Author:Wall Street CN

In the first quarter of this year, energy storage, which had been mired in price infighting, finally began to turn around – prices rose across the entire upstream and downstream chain:

-

lithium carbonateThe price increased from 75,000 yuan/ton to 90,000 yuan/ton.

-

Copper prices break through90,000 yuan/ton

-

Lithium hexafluorophosphate prices have increased.20%

After the price increase is passed down from the upstream material supply chain, the prices of battery cells and systems are also rising:

-

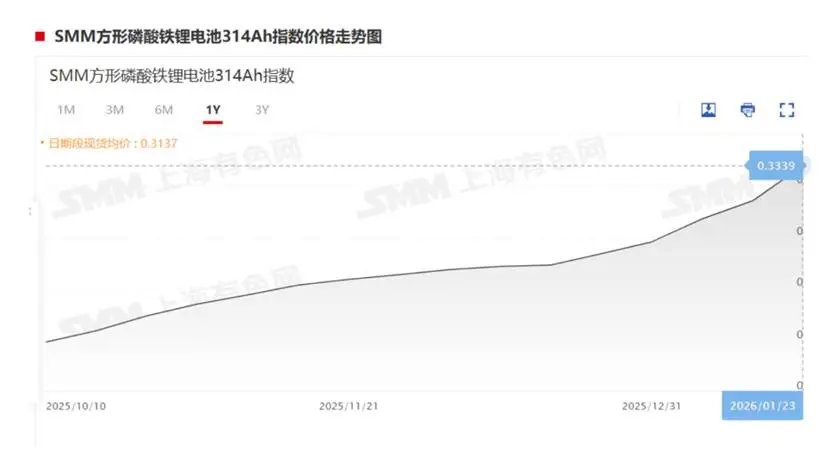

314Ah energy storage cellThe price increased from 0.31 yuan/Wh to 0.36 yuan/Wh.

-

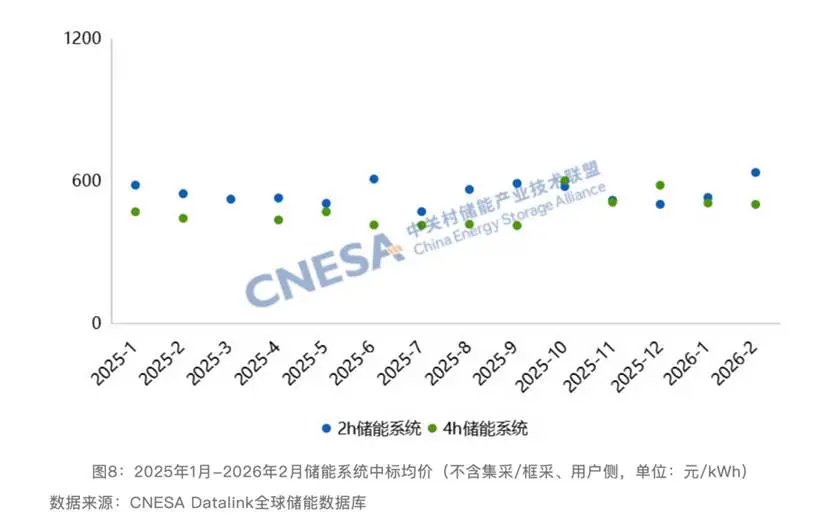

Bidding price of energy storage systemThe price increased from 0.5 yuan/Wh to 0.8 yuan/Wh.

In the past, energy storage companies, which are extremely sensitive to costs, would have denounced such price increases as "ripping off consumers." But this time, the entire energy storage industry chain has silently accepted this wave of price hikes.

To understand this, we must first understand one thing:

The biggest cost of an energy storage power station is the battery cells. For a 100MW/200MWh energy storage power station, the cost of battery cell procurement typically accounts for 50%-60% of the total investment.

Therefore, in the past few years, downstream industries have been extremely sensitive to battery cell prices. How sensitive?

A research report by CITIC Securities in December 2025 made the following calculations:

Taking a typical energy storage power station as an example, for every 0.1 yuan/Wh increase in the price of battery cells, the project's total return on investment will decrease by more than 1 percentage point.

