Author:链捕手

Author: Chloe, ChainCatcher

On February 26, 2026, blockchain detective ZachXBT officially uncovered the truth behind the Axiom Exchange insider trading case: a senior business developer abused his backend privileges for ten months, illegally profiting over $400,000 by tracking the private wallets of key opinion leaders (KOLs). This report not only closed the case but also brought to a close the $40 million prediction bet on Polymarket that had the entire market on hold.

However, the truth still reverberates. Before the investigation was revealed, the market unanimously pointed the finger at Meteora, with its implied probability reaching as high as 43%. This was not unfounded speculation. According to the crypto asset data platform RootData, Meteora is backed by a Singaporean and Malaysian startup team led by Meow and Ben Chow. They started from the ruins of Mercurial Finance and built a full-stack matrix within the Solana ecosystem, encompassing traffic entry points, transaction aggregation, and liquidity infrastructure.

From the LIBRA controversy and the MET airdrop scandal to the Upbit IPO rumors, Meteora's history has always lingered in the gray area of "information asymmetry arbitrage." Although ZachXBT eventually turned his attention to Axiom, the many questions surrounding Meteora seem to have never been truly answered.

From Mercurial to the "Jupiter system," the underlying relationships remain connected.

It all started in 2021.Using the pseudonym Meow, he and Ben Chow founded Mercurial Finance on Solana.Positioned as a stablecoin asset management protocol on Solana, Mercurial aims to become the Solana version of Curve. During that bull market cycle brimming with liquidity, Mercurial not only received support from Alameda Research but also completed its IEO (Initial Exchange Offering) on the FTX platform with the personal endorsement of SBF. At that time, TVL once accounted for 10% of the Solana ecosystem, enjoying immense success.

In 2022, the FTX empire collapsed, severely damaging Mercurial. However, the two founders did not choose to liquidate and leave, but instead launched a rebuilding initiative known as "Project Phoenix": splitting the business in two. Meow led Jupiter, aiming to solve Solana's liquidity fragmentation by defining optimal prices through routing algorithms; Ben Chow steered Meteora, focusing on developing a highly capital-efficient Dynamic Liquidity Market Maker (DLMM) model. This split, ostensibly a focus on specific business areas, was in reality a complementary flywheel of two independent brands, while remaining interconnected in terms of shareholder structure and underlying logic.

