Author:Wall Street CN

As the Middle East conflict continues to escalate and oil prices remain high, gold has experienced an unusually sharp decline in this round of geopolitical tensions. However, this unusual performance is not due to a collapse of fundamental logic, but rather stems from short-term liquidity disturbances, which are now nearing their end.

Zheshang Securities pointed out in its latest monthly report that there were no...Whether geopolitical tensions escalate or de-escalate, gold is likely to benefit. This "two-way benefit" logic...This gives it rare investment value in the current chaotic market environment.

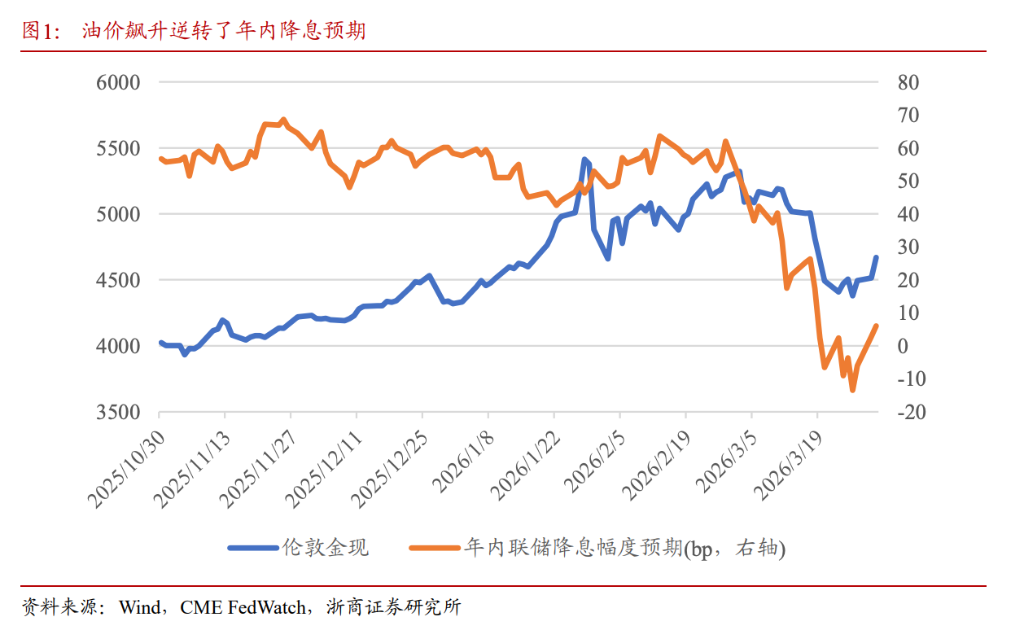

Specifically, the market previously followed the trading logic of "rising oil prices → retreat of interest rate cut expectations," but the report points out that if oil prices remain high for more than a quarter, the demand-damaging effect will begin to appear, and the economic fundamentals will weaken significantly. In other words, the higher the oil prices, the greater the risk of recession, and the expectation of interest rate cuts may actually rise accordingly. The current conflict has lasted for a month.The inflection point in the market's shift from "interest rate hike trading" to "recession trading" may be just around the corner.

Meanwhile, the trend of global central banks increasing their gold holdings remains unchanged.Türkiye's sale of gold is an isolated case. Due to its high dependence on energy imports, high gold reserves, and very low US Treasury holdings, it is essentially a forced financing for oil imports.Major European countries have maintained stable gold reserves for a long time, and these reserves serve as a guarantee for the euro's credit, thus lacking the incentive to reduce their holdings.