Don't underestimate this one point. The original 8% return rate may drop directly to 6.5%, and if it rises a little more, it will fall below the 5% break-even point, and the project will not be able to make money.

When lithium carbonate prices soared in 2021, downstream users accused battery manufacturers of price gouging; when prices rebounded in 2023, some said they were "fleecing the韭菜 (a metaphor for exploiting consumers)."Battery manufacturers that raise prices are always the target of public opinion.

But this time, something unusual happened:Not only did no one criticize it, but the market was very optimistic about the trend of "both volume and price rising".

Why did the 314Ah battery cells suddenly "disappear"?

In industry terms314Ah battery cells are currently "unavailable even with money in hand".

Since the first quarter of 2026, the market supply and demand for 314Ah battery cells has reached its limit. On the one hand, large-scale procurement orders from central and state-owned enterprises have been placed one after another, with China Electric Equipment (19.8GWh), State Power Investment Corporation (7GWh), and China Huadian Corporation (12GWh) all explicitly requiring a battery cell capacity of no less than 314Ah. These large orders are like several pumps, almost draining the market of available 314Ah battery cells.

It's not that there's no stock, it's that the manufacturers "don't want to sell".

The 314Ah battery cell is stuck in an awkward position.Supply is contracting, while demand is still rising.

Battery manufacturers on the supply side are generally no longer expanding their 314Ah production capacity, but instead shifting to 500+Ah. However, the new 500+Ah capacity will not be released on a large scale until the second half of 2026, and will still require downstream certification.

On the demand side, downstream energy storage projects continue to generate strong demand, especially large-scale procurement orders from central and state-owned enterprises, which maintain a strong demand for mature 314Ah battery cells. As a result, supply contraction coupled with rigid demand has led to a structural shortage of 314Ah battery cells.

The reason why battery companies are no longer expanding their 314Ah production capacity is quite simple.You don't make much money.

SMM's calculations show that the theoretical cost of a 314Ah battery cell had climbed to 0.3683 yuan/Wh in January 2026, but the market transaction price was still hovering around 0.33 yuan/Wh at that time, so every sale resulted in a loss.

Currently, leading manufacturers are quoting prices close to 0.4 yuan/Wh, but there is still a long way to go before reaching a price that is comfortable for all players.

Can the demand side absorb this price increase?

Why is no one criticizing the recent price increase in energy storage? The core reason is that the demand side has made the financials work.

January 2026,Document No. 114 jointly issued by the National Development and Reform Commission and the National Energy AdministrationThis marks the first time that the "capacity value" of energy storage has been established at the national level.

This means that previously, energy storage power stations, being purely cost-based, were extremely sensitive to battery cell prices. Now, independent energy storage power stations are beginning to have diversified revenue structures, and the actual surge in demand can naturally absorb the cost increases from raw material price hikes.

Over the past three years, the price war has been so fierce that everyone is suffering. Almost no one in the entire industry chain, from material manufacturers to battery manufacturers to integrators, has made a lot of money.

Downstream power plants also understand a principle—Low price means low quality, unfinished projects, and projects where problems arise and no one can be found to help.

After the first major test of energy storage power stations, and after learning from the lessons of fires and frequent malfunctions in the first two years, downstream users have realized: "Cheap prices are great for a while, but after-sales service is a nightmare."

Therefore, this price increase signals that the industry is shifting from price wars to value wars.

At the same time, we can see that upstream producers are simultaneously reducing production at one end and expanding production at the other – reducing production at the low end and expanding production at the high end.

At the end of 2025, five leading companies simultaneously announced a production halt for maintenance.Hunan Yuneng, Defang Nano, Longpan Technology, Wanrun New Energy, and Fulim PrecisionThey all acted in unison, "pressing the pause button" during the annual price negotiation window.

They are inspecting old production lines and inefficient capacity. Taking this opportunity to stop not only gives them a reason to raise prices, but also completes the clearing of excess capacity.

At the same time, Fulim Precision announced an investment of 6 billion yuan to build a 500,000-ton high-end energy storage lithium iron phosphate plant, and Longpan Technology invested 2 billion yuan to build a 240,000-ton high-density lithium iron phosphate plant.

