Author:Wall Street CN

Goldman Sachs believes that although the market has experienced volatility, it has not yet triggered a true risk repricing.

In his latest weekly market review, Goldman Sachs' head of hedge fund business, Tony Pasquariello, emphasized...While current market risk indicators appear to be under control, the potential downside impact has not yet been fully realized. Compared to previous market turmoil, stock traders have not yet faced a true test in this round of correction.

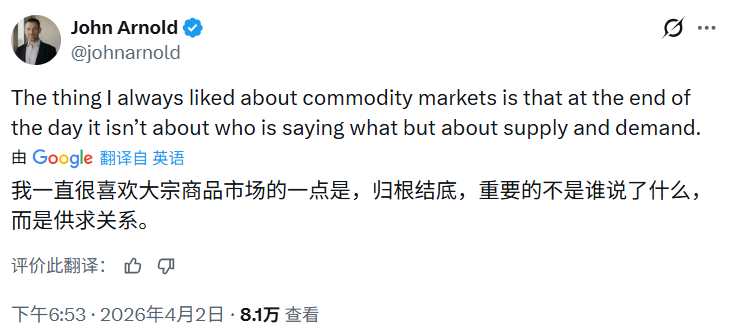

Pasquariello believes that the most apt summary of the current market situation is a quote posted on social media by John Arnold, co-chairman of Arnold Ventures:

The allure of the commodities market lies in the fact that what ultimately determines success is not what anyone says, but rather supply and demand themselves.

In addition, Pasquariello pointed out that Goldman Sachs data showed that clients reduced their positions by the largest amount in 13 years in March, and the market as a whole was in a state of large-scale net short positions in April.

Nevertheless, he still clearly advised that the primary task at present is to preserve capital and wait for the next clear entry signal. He stated:

Opportunities to make big money during a crisis often appear after the crisis.

Risk premiums are moderate, but the worst may yet be yet to come.

Pasquariello points out that, based on multiple quantitative indicators, the "intensity" of this round of market turmoil is lower than expected.

Forward volatility, the relative performance of cyclical stocks to defensive stocks, and investment-grade credit spreads have not seen the significant widening seen during historical crisis periods.

Pasquariello stated:

I'm not saying March won't be chaotic. What I mean is, stock traders haven't really been put to a full test yet.

Regarding the market's current resilience, Pasquariello has outlined two opposing interpretations.

Optimists believe that the market has not lost confidence in the sustainability of US economic growth.

Goldman Sachs strategist Ben Snider's data provides corroboration: the S&P 500's earnings per share forecast for the next 12 months has been revised upward by 6% since its peak and by 3% since the outbreak of the conflict. The continued improvement in earnings expectations provides fundamental support for the market.

Those who are concerned believe that the market is merely overly complacent, and the real shock is yet to come.

Goldman Sachs' Tony Kim points out that the last batch of oil tankers to pass through the Strait of Hormuz at the end of February have just arrived at their destinations in East Asia and Western Europe. The impact of the physical energy supply shortage is now truly taking effect, and the most explosive convex range in the energy price rise has yet to be released.

Pasquariello admitted that he was not fully confident about either the bullish or bearish viewpoints.The S&P 500 rebounded strongly this week despite rising oil prices, a combination that reflects deep-seated contradictions within the market.

The impact of physical energy shortages may soon become apparent.

Beyond subjective judgment, Pasquariello cited objective data from Goldman Sachs' own business.

Data from Goldman Sachs' prime brokerage shows that hedge fund clients sold the most shares in March in nearly 13 years. This means that the trading community significantly reduced its long exposure in March and carried a substantial short position into April.

Pasquariello believes that although this data cannot guarantee any conclusions in any direction and only represents a specific type of market participant,This indicates that the risk-reward structure at the tactical level is now relatively more balanced than it was a month ago.

He summarized the current core contradiction as follows:The market is facing the largest oil supply disruption in history, but at the same time, just one major headline news item could trigger a sharp short-covering rally.He called this state "strategic ambiguity".

Regarding volatility, Pasquariello believes that even if the VIX has peaked, both upside and downside tail risks still exist simultaneously.

- on the one handIf the crisis continues to evolve into a comprehensive economic shock, the downside risks should not be underestimated.

- on the other handOnce a "step-down" diplomatic or policy turnaround occurs, the upward trend at the tail end should not be ignored.

Based on this assessment, he maintained a conservative stance, emphasizing that the current priority is to preserve capital and reserve the capacity to respond to opportunities in the next phase.

Preserving capital is the priority; we await the post-crisis window for strategic positioning.

Looking ahead, Pasquariello believes three major themes will continue to dominate the market once the risks subside:

First, the AI investment boom will not subside.Identifying the direction is easy, but execution is much more difficult. Pasquariello stated that it will adhere to its AI leader-versus-underdog pairing trading strategy.

Secondly, the demand for financing in the power and infrastructure sectors will exceed previous expectations.A pattern similar to that of 2022 is emerging again, with the structural costs of long-term underinvestment in basic industries and a lack of supply chain diversification becoming apparent, further highlighting the strategic value of energy infrastructure.

Third, the resilience of the Japanese stock market deserves attention.Japanese stocks are cyclical assets, highly dependent on energy imports, and widely held by traders. Despite these multiple headwinds, their performance over the past month has been impressive. Pasquariello believes that the two main themes attracting capital inflows to Japan—AI and defense—will continue to drive capital inflows in the next phase.

Pasquariello concludes its market observations for the week by concluding with Darwin's theory of evolution:

Those that survive are not the strongest or the smartest, but those that are most adaptable to change.