Author:Wall Street CN

Brent crude oil prices temporarily lost upward momentum and fell back to $96, influenced by rumors of potential US-Iran negotiations. However, supply-side tensions have not eased: oil flow in the Strait of Hormuz remains more than 95% below normal levels, and the overall oil flow deficit in the Persian Gulf has widened to 17.7 million barrels per day. Meanwhile, demand-side pressures are accelerating.

Refining capacity has been severely damaged, and refined oil prices have soared, with the demand-damaging effect beginning to spread from Asia.Several airlines have cut flights due to rising fuel costs, many Asian countries have implemented work-from-home policies to control road fuel consumption, and economies such as South Korea have introduced export bans or price controls on gasoline, jet fuel, and diesel. Analysts warn that...If supply chains cannot be restored within days, the demand disruption will quickly spread to Europe and the world.

On the supply side, Trump's recent comments on potential US-Iran negotiations, coupled with rumors of a ceasefire agreement, put downward pressure on oil prices. According to CCTV News, a spokesperson for Iran's Hatem Anbia Central Command directly addressed the US on the 25th, stating: "The Americans are negotiating with themselves; don't call your failure an agreement."

Although Iranian officials denied contact with the US, Israel subsequently confirmed indirect communication between the two sides, briefly easing market pricing of a prolonged disruption. Goldman Sachs currently expects the disruption to oil flow in the Strait of Hormuz to continue until April 10.

With supply and demand pressures intertwined, the backlash from high oil prices on demand is evolving from a regional phenomenon into a global challenge.

Demand disruption: Asia is the first to feel the pressure, and the risk of contagion is rising.

The cumulative effects of supply chain disruptions are rapidly translating into substantial demand damage. The sharp rise in jet fuel and diesel prices has already significantly dampened end-consumer demand.Several airlines have announced flight cuts, while policymakers in some Asian countries are pushing for wider work-from-home arrangements to ease pressure on road fuel demand.

In terms of policy responses, South Korea set price caps on gasoline and diesel to protect domestic consumers from the impact of soaring wholesale prices. Several European countries have also subsequently introduced export restrictions on certain petroleum products.

Analysts pointed out thatThe current demand disruption is still in its early stages and is concentrated in Asia. If supply chains cannot return to normal within days, rather than weeks, this effect will quickly spread to Europe and eventually affect other parts of the world.Historical experience shows that once a shortage of refined oil products triggers a chain reaction, the recovery period is often much longer than initially expected.

Energy shock spreads outwards; markets reassess inflation risks.

The energy shock is spreading to a wider range of asset classes. The correlation between crude oil prices, US Treasury yields, and breakeven inflation is tightening again.The market is rapidly repricing the “second wave of inflation” rather than downplaying it.

In the interest rate market, if the yield on the 10-year US Treasury bond breaks through 4.4%, this situation will no longer be confined to the interest rate market itself, but will evolve into systemic pressure covering multiple asset classes such as stocks, credit, and exchange rates. Currently, the stock market's pricing of this risk is still insufficient.

Emerging markets are facing a triple shock from oil prices, interest rates, and volatility. The EEM (Emerging Markets ETF) is testing a key trendline support, and the VXEEM volatility index is rising rapidly. Once the support level is broken, selling pressure is likely to accelerate rather than ease.

Supply-side pressures remain unresolved; offshore oil storage nears its limit.