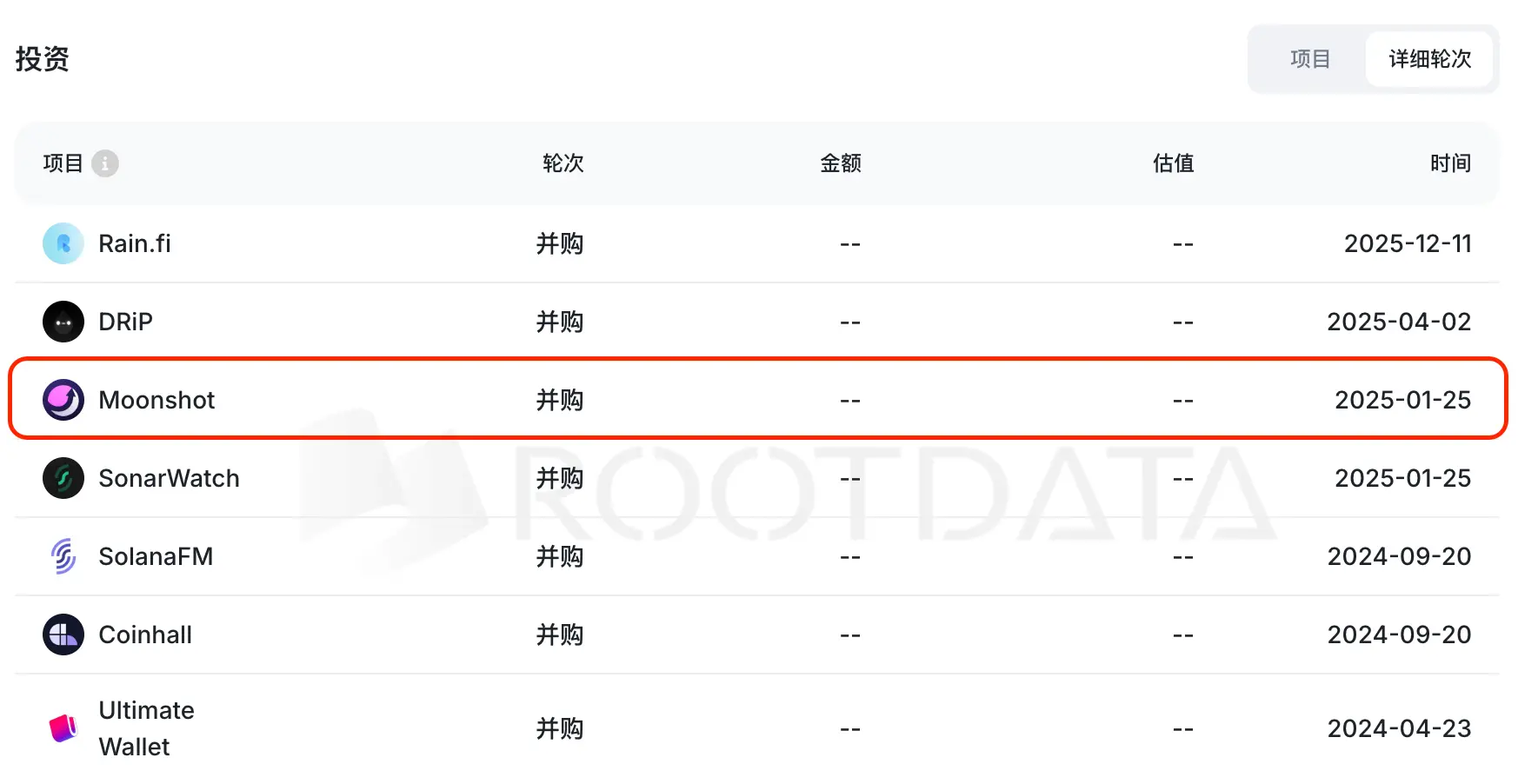

On the traffic front, Jupiter employs an aggressive strategy. According to RootData, a crypto asset data platform, in January 2025...Jupiter acquired MoonshotThis successfully opened up the shortest path for retail investors to directly purchase meme coins via Apple Pay or credit cards, lowering the consistently high barriers to entry in the crypto industry to a consumer-level standard.

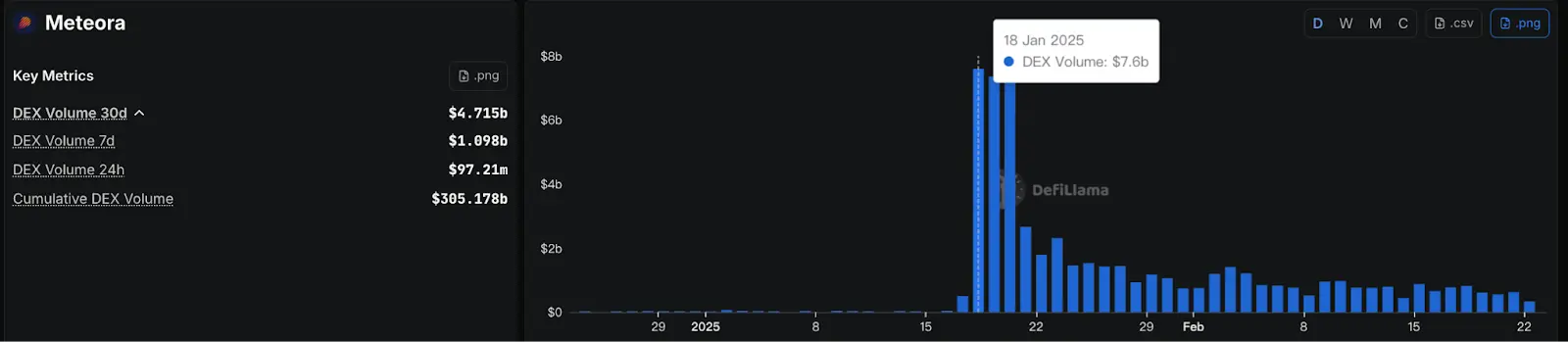

This strategy successfully translated into real-world monetization during the Trump token boom: when a large influx of retail investors arrived via Moonshot, these buy orders precisely matched the initial liquidity the Trump team had built on Meteora. This closed loop of "capturing traffic in the front end and handling transactions in the back end" enabled Meteora to achieve a single-day trading volume of $7.6 billion, accounting for 20% of the total DEX trading volume on the Solana chain.

Meanwhile, Jupiter's flagship DEX aggregator has evolved into a cornerstone of the Solana ecosystem. It's no longer limited to token swaps but has introduced continuously iterating products such as perpetual contracts, lending markets, and prediction markets. Thus, Moonshot, Jupiter, and Meteora have built a fully closed-loop ecosystem encompassing fiat currency deposits, front-end traffic, transaction routing, multi-functional products, and automated market making, completing their transformation from "project teams" to "ecosystem controllers."

