return, they must endure the risks of junk bonds, liquidity shortages, or waits of up to a century.What do retail investors want? They don't want any duration risk, currency risk, credit risk, or volatility. They just want to be able to get their money back at any time, with returns several times higher than money market funds, and without paying taxes.

Traditional bond models have reached their limit; they're for professional investors. Retired Air Force sergeants just want a stable monthly cash flow. Why monthly? Because conventional markets don't support weekly or daily payments. If Nasdaq supported hourly payments, we would too. Therefore, we've created the most efficient, tax-efficient, and simplest fixed-income stream.The company's five-year vision is: Bitcoin is digital capital. I'll spend a thousand hours explaining it to you, and you'll eventually understand, but you'll still have to endure a 45% crash and ridicule from the whole world; on the other hand, do you want a bank account that pays 11% and has deferred taxes? Choose STRC.

The former explanation takes a thousand hours, the latter only 10 seconds. The world doesn't need to read ten thousand pages of history; it only needs answers, or even just products, like the iPhone. You use air conditioning, tap water, and lights every day—do you study how they work? No. You only need a pill to solve the problem. If I could cast a spell to instantly make you happy and rich, you'd definitely sign up immediately. STRC is that spell:You buy it, it pays you double-digit tax-free dividends, and you can enjoy tax benefits when you leave it to your descendants. Other than that, you don't have to worry about anything..

This is similar to Standard Oil in its early days. It was called "standard" because it guaranteed that kerosene lamps wouldn't suddenly catch fire; it was safe. Consumers need trust in the brand. Bitcoin is evolving from a niche community of "amateur radio enthusiasts" to the mainstream. Previously, playing with radio required understanding physics; now, six-year-olds use radio technology while scrolling through TikTok, but they don't care about the principles. Bitcoin will be the same. Ultimately, 8 billion people will manage digital capital on their phones, seamlessly switching between savings coins, stablecoins, and various securities. Just like that video where I held up an iPhone and said, "Everyone will want it," STRC solves the market's ultimate pain point: eliminating volatility and leaving cash.

Media Sentiment and Fluctuation Cycles

Natalie Brunell: We've seen extreme media frenzy and praise whenever Bitcoin hits a new all-time high; conversely, when prices pull back, a pessimistic mood emerges, with people over-predicting a negative outlook. Do you feel like someone is hoping you fail? How do you cope with these extreme emotional swings?

Michael Saylor:This struggle is real, but it's volatility that drives participation, interest, and speculation. When Bitcoin prices fall, everyone's talking about us, while nobody talks about non-volatile assets like Upper East Side real estate or lumber prices.Without news, there is no interest.

I've been running publicly traded companies for many years. In traditional companies, information is released quarterly, and investors might only make a decision once a year. But after entering the Bitcoin space, we realized that the assets we hold allow our website to update every 15 seconds. We went from updating the financial market every 12 weeks to updating it every 15 seconds.

For every $10,000 fluctuation in Bitcoin's price, our company gains or loses approximately $7 billion to $8 billion.Previously, our company worked hard all year to earn $70 million. Now, a $100 fluctuation in Bitcoin is equivalent to our annual workload.We've directly connected an energy source, a volatility generator, to the balance sheet, which drives a continuously cyclical news cycle.Even on television, skeptics were considering shorting us, while bulls were looking for buying opportunities. Without this volatility, neither short-term nor long-term investors would be paying so much attention to us.

Previously, the Wall Street Journal only reported on publicly traded companies because the stories of private companies were irrelevant to the average reader's buying and selling. Now, we've made a company "interesting" by putting a huge amount of Bitcoin on its balance sheet and letting it vibrate, making the company 10,000 times more interesting.

This toxicity and extreme evaluation actually stems from a genuine interest in Bitcoin. The breakthrough of the crypto economy lies in creating a globally accessible, 24/7, and incredibly interesting financial asset. In contrast, I can tell you how to destroy a financial asset: prohibit purchases by people outside the US, restrict trading hours to 9:30 AM to 4:00 AM, mandate a three-month account opening review, and add a $100 million threshold. If you keep adding these restrictions, the asset becomes lifeless, and even giving it a difficult-to-remember six-digit code diminishes its appeal.

However,The crypto industry has gone in another direction: anyone, anywhere in the world, can start trading within 60 seconds by simply downloading an app.Even during bank holidays, you can still move $1 billion worth of Bitcoin in minutes for a mere 44 cents. This is a digital revolution, where money wants to circulate at the speed of light, around the clock. The waterfall doesn't stop on bank holidays, nor does electricity, gravity, or the speed of light. Bitcoin wins because this digital capital, programmable by AI and vibrating millions of times per second, will replace slow, cumbersome traditional forms of finance through a brutal Darwinian evolution.

