Author:Wall Street CN

The turmoil in the private lending market has spread from BDCs (Business Development Companies) to the broader lending ecosystem. While JPMorgan CEO Jamie Dimon believes it does not yet pose a systemic risk, a recent research report from Barclays and UBS reveals a overlooked blind spot:The private lending and mortgage-backed securities (CLO) markets are deeply intertwined.

With Business Development Companies (BDCs) facing massive redemptions, private credit valuations may be forced to shift from "model-based pricing" to "market capitalization pricing," and investors should be wary of the net asset value impact from falling prices of underlying assets (especially software/SaaS loans).

Meanwhile, the spread on unsecured BDC bonds has widened significantly, and the pricing of privately placed credit CLOs has not yet fully reflected this reality. Barclays points out that BDCs are highly comparable to Single-A CLOs.With rising default rates on software loans, the CLO market is highly likely to become the next risk trigger.

UBS warns that rising private lending defaults will lead to a sharp decline in leveraged loans and CLO issuance, and that due to the high degree of overlap between investors in the public and private lending markets,Liquidity pressures could quickly spread to the broader public credit market.

The starting point of the crisis: BDC redemption wave and valuation transparency crisis

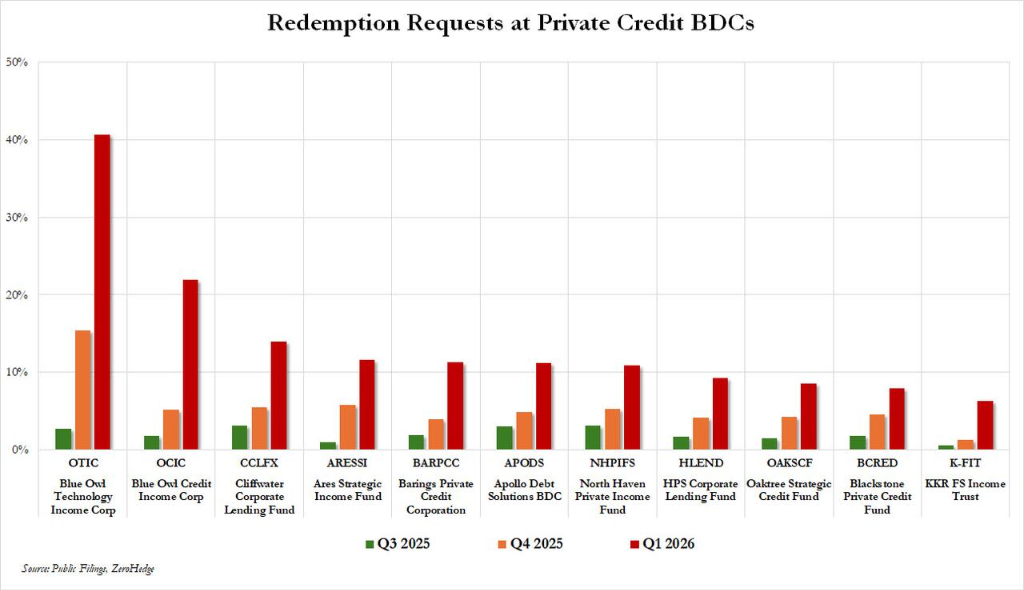

Private equity credit-related assets have been sold off over the past two months.

Redemption requests from investors in Blue Owl's two private credit funds (Technology Income Fund and Credit Income Corp) reached as high as 41% and 22% respectively, causing many listed private credit/BDC securities to hit record lows.

JPMorgan CEO Jamie Dimon warned that "the lack of transparency and rigorous valuation of loans in private lending has led to current losses exceeding what would be expected under normal circumstances."

Dimon also warned that insurance regulators will sooner or later require stricter ratings or write-downs, and retail investors will resort to legal action if problems arise.

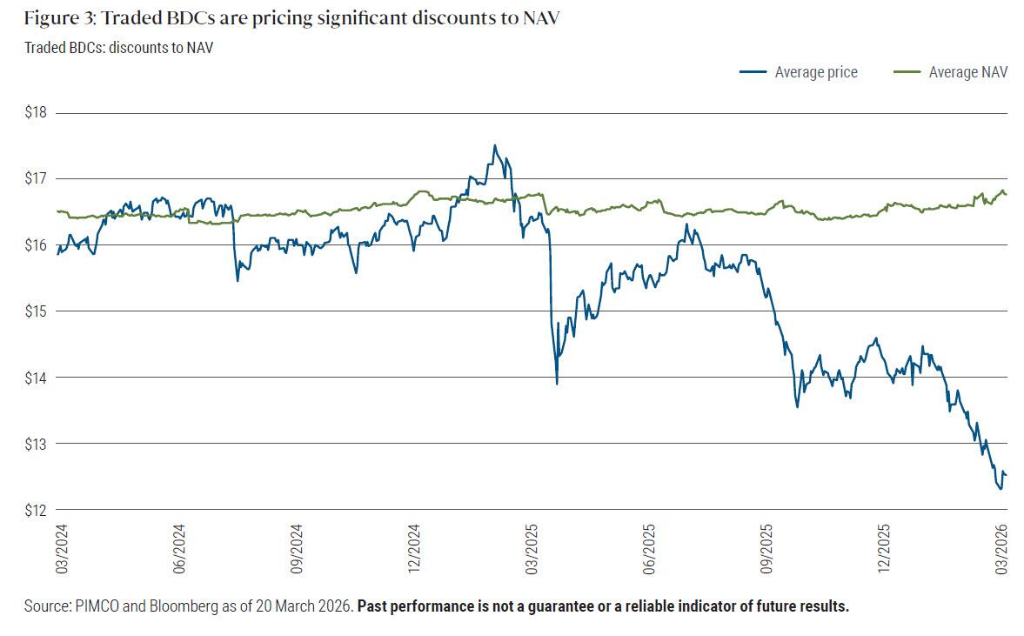

Pimco's data clearly shows that publicly traded BDCs are trading at a significant discount to their net asset value (NAV), and the valuation gap between the public and private markets continues to widen.

Nevertheless, Dimon also stated that private lending "may not" pose a systemic risk because of its relatively limited size within the overall credit market—a judgment that echoes a previous Goldman Sachs report.

Barclays warns: CLO pricing is severely out of touch with reality

However, a Barclays report suggests that Dimon's assessment may have overlooked the deep-seated connection between private lending and derivatives markets such as CLOs.