Meteora's airdrop controversy and Upbit's listing uncertainty

While vertical monopolies bring efficiency, the resulting information asymmetry and suspicion of power abuse have always loomed over the Jupiter ecosystem. The Meteora (MET) airdrop distribution and the Upbit launch controversy have led outsiders to question whether this is truly "community-first".

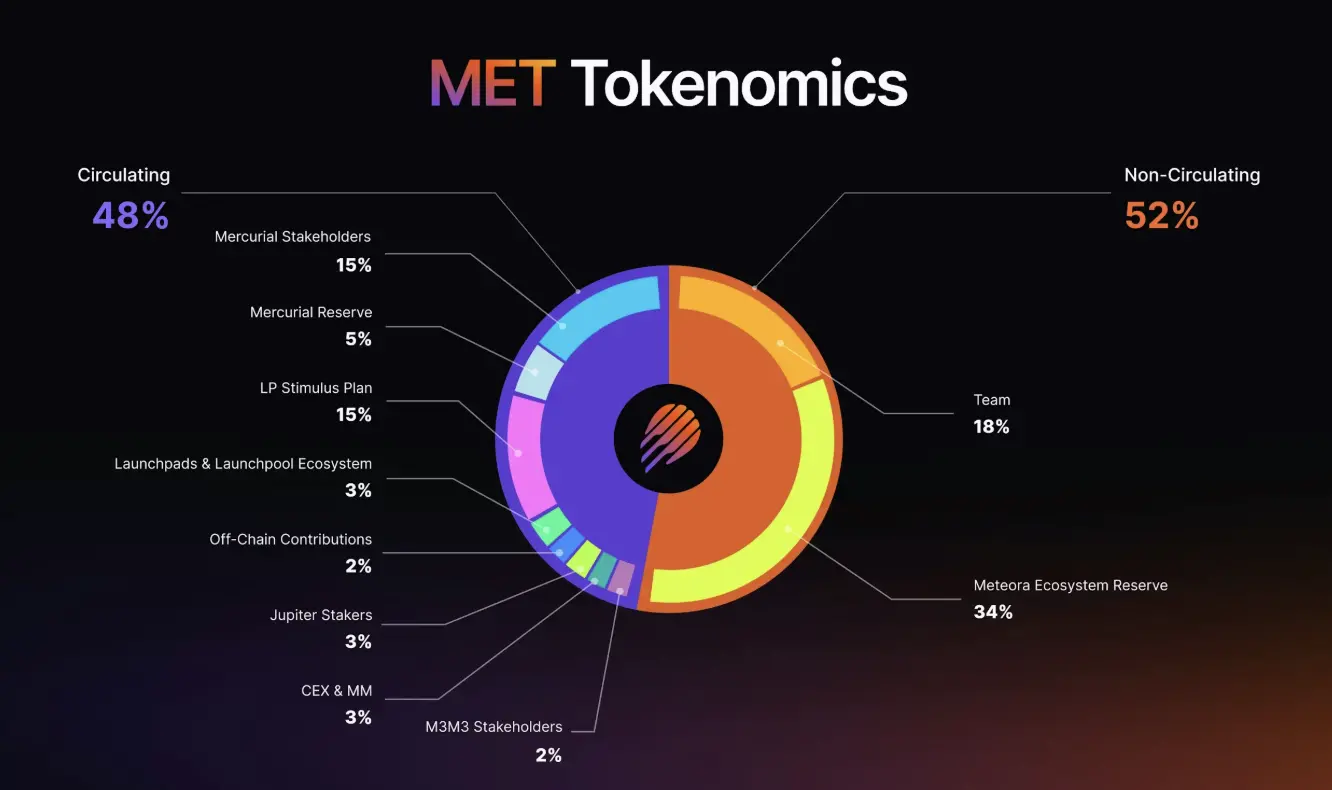

On October 23, 2025, Meteora launched TGE. At that time, the total token supply was 1 billion, and 48% (480 million tokens) of the total supply were unlocked and released into circulation all at once. The team claimed this was intentional, designed to achieve "true price discovery," but the market's response was extremely disastrous. Within hours of opening, MET plummeted from $0.90 to $0.51, a single-day drop of over 55%.

Initial on-chain data analysis of TGE revealed significant flaws in the fairness of the airdrop distribution. The first four claiming addresses received approximately 45.94 million tokens, representing 28.5% of the total distributed. The behavior of these addresses was unusual.

Suspect address #1 (3vAau...ae): Claimed 12.15 million MET (worth $6.31 million at the time). This address not only claimed Mercurial (MER) airdrops but also sold over 30 million JUPs to exchanges in the past, using the same selling tactics on METs.

