Author:Wall Street CN

When will global crude oil inventories "bottom out"? JPMorgan Chase has calculated a countdown curve.

In early April, JPMorgan commodity analyst Natasha Kaneva released a new report that systematically calculated the rate at which global crude oil inventories were depleted under the impact of the Strait of Hormuz blockade, and provided a complete timeline from "bottoming out" to "rebuilding." The conclusion is straightforward: the inventory buffer is being rapidly depleted, and the market is not far from its "operating minimum"—it may bottom out in May.

What is the "minimum operating value" and why is it a red line?

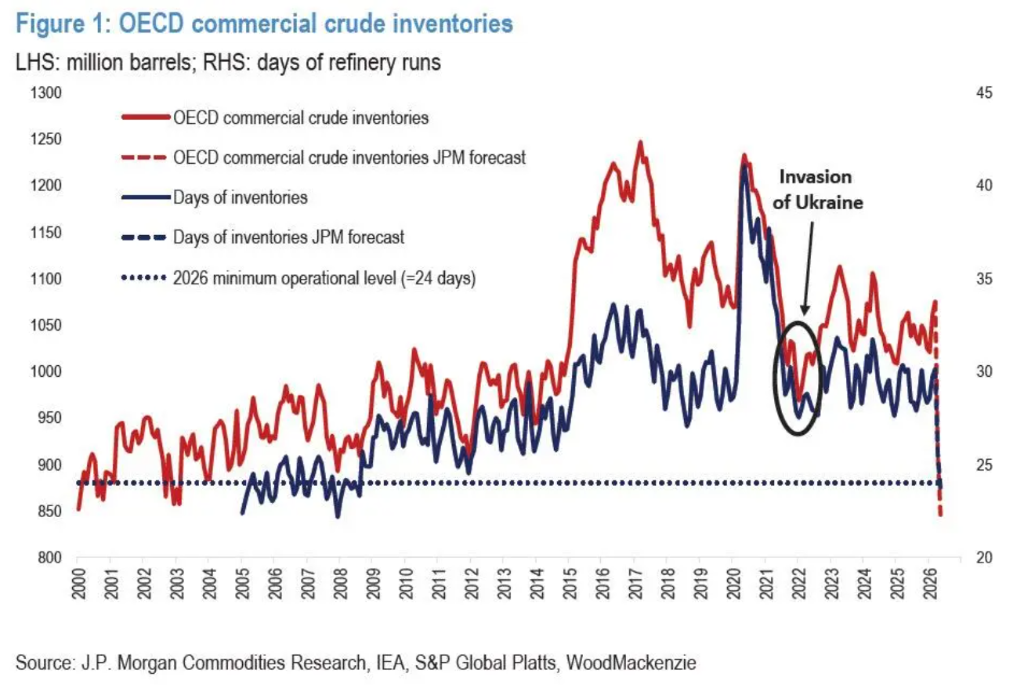

To understand this report, you must first understand a key concept: Operational Minimum.

This is the functional bottom line for inventory, not a physical "emptying".Kaneva defines it as the level at which OECD commercial inventories can cover approximately 30 days of forward refining demand, corresponding to approximately 842 million barrels.

Below this level, refinery scheduling, logistics coordination, and market liquidity will all begin to experience problems. Theoretically, the system can withstand 24 days of coverage (the minimum engineering value), but that would mean severe operational stress and a collapse in market liquidity.

It's not like the fuel tank is completely empty, but rather the fuel tank is so low that the dashboard warning light comes on—the car can still be driven, but it could break down at any moment.

Once inventory approaches this thresholdPrice, rather than inventory itself, will become the main balancing mechanism in the market.In other words, high oil prices will forcefully suppress demand, replacing inventory as a buffer.

Countdown: When will inventory bottom out? Perhaps as early as May.