Does quantum computing pose a threat to Bitcoin?

Natalie Brunell: In the Bitcoin community, we often say "Don't trust, verify," but many ordinary people lack the technical skills to verify. Is quantum computing truly an existential threat? I saw MicroStrategy recently released a statement about ensuring Bitcoin is "quantum-resistant." Can you explain why you don't consider this a risk already reflected in the price?

Michael Saylor:

first,The broad consensus in the cybersecurity community is that quantum risks (if they exist) will be at least 10 years from now; it's not something that happens in the next decade.Whether a quantum threat exists remains an open question, but it's certain that there is no imminent threat at present. If a quantum risk were to materialize, you would see massive upgrades to the software running the global banking industry, the internet, consumer devices, AI networks, and all encrypted networks (including Bitcoin). We would adopt "post-quantum resistant cryptography," and this is not a sudden development; we can all foresee its arrival.

Bitcoin's software is constantly evolving, and we're currently discussing upgrading from version 29 to 30. Nodes, hardware, wallets, and trading platforms will all be upgraded accordingly. In 10 years, a global consensus on the best approach to Bitcoin will naturally emerge. Why am I not worried now?Because all stakeholders—Google, Microsoft, Apple, Coinbase, BlackRock, the US government, the Chinese government, JPMorgan Chase—have to deal with the same problem.

In fact, the crypto community is currently the most cutting-edge cybersecurity community.If you look at the security protocols for mobile crypto assets (multi-factor authentication, hardware private keys, etc.), they are orders of magnitude stronger than those for bank transfers or stock trading. I believe the crypto community will be the first to perceive and respond to this threat. We have already announced a Bitcoin security plan, and even my early donations to MIT were for Bitcoin security research.Quantum narratives are not currently the biggest threat to Bitcoin.

The reason we're still talking about the threat of quantum computing is because other so-called risks have failed to materialize. Ten years ago, the Bitcoin community was embroiled in the "block size war," with some even predicting that Bitcoin would fail due to insufficient bandwidth. However, ten years later, the free market has solved that problem.

In fact, this kind of "doomsday narrative" has always existed in human history. Whether it's "alarmists," "ambitious speculators," or "idealistic intellectuals," they often fabricate various crises to gain influence, capital, or power. How can I get rich? How can I be elected governor if I don't promote some kind of "doomsday narrative"?

99% of these narratives are just a business. Like someone selling "fall insurance for carrying heavy objects" or "autism vaccine for children," the probability of these events happening is probably only 0.01%, but if you insure against every tiny possibility, your income will eventually be completely depleted, leading to bankruptcy. The reality is, ten years from now, you might simply need to tap "software update" on your iPhone to solve the problem.

The threat of quantum computing is the latest form of "quantum FUD," and when this narrative is ultimately proven to be nonsense, someone might jump out and claim we need to implant nanobots in our brains, and Bitcoin isn't ready for that. This isn't just a Bitcoin story; it's a microcosm of human history. Faced with these so-called crises, you simply need to maintain a constructive optimism. You can choose to believe that humanity is too foolish to cope with technological change and hand your money over to speculators who predict the end of the world; or you can believe that we will upgrade software and use new technologies to make life better.

Remember the quote on the back cover of The Hitchhiker's Guide to the Galaxy: "Don't Panic."Even if a real cybersecurity threat emerges, your bank, government, and business software will be forced to upgrade to cope. Remember the Y2K bug? The whole world panicked, but ultimately nothing happened. Humanity has overcome thousands of similar "trouble-making" events throughout history, and the quantum threat will be one of them.

What is the strongest objection to Bitcoin?

Natalie Brunell: I have an interesting question for you: What do you consider to be the strongest objection to Bitcoin right now? And why do you reject it?

Michael Saylor:

The strongest argument for Bitcoin right now is that it's too new.As a new thing, it hasn't been around long enough, and perhaps I hope to see it last much longer before I trust it for the rest of my life.

It took humanity 30 years to embrace electricity, while Bitcoin has only been around for 17 years. One might ask, "How many people have flown on a jet airliner 17 years after the invention of the airplane?" The airplane was invented in 1903, and by 1920 it was still in its infancy. The world is full of such profound innovations that are eventually embraced by everyone, but the process often takes more than 17 years.