The expansion isn't about "homogenized production capacity," it's about next-generation technology:High density, long cycle life, and optimized low-temperature performance.

Therefore, reducing production is to prevent current orders from resulting in losses; expanding production is to ensure that future orders will generate more profits.

Who profited from the price increase?

The money raised in this round of price increases did not flow evenly into everyone's pockets. Along the industry chain, the flow of profits exhibits a clear K-shaped divergence—Upstream mining companies and leading material manufacturers are the biggest winners, while battery manufacturers also benefit.

Upstream mining companies are making easy money.In February of this year, Zimbabwe, the world's fourth-largest lithium producer, suddenly announced a suspension of all exports of raw lithium ore and lithium concentrate, including goods already in transit. This policy directly exacerbated the global shortage of lithium carbonate, causing the price of lithium carbonate to break through 150,000 yuan per ton.

Chinese companies with lithium resources in Zimbabwe, such as China Mineral Resources, Huayou Cobalt, and Yahua Group, have been less affected by export restrictions because they own beneficiation plants or lithium sulfate production lines there. Instead, they have benefited from rising prices. Coupled with geopolitical factors driving up freight and insurance costs, mining companies have become the first beneficiaries of this round of price increases.

Leading material manufacturers will recover. By the end of 2025, leading companies such as Hunan Yuneng, Defang Nano, Longpan Technology, Wanrun New Energy, and Fulim Precision will tacitly announce simultaneous production shutdowns for maintenance during the annual price negotiation window.By temporarily reducing supply, the company conveys its demand for price increases to downstream industries, creating room for negotiation on raising processing fees.

The effects were immediate. In the first quarter of 2026, leading material manufacturers successfully raised processing fees, coupled with a supply shortage of high-end, high-pressure products, resulting in some leading companies achieving capacity utilization rates exceeding 90%. Companies such as Hunan Yuneng and Defang Nano are expected to return to profitability in the first quarter of 2026.

The tail material factory is drinking soup.

Not everyone can reap the benefits of this wave.Although the overall capacity utilization rate of the lithium iron phosphate industry has rebounded, the operating rate of many small and medium-sized enterprises is still not high.

The reason is that technology cannot keep up. The core driver of this round of price increases is the structural shortage of high-end, high-density products, while most companies are unable to upgrade to third- or fourth-generation products and can only watch helplessly as they struggle with low-end production capacity.They can only "drink the soup" of the price increase, or even get nothing at all.

How long will this round of price increases last?

At least until the fourth quarter of 2026.

According to InfoLink Consulting,The tight supply-demand balance will continue until 2026.The price of mainstream battery cells is expected to remain above 0.3 yuan/Wh, with the price center rising by more than 15% compared to 2025.

Specifically, we can judge this from three indicators:

First, look at the supply.Leading companies are operating at over 95% capacity, indicating insufficient supply elasticity. Low-end capacity is still being cleared out and is unlikely to resume large-scale production in the short term.

Second, consider the needs.Demand for energy storage cells is growing at a rate exceeding 50%, and demand for power batteries is also robust. The structural shortage of 314Ah cells is unlikely to ease in the short term.

Third, examine the policies.The capacity compensation policy outlined in Document No. 114 will be implemented until the end of 2026, and downstream acceptance will not suddenly decrease.

In summary, the upward trend in lithium iron phosphate prices is expected to continue at least until the fourth quarter of 2026, and the strong price of energy storage will persist throughout the year.

Is a price increase a good thing or a bad thing?

This is a good thing for the industry.

This shows that the industry has finally learned to self-regulate. Previously, everyone was trapped in..."Expansion - Price War - Losses"It's a vicious cycle. Now finally someone knows when to step on the brake and when to step on the gas.

An industry that knows when to apply the brakes has a price floor. An industry that knows when to apply the accelerator has a price ceiling.

Because everyone knows that an industry that proactively reduces production, rationally expands production, and sets prices in an orderly manner is much healthier than an industry that only engages in price wars.

Energy storage prices have risen, but the energy storage industry is finally starting to become valuable.

This article is sourced from: