Author:Wall Street CN

1. Why are central banks selling gold?

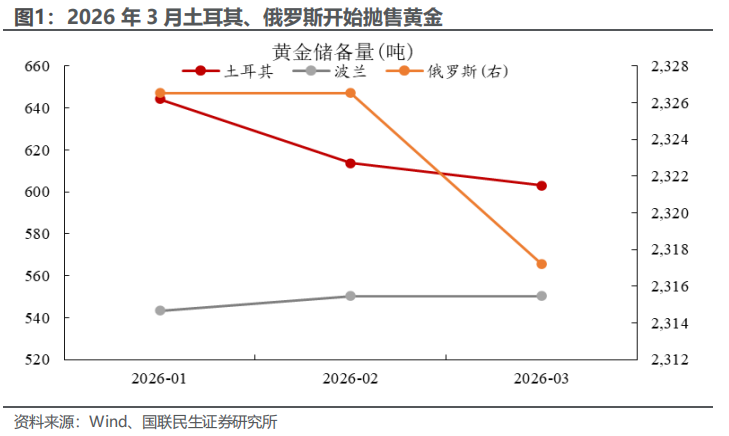

Since the outbreak of the conflict between the US and Iran, the market has paid close attention to the gold sell-off by some countries, and the logic of the gold bull market supported by "central bank gold purchases" has begun to be questioned.As shown in Figure 1, in March 2026, the central banks of Turkey and Russia began selling gold, while Poland planned to sell gold to support its defense. So, why are some central banks "passively" selling gold? Does central bank gold selling really negatively impact gold prices?

We believe that the recent gold sales by some central banks are more "tactical" than "strategic," for the following three main reasons:

The first is institutional behavior of "following trends".In essence, central banks also play the role of "institutional investors" in the gold market. Take the Central Bank of Turkey as an example: when gold prices are consolidating, the Turkish central bank tends to sell gold; conversely, when gold prices are rising rapidly, the Turkish central bank accelerates its gold purchases.

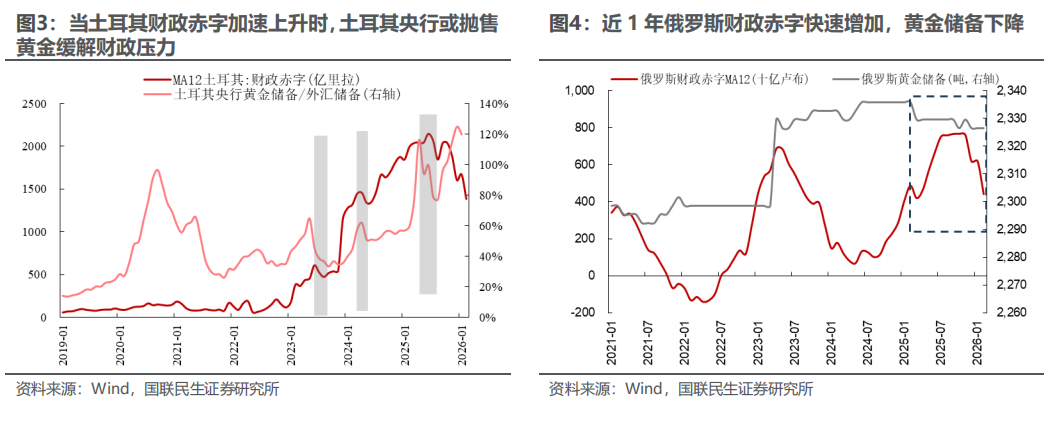

Second, the fiscal deficit rose rapidly in the short term, and the central bank was "passively" selling gold to meet liquidity expenditures.For example, in Turkey, after its fiscal deficit rose rapidly, the central bank may be "forced" to sell gold in exchange for US dollars; similarly, in Russia, after its fiscal deficit rose rapidly in 2025, the Russian central bank also began to "passively" reduce its gold holdings in exchange for financial support for the Russia-Ukraine conflict.

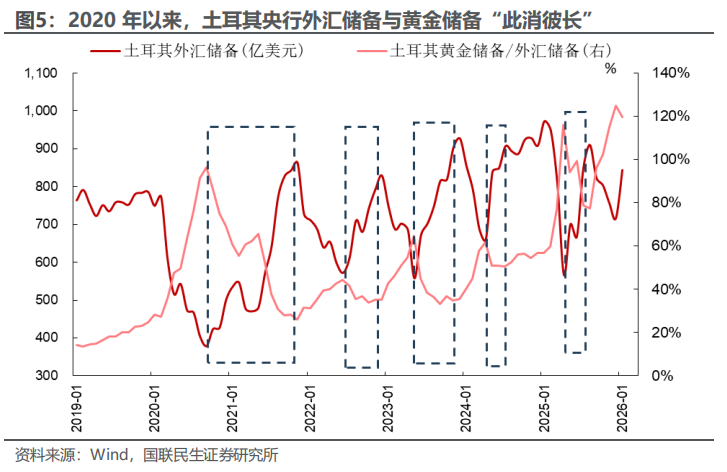

Third, there is the ebb and flow between the central bank's gold reserves and foreign exchange reserves.Taking the Central Bank of Turkey as an example, the transmission path of the seesaw effect between "foreign exchange reserves" and "gold reserves" is as follows: oil price supply shock → rising oil prices → exacerbated current account imbalance → accelerated lira depreciation → central bank sells gold to increase foreign exchange reserves. With the outbreak of the US-Iran conflict, and concerns that the rapidly widening trade deficit would lead to excessive lira depreciation, the Central Bank of Türkiye sold nearly 60 tons of gold in March.