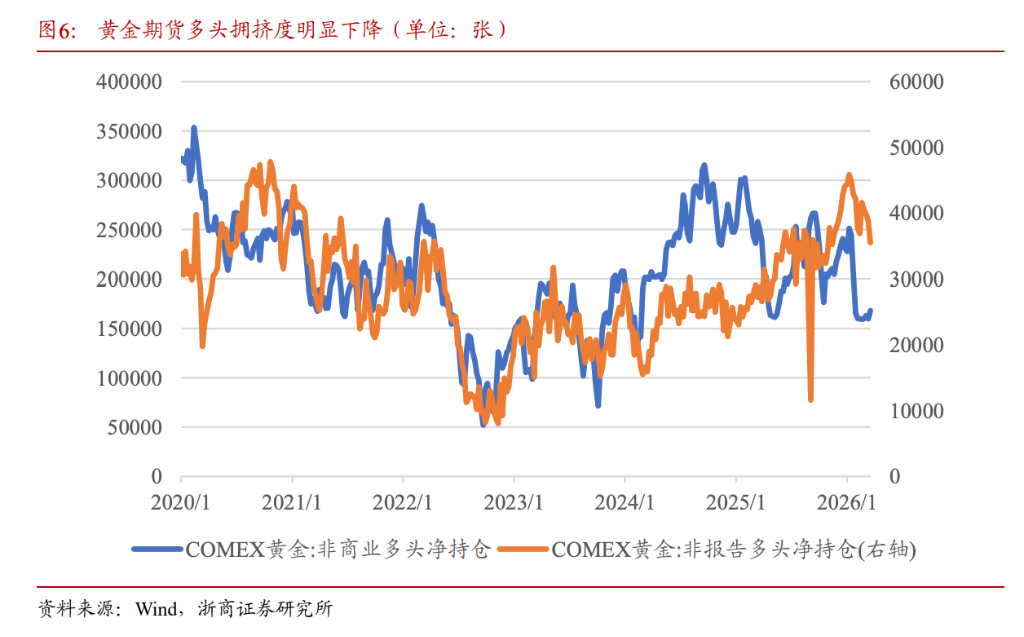

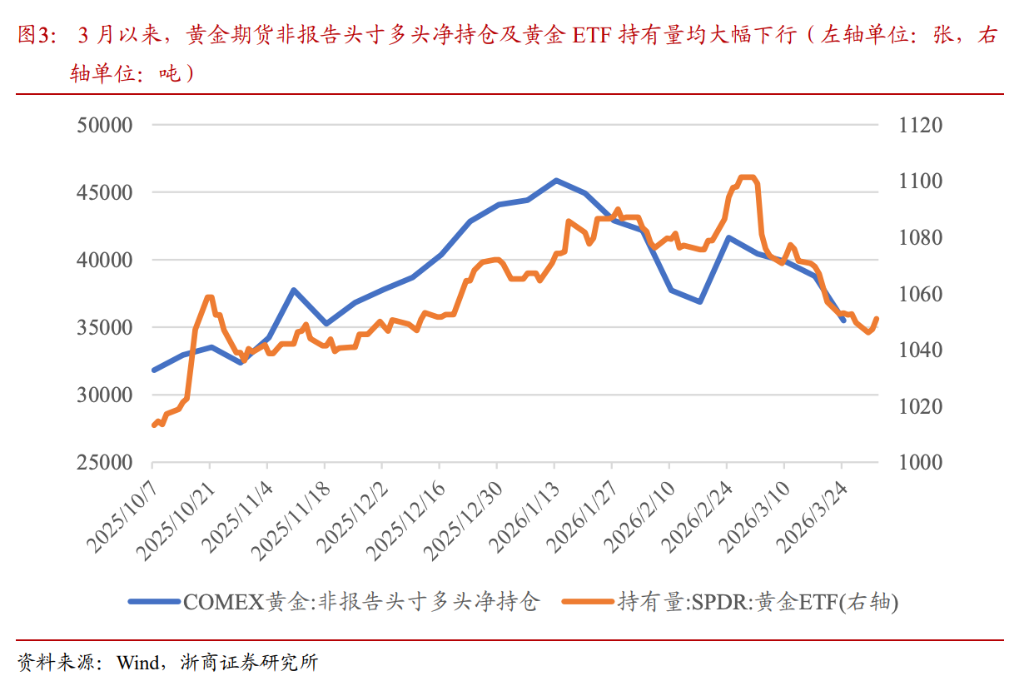

also,The improved portfolio structure also provides conditions for gold to return to fundamental pricing.Currently, both non-commercial net long positions and retail positions in COMEX gold have declined significantly compared to the previous period, indicating that the funding disturbances that previously suppressed gold are coming to an end.

Why does gold "fail" in geopolitical conflicts? Liquidity is the real culprit.