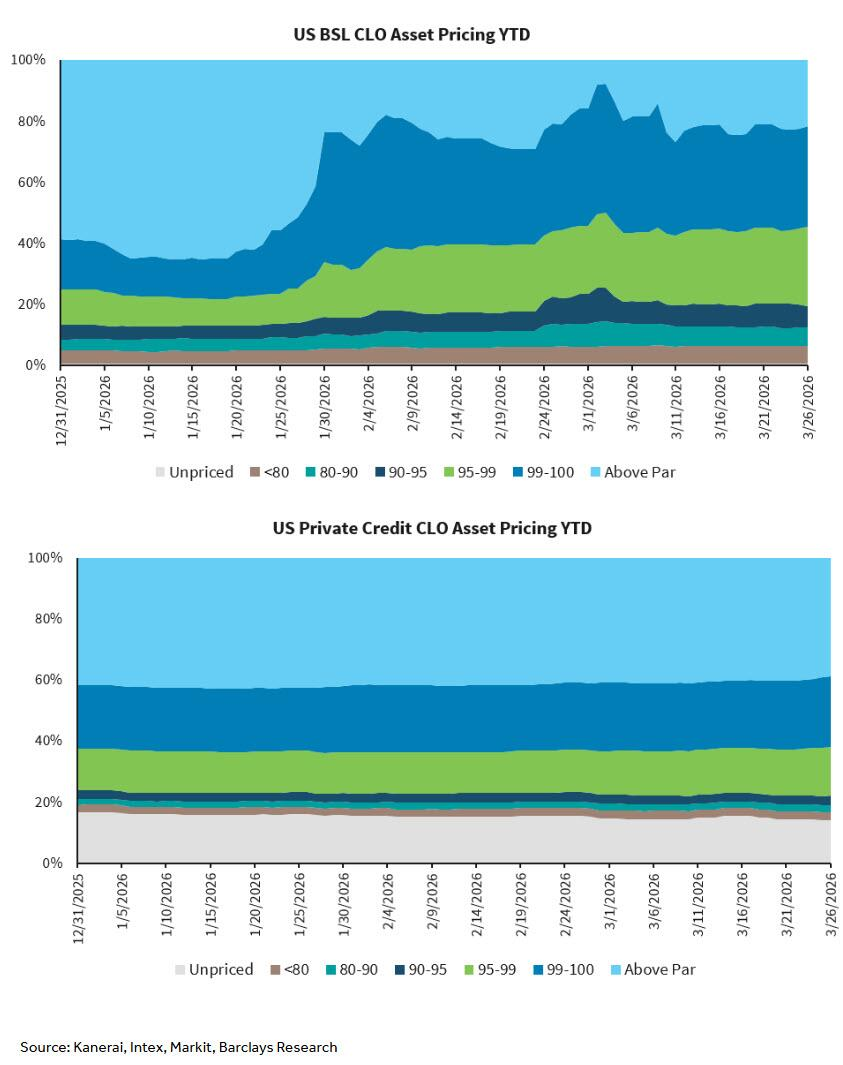

The bank's credit analyst, Gavin Zhu, pointed out that compared to the massive sell-off of broad syndicated loan (BSL) CLO assets, private credit CLOs have not yet seen a similar situation.

So far this year, private credit CLO pricing has seen minimal changes: loans above par value have only decreased from 42% to 39%, loans below 95% have only increased from 7% to 8%, and approximately 14% of loans remain unpriced.

In contrast, the percentage of loans with a face value of 95 or higher in the US has plummeted from 59% to 22%, while the percentage of loans with a face value below 95 has risen from 13% to 19%. Barclays believes that...BDC's current pricing is severely out of touch with the realities of the CLO market.

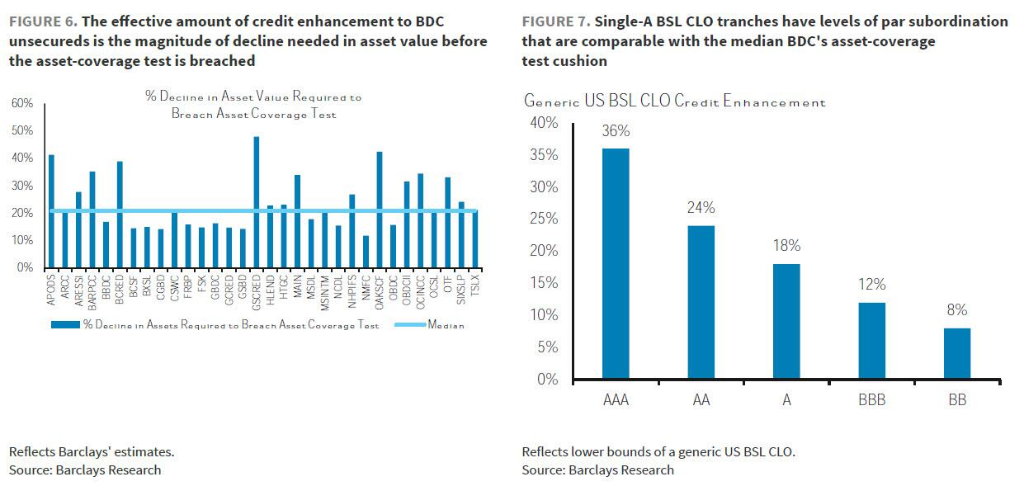

BDC asset coverage testing has become a key constraint, with a single Class A CLO serving as the best benchmark.

To quantify the relative value of BDC unsecured bonds, Barclays has developed a systematic comparative analysis framework.

Barclays points out that the spread of BDC unsecured bonds has widened by 80 basis points (bp) so far this year, currently hovering around 260 bp, significantly underperforming the investment grade (IG) index (which has only widened by 15 bp to 92 bp). To find a suitable relative value benchmark, Barclays has turned its attention to CLOs.

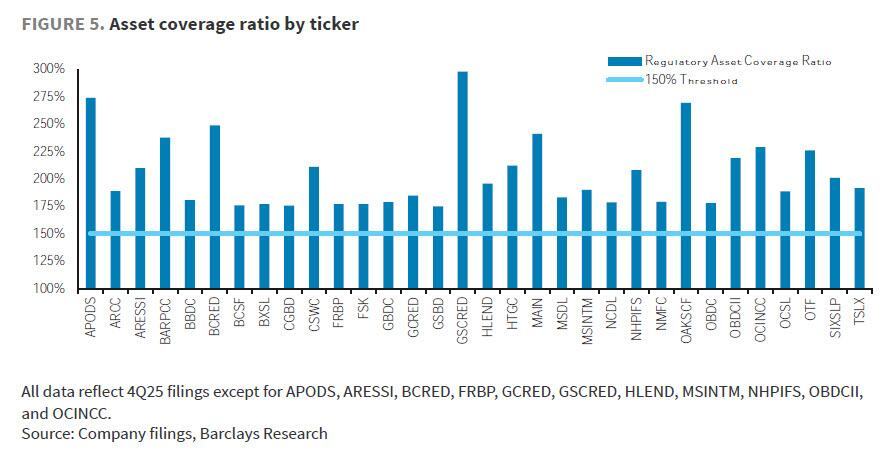

Under the 1940 Act, BDCs are subject to a strict asset coverage test, which requires that their assets cover at least 150% of their debt (i.e., a leverage ratio capped at 2x).

If it defaults, BDC will be unable to issue new debt or pay dividends, and may even lose its Regulated Investment Corporation (RIC) status and become a cash taxpayer. Currently, the average/median regulated asset coverage ratio of investment-grade BDCs is 205%/191%.

Barclays estimates that for BDC assets to reach the 150% threshold, the median value of BDC assets would need to fall by 21%.This attachment point is closest to the Single-A layer in the standard BSL CLO structure.Therefore, a single-A-rated CLO is the best benchmark for assessing the relative value of BDC unsecured bonds.

Quantitative Impact and Relative Value Assessment of Software Loan Sell-off

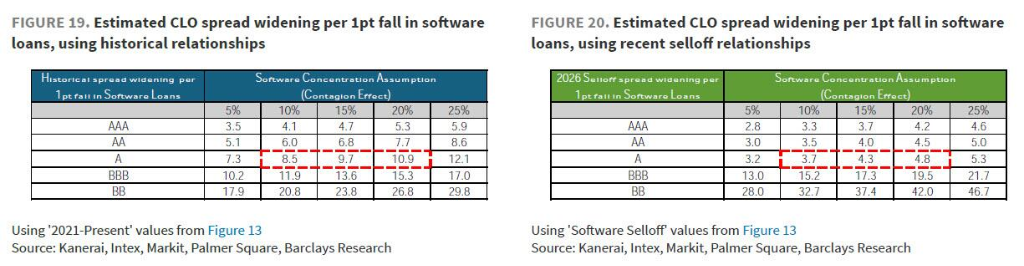

Barclays has conducted a quantitative assessment of the devaluation of software/SaaS assets caused by AI disruption.

In the US BSL CLO, direct software risk exposure is approximately 11-13%, and combined exposure is approximately 22%. In the current environment, assuming a 1-point decrease in software loan prices (with a corresponding 0.2-point decrease in non-software loan prices), the spread for a single A-rated CLO will widen by 4 basis points.

In comparison, BDC has a higher software exposure (approximately 20%). Barclays estimates that under the same shock, the spread of BDC unsecured bonds should widen by 4.8 basis points (approximately 20% higher than CLOs).

The research report states that, based on actual market performance:Recently, the spread of single-A-rated CLOs has widened by about 20bp to 195bp; while since January, the spread of BDC unsecured bonds has widened by nearly 75bp to 270bp on a Z-spread basis.

According to Barclays' model, a 20bp widening for a single A-rated CLO implies a 24bp widening for BDC. This means that BDC unsecured bonds have substantially underperformed by approximately 50bp compared to single A-rated CLOs. As investors search for the next credit weakness,Attention will inevitably turn to the CLO market, which has not yet been severely impacted.

UBS: The transmission path of the private lending crisis to CLOs and the public markets

In its latest report, UBS's credit team provided systematic answers to seven core questions raised by clients, three of which directly relate to risks for CLOs and the broader market.

Question 1: What are the potential impacts of rising private lending losses on the structured finance market?

UBS projects that leveraged loan issuance will contract by approximately 20% to $360 billion in 2026, while CLO issuance will fall to approximately $150 billion from $208 billion in 2025. Under a tail-risk scenario, leveraged loan issuance could decline by 50-75%, and CLO creation would further shrink to $100-110 billion.

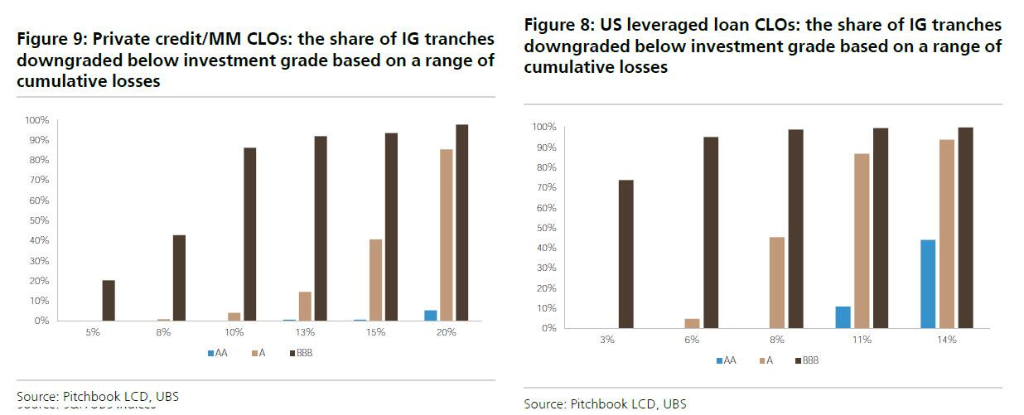

Regarding credit quality, UBS analysis shows that approximately 11-12% of leveraged loan portfolios in the US and Europe are in high-AI disruption risk sectors with lower ratings, of which about 8% face the risk of being downgraded to CCC rating within the next two years. This will increase the CCC concentration in CLO portfolios, which is currently at 4.5-5.5% and is approaching the upper limit of 7.5%.

Regarding rating stability, S&P stress tests show that the loss threshold leading to a downgrade on average BBB rating is in the low to mid-single digits for leveraged loan CLOs and in the high single digits for mid-market CLOs. UBS's baseline/tail scenario loss forecasts are: 2.6%/6.75% for US leveraged loans and 7%/12.4% for private credit in 2026, implying a substantial risk of rating downgrade within the next year.

Question 2: What are the spillover channels from private lending to the public lending market?

UBS identified four main transmission channels:

- Investor overlap: Insurance companies, foreign investors, and retail investors all have significant holdings in both private and public credit markets;

- BDC holds syndicated loans: The BDC portfolio holds an average of about 10% exposure to syndicated leveraged loans, which may be sold off more aggressively should net redemption pressure arise.

- Valuation Relevance: Private credit valuations are highly correlated with global leveraged loan valuations, with the overlap exposure (by debt weight) between European leveraged loan portfolios and US leveraged loan names reaching approximately 50%.

- Issuance pattern correlation: Historically, the issuance patterns of leveraged loans in the United States and Europe, as well as high-yield bonds in the United States, have shown a high degree of correlation.

Question 3: How will the valuation of a private BDC evolve when it faces redemption pressure?

BDCs account for one-third of private credit investment assets (approximately $500 billion, representing about $1.5 trillion of the total), with two-thirds of these BDCs being private, non-trading vehicles, which bear the majority of the redemption risk.

UBS believes that once redemption pressures begin to impact BDC liquidity, private credit valuations will shift from a "model-marked" framework to a more traditional "market-marked" approach. Historically, B3/B- rated loans traded at $90 during the Fed's tightening cycle in 2022-23, briefly fell to $80 during the COVID-19 pandemic, reached the mid-range of $85 during the high-yield shale oil crisis, and fell to the mid-range of $50 during the financial crisis.

UBS believes that these historical data points can serve as a reference range for the evolution of mark-and-price strategies in the private credit portfolio market.

CLOs are the next domino in the private lending crisis.

Based on the analyses of Barclays and UBS, the logical chain is clear:

First layer:The disruptive risks posed by AI from software/SaaS companies continue to erode the asset quality of BDC, leading to a significant widening of the spread on BDC's unsecured bonds and a surge in redemption pressure.

Second layer:There is a deep structural link between BDC and CLO, but the current pricing of private lending CLOs hardly reflects any pressure, and this valuation gap will eventually narrow.

Third layer:Once CLO pricing aligns with reality, it will trigger a chain reaction including CCC rating downgrades, OC testing pressure, and a contraction in CLO issuance, which will then be transmitted to the broader public credit market through channels such as investor overlap and valuation correlation.

As Barclays pointed out,As investors search for the next weakness in the credit markets, they will inevitably turn their attention to CLOs—a market that has so far been largely unaffected by the collapse of BDCs.

UBS further warned,If AI continues to disrupt the software industry and, coupled with a broader economic downturn, the private lending crisis will not only worsen but will also spread to the entire public lending market, using CLOs as a springboard.