Addresses 2 and 3: These two addresses exhibit a very high degree of synchronization, with their JUP transfer amounts repeatedly and precisely locked at a specific number of 2,622,632.41, and their activity times being completely consistent, suggesting they may belong to a group controlled by the same faction.

Address #4 claimed 10 million MET. Strangely, this address was created after the snapshot time and has never participated in any liquidity additions or staking activities. This "out of nowhere" claim completely deviates from the logic of the points system.

If airdrop distribution is a manifestation of power corruption and abuse, then the information leaks regarding exchange listings touch upon the industry's gray areas. On November 18, 2025, Meteora officially listed on Upbit, but even before the official announcement, sources claimed to have obtained this information and profited from the leaks. Although there is no direct evidence pointing to Jupiter or the Meteora core team, combined with the controversy surrounding the MET airdrop, the community has already labeled it as distrustful.

Libra Scandal: Ben Chow's Resignation and the Rashomon of Responsibility

Rewind to February 2025, when the LIBRA token, endorsed by Argentine President Javier Milei, suddenly appeared, its market capitalization soaring to $4.6 billion in just a few hours before nearly disappearing to zero.Tens of thousands of investors lost more than $280 million.Public opinion quickly turned against Meteora and the Jupiter team.external accusationsDespite knowing that the token launch was rife with pre-emptive strikes and market manipulation, the team still provided LIBRA with a "verified" label and liquidity support. Although the team insisted that the verification was merely to prevent counterfeit tokens, not to endorse them, the public clearly didn't buy it.

Under pressure from public opinion, Meteora's core leader, Ben Chow, announced his resignation.The law firm Fenwick & West has been hired to conduct an independent investigation.However, this move triggered a second crisis: Fenwick & West is embroiled in a class-action lawsuit stemming from the collapse of FTX, with allegations that the law firm assisted SBF in blurring the financial lines between FTX and Alameda Research.

The community's reaction was almost unanimously sarcastic. Using a former FTX legal counsel who was itself embroiled in lawsuits to "independently investigate" the ethical issues of former FTX projects was a "controversiality-based" approach that made outsiders even more suspicious of whether the Jupiter group was truly willing to become transparent. Although Meow eventually stated under public pressure that he would re-evaluate the choice of legal counsel, there was no follow-up explanation.

The double-edged sword effect of vertical monopolies on the DeFi ecosystem

For the average user, vertical monopoly translates to extreme efficiency. When you deposit funds using Moonshot, navigate through Jupiter, and ultimately complete the transaction in a Meteora pool, the failure rate and user experience are minimized because the entire process is optimized by a team within the same ecosystem. Furthermore, because the team controls both traffic and liquidity, they can quickly foster tokens with phenomenal potential like Trump, thus maintaining Solana's popularity and on-chain activity.

However, for the entire ecosystem, this high concentration is almost synonymous with high risk. When a team simultaneously controls front-end traffic, transaction routing weights, lending markets, and liquidity pools, if its core private keys experience security issues, or if core members are forced to shut down due to legal disputes, liquidity could suffer a severe blow in a short period of time.

More concerning is the issue of "innovation monopoly." Jupiter controls most of the order flow routing on Solana, meaning that new DEXs that don't integrate into Jupiter's ecosystem almost completely lose the basic means to acquire traffic. This oligopolistic structure at the routing level essentially constitutes an invisible market barrier—it's not the product's superiority that determines who wins, but rather the closeness of their relationship with Jupiter. Even more worrying is that Jupiter itself participates in liquidity business through Meteora, creating a clear conflict of interest between "determining traffic flow" and "benefiting from traffic itself."

Conclusion: The shadow of the Jupiter group, and the answers the market has yet to find.

ZachXBT ultimately exposed Axiom, but this does not mean that Meteora, or the entire Jupiter group, is innocent. It may simply mean that ZachXBT's investigation did not cover that area, or that there was insufficient direct evidence.

The controversy surrounding Meteora has never been a black-and-white legal issue; it is a complex web of gray areas: the exploitation of information asymmetry, airdrop controversies, the selection of legal counsel, and even the recurring excuse of "we only provide infrastructure" after the collapse of several high-profile tokens.

This startup team, originating from Singapore and Malaysia, has indeed demonstrated its product execution capabilities to the market over the past three years. However, they have also been exploiting every regulatory gray area with their business logic to maximize arbitrage. Trust in the crypto industry has never been easy. When the traffic entry point, transaction execution, and liquidity of an ecosystem are controlled by the same interest group, the costs are ultimately borne by retail investors.

The Polymarket bet is over, but the market still doesn't have an answer regarding Jupiter and Meteora.