Historically,The loss of gold's safe-haven properties often occurs during liquidity crises.Examples include the 2008 financial crisis and March 2020. The underlying logic behind the initial sharp decline in gold prices during this round of Middle East conflict is similar, stemming from liquidity disturbances on three levels:

First, soaring oil prices reversed expectations of interest rate cuts, leading to an overall contraction in global liquidity.As oil prices rose rapidly, expectations for interest rate cuts this year quickly receded, and the market even began to anticipate an interest rate hike around March 20, directly leading to a tightening of the global liquidity environment and putting downward pressure on gold.

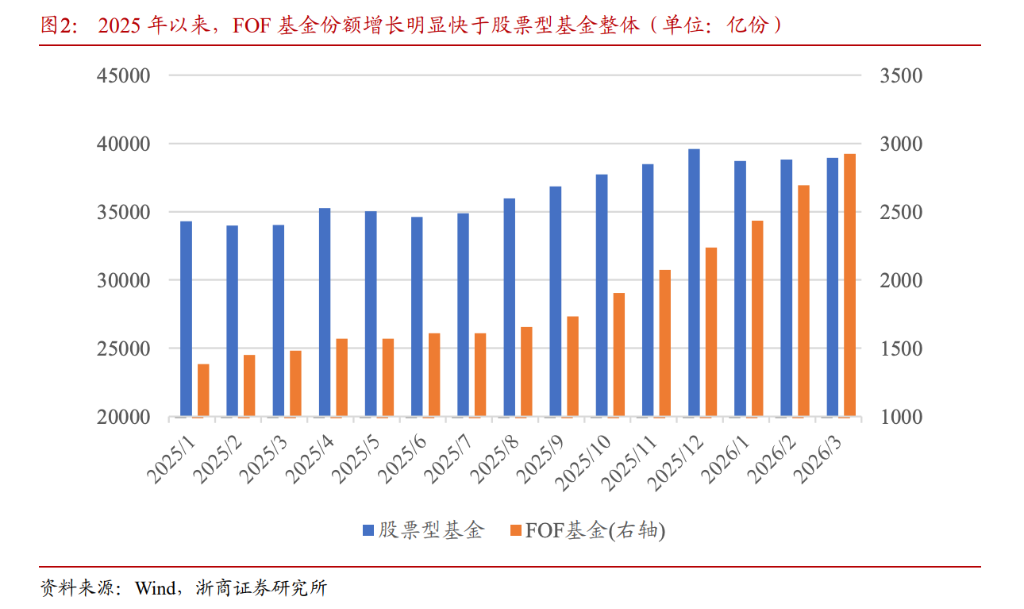

Second, the scale of multi-asset strategies expanded, leading to systemic reductions in holdings due to tail risks.The global asset price surge in 2025 fueled the rapid development of multi-asset funds (FOFs). Data shows that from January 2025 to March 2026, equity fund shares increased by 13.6%, while FOF fund shares surged by a staggering 111.2%. When tail risks materialized, multi-asset strategies systematically reduced their holdings, triggering the unusual phenomenon of simultaneous declines across different asset classes.

Third, retail investors' tendency to chase rising prices and sell falling ones amplifies the disturbance to the money supply.Gold's previous strong performance attracted a large influx of retail investors, but then saw a significant outflow during the March pullback. Data shows that both the net long positions in COMEX gold futures (non-reportable) and holdings in the SPDR Gold ETF have fallen sharply, with retail investors' chasing-the-trend and selling-the-trend behavior further amplifying the volatility in gold's liquidity.

Türkiye's central bank's gold sale is an isolated case; the global trend of central banks buying gold remains unchanged.

The recent announcement by the Central Bank of Turkey to sell gold has sparked concerns in the market that the central bank's gold-buying logic has reversed. The report argues that this concern has been over-interpreted, and that Turkey's actions have a highly specific background.

According to data cited by Reuters on Thursday,

Türkiye's energy needs are heavily reliant on imports, and rising oil prices are forcing it to need more US dollars to purchase energy..at the same time,Nearly half of Türkiye's official reserves are made up of gold, while US Treasury bonds account for a very small portion. Unable to obtain the necessary US dollars by selling US Treasury bonds, Turkey can only sell gold.