I believe the answer is "time".Early pioneers are always a minority. Just like after the invention of the automobile, it didn't become widespread until the Ford Model T appeared, and it took many more years for everyone to own a car.

This is essentially a natural process:Transform innovative technologies into consumer or industrial devices and establish a track record that makes people willing to stake their lives or reputations on them.I believe we are currently in the process of "commercialization".

Does MicroStrategy's Bitcoin cost base matter?

Natalie Brunell: Before you finish your summary, I'm curious, you seem completely unconcerned about cost price. A lot of people are trying to find the bottom right now, and obviously many are staring at technical charts, but you seem completely unaffected, just buying at any price. Can you explain this to those who think, "Since it might go lower, why not accumulate at a lower cost price?"

Michael Saylor:You can think of us as using DCA (Discounted Cost Averaging), but the key point is: we're using equity; we're not borrowing. When we buy Bitcoin, if we sell equity and then buy Bitcoin, then whether we buy it for $100,000 or $200,000,We are simply engaging in a perpetual, risk-free exchange.We are exchanging equity for Bitcoin. When should we exchange equity for Bitcoin? As long as it is "accretive".

If Bitcoin rises by 10%, but our equity rises by 25%, then the swap would be profitable. If Bitcoin subsequently falls by 20%, would you regret it? Of course not, because if you didn't do it, you wouldn't own those Bitcoins in the first place.

By that point, you've actually reduced the risk of your equity. If you place a stable asset beneath your equity, the risk actually decreases, especially when you're making this swap at a premium. So the only real question is: is this swap beneficial to the shareholders? At one level, exchanging preferred stock for Bitcoin is worthwhile; at another level, exchanging common stock for Bitcoin is also worthwhile.

Once you've completed the transaction, the future price movement of Bitcoin isn't that important. If you're exchanging common stock for Bitcoin, it's irrelevant because you won't have a continuous debt for the next few thousand years.

Of course, there is a theoretical possibility that if the exchange involves preferred stock, dilution might occur. For example, if I pay 10% preferred stock dividends, while Bitcoin only returns 5% over the next 100 years, then this exchange would be dilution for common stockholders.Therefore, the calculation of exchanging "digital credit" for Bitcoin is much more complex, but the calculation of exchanging common stock for Bitcoin is very simple.

If you're swapping debt, such as a 10-year debt with a 5% cost, to buy Bitcoin, then you need Bitcoin to appreciate by more than 5% over those 10 years to avoid being diluted.

If you use "margin debt" to exchange for Bitcoin—for example, if you simply borrow money and buy with 10x leverage—let's say you buy 1 billion Bitcoins with only 100 million as collateral. If Bitcoin drops by 10%, you will be forced to liquidate and lose all 100 million. Why is this so dangerous? Because you only have "one minute" to borrow this money.

So the real core question is: what is the duration of the swap?Are you taking out a "one-minute flash loan"? If so, the purchase price relative to the current price is extremely important. Are you borrowing money for ten years? Then its importance will only become apparent after ten years. If you are borrowing perpetual funds, never to be repaid, then the importance of the purchase price becomes very obscure.

Financial mathematics varies. The simplest way to think about it is:If you are exchanging equity for Bitcoin, the price is not important; what matters is the premium or relative valuation you pay when you enter the transaction.If you exchange preferred stock for Bitcoin, Bitcoin's performance over 30 years will be somewhat affected. However, even if Bitcoin's annual increase is less than 10%, and we pay a 10% dividend, it can still be beneficial to common stock in certain scenarios.

In fact, when we sell digital credit to buy Bitcoin, we have 20 to 30 years to prove ourselves right. If you're selling corporate bonds or convertible bonds, those instruments have much shorter durations, perhaps three or four years, and you have to prove yourself right much faster.

What most retail investors don't understand is that their only source of credit is "margin credit," which is essentially one-minute credit. If they make a mistake, they'll be liquidated over the weekend, while with the credit we use, we can be wrong for 30 years.

I could paint a picture of all sorts of scenarios for you: we pay 10%, Bitcoin only returns 8%, we've been wrong for 30 years, but it's still a good idea for common stock. Explaining that would take hours, and that's a completely different podcast; we'd need to delve into the first, second, and third-order financial dynamics of monetary networks and "harmonics."

But the truth is:If it were common stock, and we had a 10 to 30-year timeframe to prove ourselves, it wouldn't matter how Bitcoin performs over the next 100 years.We don't participate in other types of short-term debt, so (short-term prices) really don't matter. That's why our average price doesn't make any substantial difference.