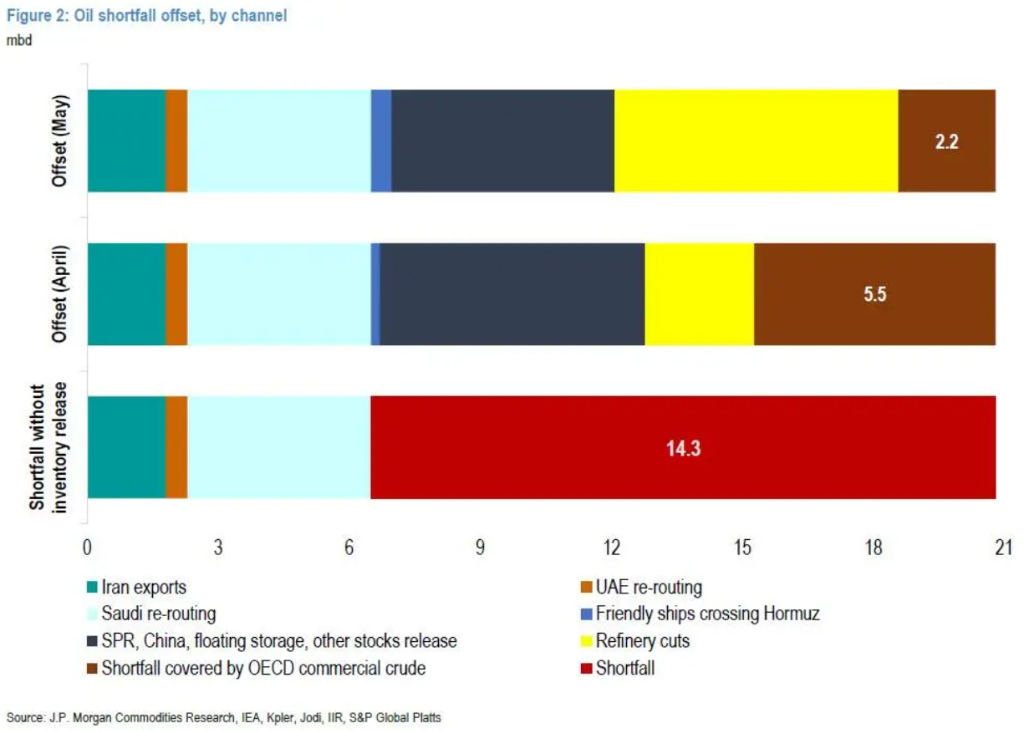

JPMorgan Chase's calculations show that the scale of this shock far exceeds that of previous ones.

The closure of the Strait of Hormuz resulted in a daily loss of effective supply of approximately 14 million barrels (14 mbd). In contrast, when the Russia-Ukraine conflict erupted in February 2022, OECD commercial crude oil inventories had already fallen to approximately 968 million barrels, equivalent to only 27 days of forward refining demand coverage, leaving them already in a vulnerable state.

This impact was larger, and the buffer was thinner. Kaneva's calculation method is as follows:

-

AprilOECD commercial crude oil inventory depletion is approximately166 million barrels

-

early May: Re-consumption approximately67 million barrels

-

Then touched842 million barrelsMinimum operating value

Demand-side pressures are already evident. The demand disruption for middle distillates and jet fuel is most pronounced in Asia, consistent with the geographical transmission path of the supply shock—Asian buyers closest to the Persian Gulf are the first to feel the pressure.