2. Why the grand narrative of "long-term gold price increase" has not changed.

We believe the main trend of "long-term gold price increase" has not changed, and the core reasons include four dimensions.:

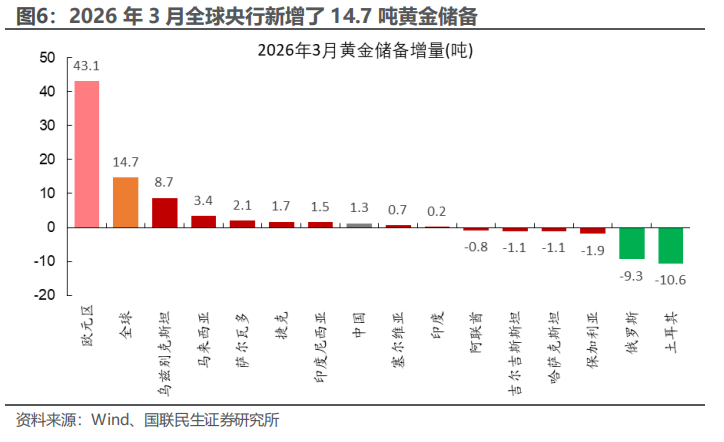

Firstly, the world was still "net buying" gold in March, and the reduction of holdings by some central banks did not affect the main theme of "central bank gold purchases".Following the outbreak of the US-Iran conflict, global central bank gold purchases reached 14.7 tons in March 2026, with the Eurozone being the main buyer (43.1 tons). Other central banks increased their gold holdings far more than Turkey and Russia reduced theirs. In conclusion, the reductions in gold holdings by some central banks do not affect the overall trend of central bank gold purchases.

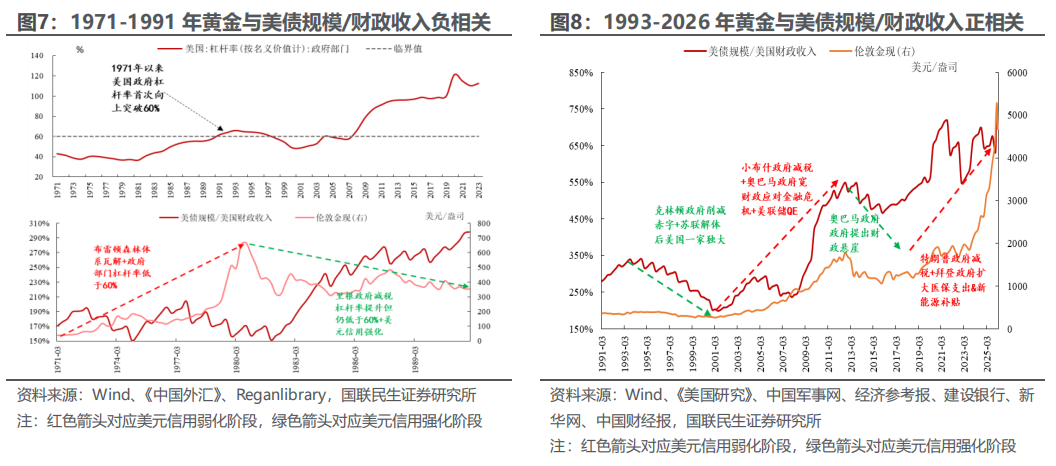

Secondly, the long-term trend of weakening dollar credibility has not been reversed.If we liken the United States to a "company," then the dollar's creditworthiness is analogous to the company's "debt repayment ability." Debt expansion in the US government before 1991, with a leverage ratio below 60%, can be considered "benign expansion," while debt expansion after 1991, with a leverage ratio exceeding or approaching 60%, can be seen as "lax fiscal discipline." The former corresponds to strengthened dollar creditworthiness, while the latter corresponds to weakened dollar creditworthiness. After the Trump administration passed the "Bigger & Better Act" in 2025, the US government's leverage ratio exceeded 110%, and the trend of weakening dollar creditworthiness continued.