What really matters is the nature of the security swaps we're doing. Selling $1 billion of STRC with a monthly changing interest rate, selling $1 billion of STRF with a perpetual 10% dividend, or selling $1 billion of common stock—these three have completely different dynamics, and the mathematics behind them is far more complex than a tweet can explain. I assure you that any critic comparing this has never considered the second-order consequences of these operations, let alone the third, fourth, and fifth-order harmonics we're dealing with.

Bitcoin is mentioned in the Epstein document.

Natalie Brunell: Some people are very concerned that Bitcoin and core developers appeared in Epstein's files. People are very angry about Epstein's documents. Is this a concern of yours?

Michael Saylor:That's not the point at all. I think they're probably tired of the "quantum threat" narrative, so they've turned to fabricating the "Epstein FUD" story. In the mainstream media, they say it's Epstein trying to influence Bitcoin. Obviously, Epstein may have used an iPhone, ordered things from Amazon, used Linux at some point, and funded the Democratic or Republican parties. So what if Epstein had connections to the Democrats, Republicans, Apple, or Google, or if he used Google Search? Am I supposed to sell my Google stock because of that? If you're a Democrat, you're still a Democrat; if you're a Republican, you're still a Republican. This so-called "contagion" is just a gimmick to increase engagement.

Bitcoin is Bitcoin.It's controllable; you can audit the code. Just as you don't need to know Satoshi, do you need to know who Prometheus is to decide not to set yourself on fire? Who Prometheus is doesn't matter. Fire is fire; it's a chemical reaction. You can study chemistry and thermodynamics to understand it.

Bitcoin is a natural force that anyone can use.Ultimately, it's a protocol. Just like con artists use Arabic numerals, criminals speak English. Every movie has a car chase; sometimes you hope the guy gets away, sometimes you hope he gets caught, but you still drive, right? So I think it's just a distraction. We shouldn't get bogged down in these things, but rather focus on the big picture like a laser beam.

Bitcoin is digital capital; it is a revolution in the capital market.It is a profound innovation rarely seen in human history, allowing us to tightly integrate economic energy with individuals, companies, or any entity.

This ability to tightly bind economic energy to individuals is as profoundly significant as the discovery of fire, the use of electricity, or even the evolution of mammals' ability to store fat—it is a fundamental building block of life. On top of Bitcoin as the underlying capital, we can build digital credit (such as STRC), and even go further, create true "digital currency." Imagine a bank account with an 8% annualized return and no volatility; who owns it now? Nobody. Who wants it? Everyone.

This is a massive opportunity worth $300 trillion, according to conservative estimates.The existing traditional credit market is plagued by low yields, heavy taxes, and various credit, duration, and currency risks. The outdated financial assets and agreements of the 20th century are no longer adequate for today's world; we are entering a new era driven by digital assets, digital capital, digital credit, and digital currencies.

Can this solve all the problems? Obviously not; there are still many dilemmas in the world that digital currencies cannot address. However, if you walk down the street and ask 100 people if they want more money, everyone will answer yes. Therefore, this is undoubtedly an opportunity with practical significance.

Money itself cannot repair itself.Bitcoin is merely the foundation of capital; we must build credit upon it, and then establish currency on that credit. We need to de-marketize it, seek regulatory approval, and encapsulate it within ETFs, crypto tokens, private funds, or public funds.

You have to get the Japanese to approve it, the Emiratis to approve it, the Americans and Europeans to approve it. You have to argue with the regulatory agencies in China, Australia, and Canada. Then people will stare at it and say, "This looks too good to be true, I don't trust it." So you have to explain why it's trustworthy, and then they'll oppose you, and you have to come back and explain again and again, because that's how the world works.

Thirty years after this podcast ended, everyone will take digital currency for granted.Just as we view electricity, cars, fire, antibiotics, or airplanes today, these great inventions have all gone through periods of notoriety, causing intense panic and skepticism throughout history.

This is just the latest technological revolution. As William Gibson said:"The future is already here, it's just not being distributed evenly."Thirty years from now, all of this will be social consensus. But by then, you and I will both be facing unemployment because when something becomes as commonplace as tap water, it loses its appeal and the extra opportunities disappear. Nobody's going to interview a company that installs water supply at headquarters, right?

Therefore, I believe we are very fortunate to live at this turning point full of uncertainties, and to have such a moment to witness a great opportunity. Let us continue to move forward and never stop.