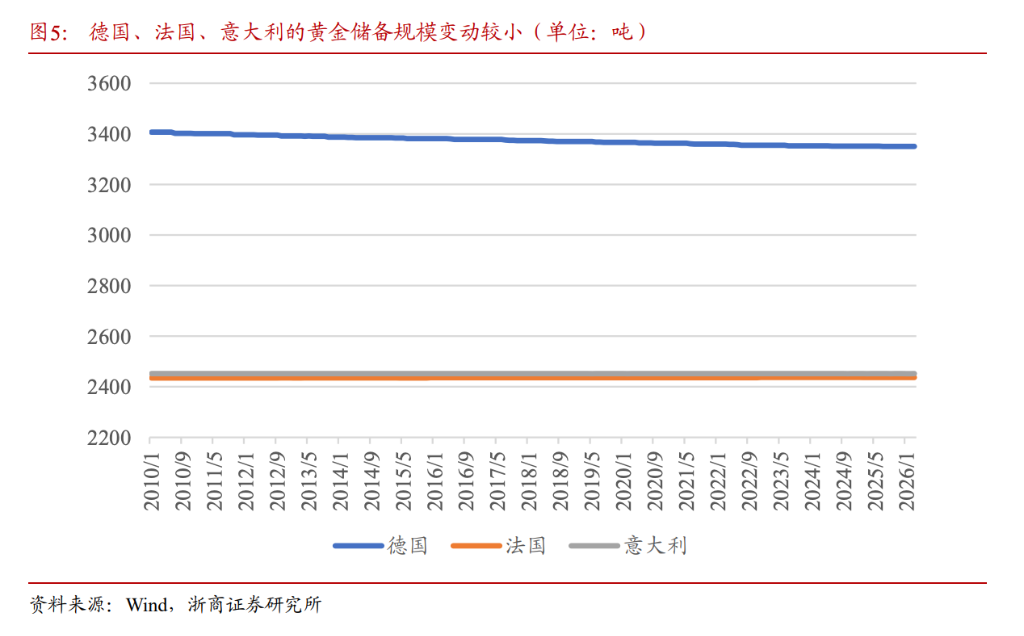

Other countries with high gold reserves and low energy self-sufficiency are mainly concentrated in Europe. Germany has 82% of its official reserve assets in gold, France 80%, and Italy 79%. However, European countries still have relatively abundant energy reserves, and gold serves as a backing for the euro's creditworthiness.

Data shows that the gold reserves of countries such as Germany, France, and Italy have remained almost unchanged in recent years. In the absence of significant liquidity pressure,European countries are unlikely to sell gold in the future, and the long-term trend of central bank gold purchases will not be reversed by the isolated case of Türkiye.

Market trading paradigms may be shifting, and gold could benefit from a two-way benefit logic.

The previous market trading paradigm was:The rise in oil prices has led to a pullback in expectations of interest rate cuts, meaning the market believes the Federal Reserve's focus is now on inflation.The US manufacturing PMI reached 52.7 in March, a recent high. Given the strong fundamentals, this trading logic is relatively sound.

However,If oil prices remain high for more than a quarter, the demand-damaging effect may begin to appear, and the economic fundamentals will weaken significantly.At that timeThe higher the oil price, the greater the risk of recession, and the more likely the Federal Reserve will cut interest rates.Given that the conflict has lasted for a month, and market expectations often precede fundamentals, if oil prices continue to remain high, the turning point in the market's shift from "rate hike trade" to "recession trade" may be just around the corner.

This creates a "two-way benefit" logic for gold:

-

If geopolitical tensions escalate furtherThe market has shifted to a recession trade, strengthening expectations of interest rate cuts, which benefits gold.

-

If geopolitical tensions cool downAs oil prices fall, expectations of interest rate cuts also strengthen, and gold benefits as well.

besides,After the previous decline, the issue of crowded positions in gold may have been largely resolved.As of March 24, COMEX gold non-commercial net long positions (roughly representing institutional investors) were at the 25.3% percentile since 2020, and non-reported net positions (roughly representing retail investors) were at the 79.9% percentile, both significantly lower than the previous period.

The improved price structure suggests that the financial disturbances that previously suppressed gold prices are coming to an end, and gold pricing is expected to gradually return to fundamental logic.