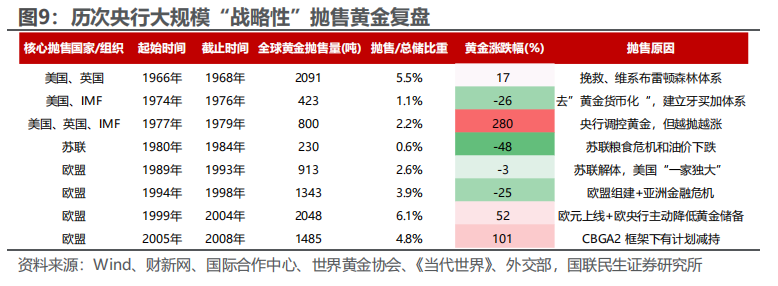

Third, even if global central banks engage in a long-term "strategic" sell-off of gold, the price of gold can still rise.As shown in Figure 7-8, the periods of 1977-1979 and 1999-2008 coincided with a period of weakening US dollar credibility (see the previous paragraph for the method of dividing these periods). Even with large-scale gold sales by core economies such as the US and the EU, gold still maintained an upward trend. Given the weakening of the US dollar's credibility, even if some central banks reduce their holdings in February and March 2026, causing short-term fluctuations in gold prices, the upward trend may not be reversed.

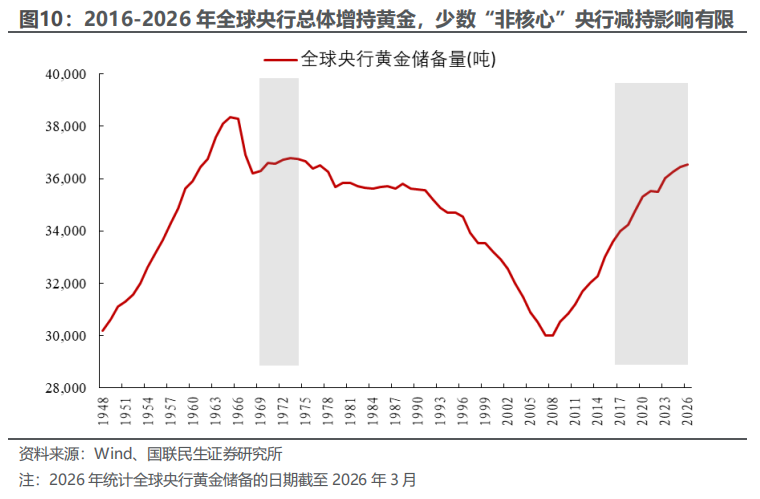

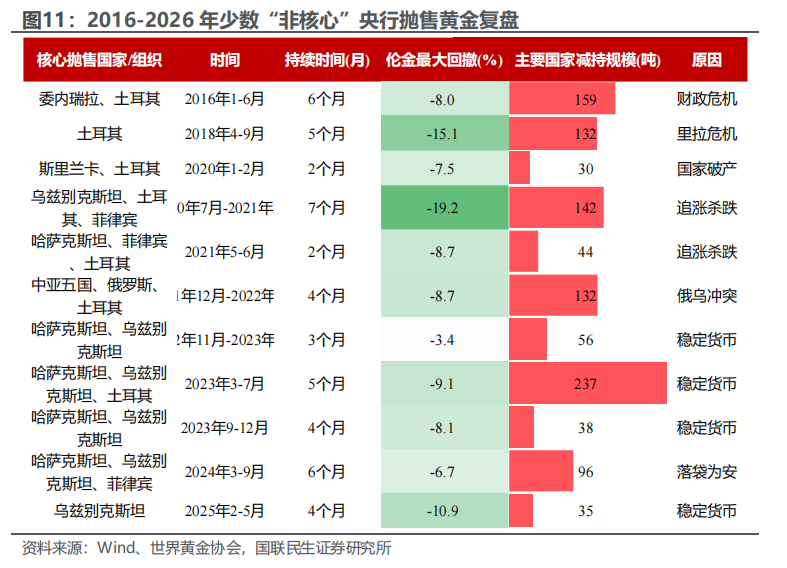

Fourth, short-term "tactical" selling of gold by "non-core" central banks does not affect the long-term upward trend of gold.Taking the period of weakening US dollar credit from 2016 to 2026 as an example, global central bank gold reserves increased by a net 3,517 tons. Although the short-term gold sales by "non-core" central banks such as Turkey, the five Central Asian countries, and the Philippines caused a certain pullback in gold prices (see Figure 11), they did not reverse the general upward trend of gold prices from 2016 to 2026.

In summary,usThe article argues that the recent gold sales by a few "non-core" central banks, such as Turkey and Russia, were "tactical" reductions based on the choice of "following the trend" and "temporarily alleviating the fiscal crisis," and do not affect the long-term logic of "weakening dollar credit → increased central bank gold purchases → consolidation of the gold price upward trend."

Risk warning:

The Federal Reserve may begin pricing in rate hikes in 2026, moving away from its expectation of no rate cuts.The closure of the Strait of Hormuz may become a medium- to long-term issue, and the continued rise or high volatility of oil prices could impact the global economy.With Warsh poised to become the Federal Reserve Chairman, there is a possibility that the Fed may accelerate its balance sheet reduction program.

This article is sourced from: