Author:Wall Street CN

While the global metals market's attention is still focused on aluminum production capacity in the Gulf region, a disruptive impact on the global steel supply and demand landscape is being systematically underestimated.

According to CCTV News, Israeli Prime Minister Benjamin Netanyahu said on April 4 that the Israeli military had attacked Iranian steel and petrochemical plants that day, destroying 70% of Iran's steel production capacity.

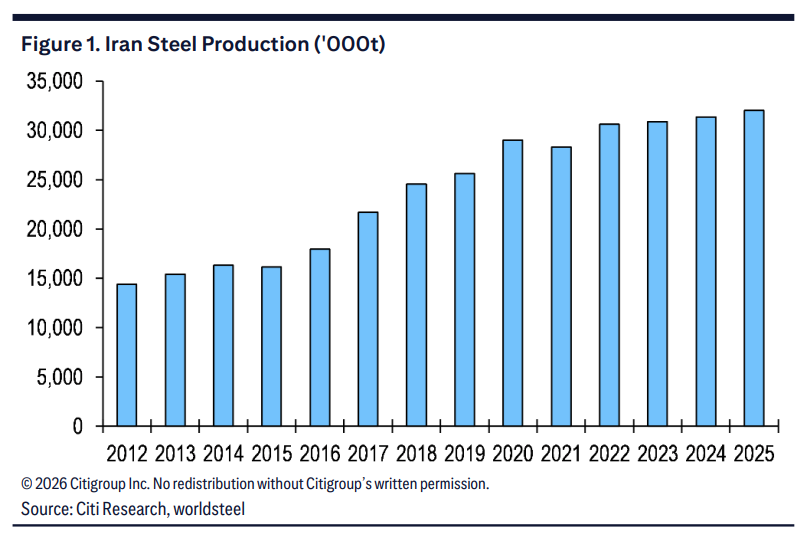

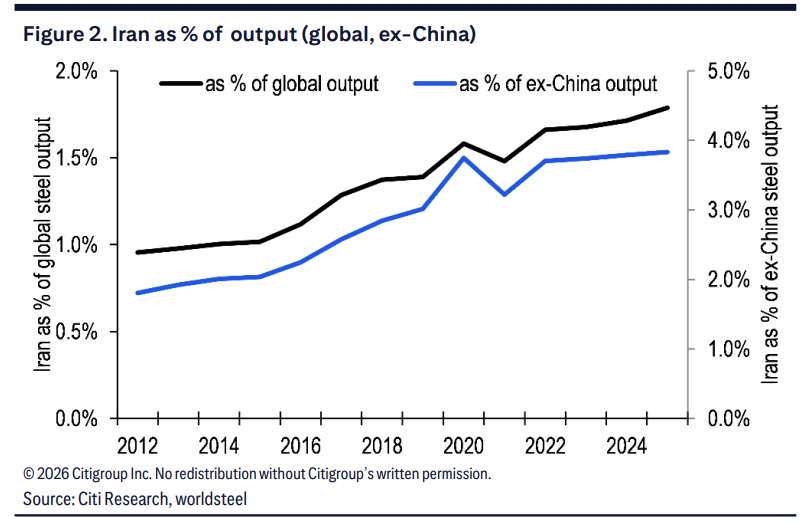

Iran's steel production is projected to reach approximately 32 million tons in 2025, accounting for about 1.8% of global steel production and 3.8% of global steel production excluding China. This is comparable to Germany's (34 million tons), about 40% of the US's (82 million tons) production, and nearly a quarter of Europe's total production (134 million tons)—making it far from a marginal player. If 70% of its capacity is indeed destroyed, over 20 million tons of annual capacity will evaporate from the market.

Citigroup warns that this is a structural supply gap that has been severely underestimated by the market, and the global steel supply and demand balance will face substantial restructuring.

The core pillar of the Middle East's steel landscape

The rise of Iran's steel industry is of great strategic significance.

According to data from the World Steel Association, Iran's annual steel production will double from 14.4 million tons in 2013 to 32 million tons in 2025, with a compound annual growth rate of 6.3%, thus making it the world's tenth largest steel producer.Iran exports 30% of its steel production and meets 70% of its domestic demand, creating a supply pattern that balances domestic and international markets.

The core impact of this strike is:If domestic production capacity is significantly reduced, the portion of output originally intended for export will prioritize meeting domestic demand. This means that the 9 million tons of net exports will almost certainly and quickly disappear from global trade flows, with no alternative in the short term.

The supply gap is extremely difficult to fill.

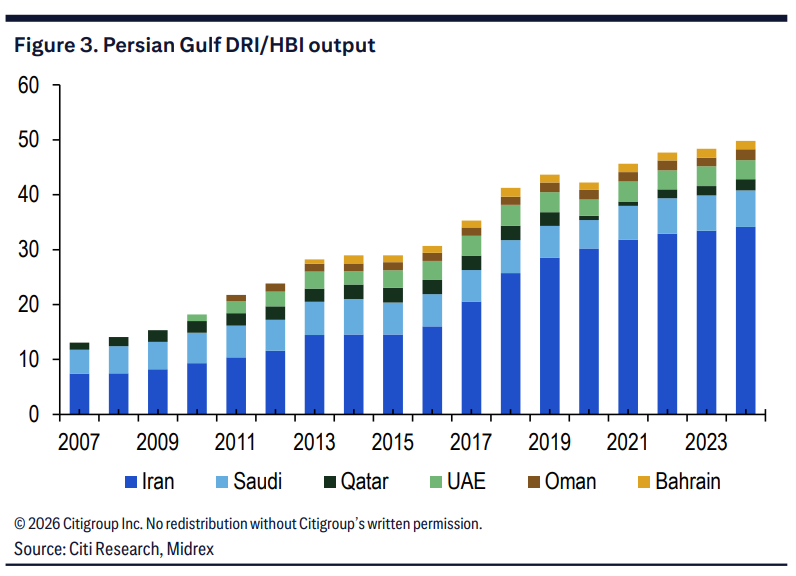

Citigroup stated that Iranian steel production is highly dependent on direct reduced iron (DRI) gas-based processes, which is significantly different from the globally mainstream blast furnace ironmaking method.This also significantly increases the difficulty of finding a replacement.

In 2024, Iran's DRI production reached 34.2 million tons, a year-on-year increase of 2%, making it the world's second-largest DRI producer and accounting for approximately 69% of the total DRI/HBI production in the Persian Gulf region. While DRI accounts for only about 7.5% of crude steel raw materials globally, in Iran…This figure exceeds 80%—Iran's steel production is almost entirely driven by natural gas-fired iron ore reduction, rather than coke smelting.

From a broader perspective, DRI production in the Persian Gulf region has expanded from 13.1 million tons in 2007 to 49.8 million tons in 2024, accounting for over 35% of global DRI/HBI production (compared to approximately 19% in 2007). Iran is the absolute core of this growth.

If this industrial chain, built on the country's abundant natural gas reserves, breaks down, other countries will have to undergo a fundamental shift in their raw material structure, from natural gas to coking coal, if they want to fill the gap with blast furnace capacity.

Coking Coal Market: The Overlooked Chain Reaction and the Logic for Going Long

Citibank estimates thatIf Iran's 34 million tons of gas-based DRI production were fully replaced by blast furnace capacity in other parts of the world, it would generate an additional demand for approximately 20 million tons of coking coal, equivalent to 8% to 10% of the global seaborne coking coal market.

Even if it only replaces the portion corresponding to exports (approximately 9 to 11 million tons of exported steel), it will still bring about an additional demand for coking coal of approximately 6 to 7 million tons.

Of course, Citi Research also pointed out hedging factors: Iran's domestic steel demand may shrink in the short term under the current situation, so it may not be necessary to fully replace all DRI capacity.

Even if only the substitution of exports is considered, the potential additional demand for coking coal of 6 to 7 million tons is enough to create a substantial price driver for the relatively limited global seaborne coking coal market.

Focus on three main themes

Citigroup recommends investors focus on three main trading themes:

First, upward pressure on global steel prices:

The rapid withdrawal of 9 million tons of net exports will create a clear supply gap in Iran's traditional export destinations (the Middle East, Southeast Asia, etc.), which will benefit spot and futures prices of steel in the relevant regions.

Second, the price revaluation of coking coal-related assets:

Whether it's full or partial substitution, the activation of global blast furnace capacity signifies a significant marginal increase in demand for seaborne coking coal. Related coking coal producers and traders face a positive catalyst.

Third, the structural challenges of filling the supply gap:

Iran’s gas-based DRI production capacity cannot be replicated in the short term, while mobilizing traditional blast furnace capacity requires time and capital.This means that the supply-demand imbalance may last for several quarters or even longer, rather than a fleeting, impulsive shock.

~~~~~~~~~~~~~~~~~~~~~~~~

The above exciting content comes from

For more detailed analysis, including real-time updates and firsthand research, please join [the group/group].

![When copper prices rise, who is buying, who is pushing up prices, and who is buying on dips? [Peifengke Master Class 3.1]](http://img.528btc.com.cn/pro/2026-04-07/img/1775556730039cc9499b27xjjh6h6ba865524b31x86h8.jpg)