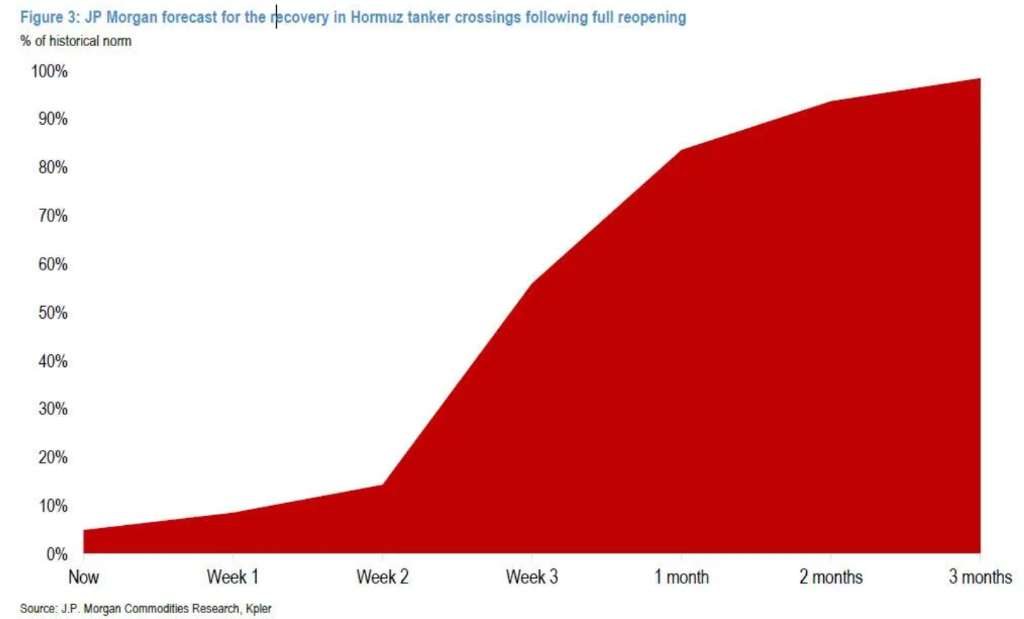

Supply Recovery: A Three-Phase Roadmap

Even if the strait reopens, supplies won't immediately resume. JPMorgan Chase has outlined a three-phase plan:

Phase 1 (Weeks 1-3): Cautious reopening, restoring approximately 6.3 million barrels per day.— Approximately half of the total output that was shut down

Even if a ceasefire agreement is reached, shipowners, port operators, and crew members will still need to confirm their safety before returning to the Persian Gulf. JPMorgan Chase estimates that shipping companies will need approximately two weeks to confirm that the risks have dissipated.

Specific rhythm:

-

Week 1: Increased Supply1.7 million barrels per dayManufacturers are tentatively resuming production to avoid hastily increasing output.

-

Week 2: Further increases2.3 million barrels per daySuccessful transit in the first week boosted confidence.

-

Week 3: Further increases2.3 million barrels per daySafety expectations are stabilizing and operational plans are gradually being implemented.

High war risk premiums, port congestion, and priority buyers (especially in Asia) rushing to take delivery will all constrain the speed of early recovery.

Phase 2 (Weeks 4-8): System normalization, recovering to 29.3 million barrels per day.

By the end of the second month, Gulf supplies had recovered to29.3 million barrels per dayIt is still about 3.4 million barrels per day lower than before the war.

Recovery progress varies from country to country:

-

Saudi ArabiaNear full recovery, supported by economies of scale and export substitution strategies.

-

UAERecovery has reached 95%, with similar dynamics, but still relies on a full resumption of operations.

-

Iraq, KuwaitRecovery is estimated at around 80%, hampered by logistics issues stemming from oil field shutdowns and restarts driven by storage tanks. Iraq's southern export system (Basra oil terminal, Kolhamaya port) has been disrupted multiple times, with alternative routes (Kirkuk-Ceyhan) only partially compensating. Kuwait Petroleum Corporation (KPC) guidance indicates that even with a ceasefire, full recovery will take months.

-

QatarOnly 60% has been restored. Ras Lafan and related facilities suffered severe damage. The repair cycle for LNG and related liquids (condensate, NGL) will be several years. Qatar Energy has quantified the losses for products such as condensate, liquefied petroleum gas, naphtha, sulfur, and helium.

Phase Three (Months 3-4): Bridging the production gap and restoring production to 99% of pre-war levels.

-

Month 3: Supply recovered to31 million barrels per dayIt is still about 1.7 million barrels per day lower than before the war.

-

Month 4: Overall recovery to pre-war levelsApproximately 99%

Saudi Arabia and the UAE will then return to full capacity. Iraq has recovered to 90%, Kuwait to 80%, and Qatar to 77%—the latter is hampered by damage to its Ras Lafan/GTL infrastructure, and full repairs are expected to take [time period missing].3 to 5 years.

Iran is another long-tail risk. The attack on the South Pars gas field has impacted the condensate and NGL supply chains. Due to the high degree of integration between gas processing, liquid recovery, and downstream petrochemical systems, the recovery of condensate and NGL production will lag behind the upstream restart. JPMorgan Chase predicts that by the end of the fourth month, Iranian production will still be approximately [missing information - likely a percentage] lower than pre-war levels.200,000 barrels per day.

Inventory rebuilding: How long will it take?

Inventories will not rebound immediately once supply recovers.

JPMorgan estimates that OECD commercial inventories will not begin to rebuild until about two months after the Straits Exchange Foundation reopens. To return to the normal levels of refining coverage 30 days ago, approximately [amount missing] will need to be replenished.150 million to 200 million barrels.

Monthly supplement30 million to 45 million barrelsBased on a rate of approximately 1 million to 1.5 million barrels per day, the complete inventory replenishment cycle is approximately...Four months.

In other words, even if the strait reopens tomorrow, it will take at least six months for the global crude oil market to truly return to normal.