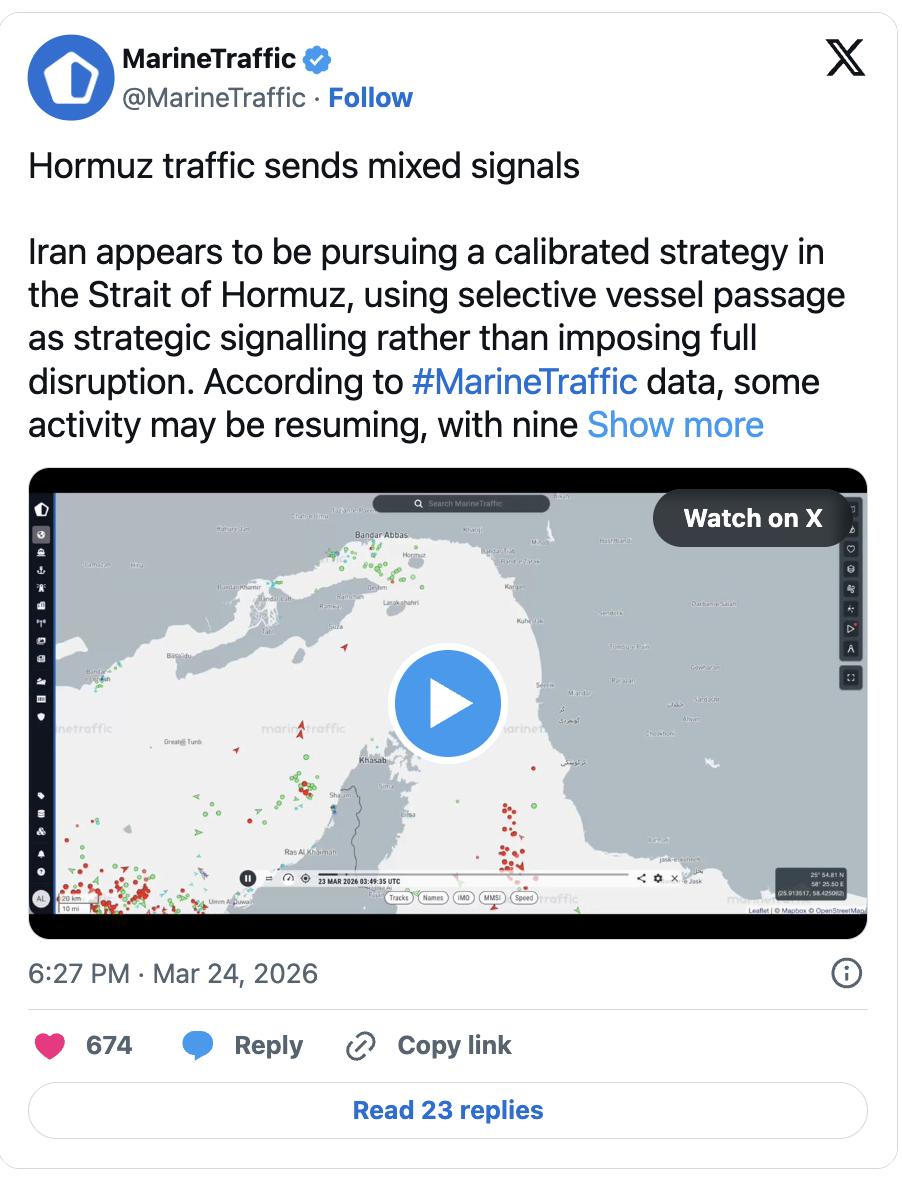

The situation in the Strait of Hormuz remains unfavorable, continuing to support high oil prices.In recent days, the average daily passage of oil tankers through the Strait of Hormuz has been only about two, a 95% decrease compared to normal levels, although there has been a slight recovery recently. US officials have confirmed that Iranian-laid mines remain in the Strait.This poses a persistent threat to shipping.

The broader Persian Gulf flow data is equally alarming. Including pipeline diversions via the ports of Yanbu and Fujairah, the loss in Persian Gulf oil flow (4-day moving average) has expanded to 17.7 million barrels per day. Strait throughput is 98% below normal, at only about 400,000 barrels per day, with a net replenishment of approximately 1.9 million barrels per day from the pipeline diversions.

Meanwhile, floating storage of oil from the Persian Gulf has increased by 74 million barrels since February 27, approaching the estimated upper limit of shipboard storage capacity at that time.This indicates that offshore storage space is gradually becoming increasingly tight for oil-producing countries in the Gulf region.If supply-side pressures are further transmitted downstream, it will add new uncertainties to the refined oil market, which is already suffering from demand disruptions.

Refining facilities become the primary target; the refined oil supply dilemma remains unresolved.

Supply-side pressures are extending from crude oil to refined products. The International Energy Agency (IEA) estimates that at least 40 energy assets in the Middle East have suffered severe damage since the outbreak of the current conflict. Notably, the substantial damage is currently concentrated in refining facilities rather than crude oil production facilities, where production cuts are mostly preventative shutdowns.

Among them, the Mina Al-Ahmadi refinery in Kuwait was attacked last Friday, prompting Goldman Sachs to raise its estimate of the disruption to refining capacity in the Middle East to 2.3 million barrels per day.The continued damage to refining capacity means that even if crude oil production remains relatively stable, the tight supply of refined oil products will continue.

Attacks on energy assets have subsided somewhat in the past two days, but concerns about a new round of action have not yet dissipated, given that Israel and the United States previously launched strikes on natural gas facilities in Iran's Isfahan province. Risk premiums for Gulf energy infrastructure remain high.