Author:Wall Street CN

[Report]Guide】The current market structure is not in a steady state, and the next scenario warrants attention. When the biggest source of shock is energy, then resolving energy-related issues is the key to truly resilient assets, and an increase in energy's share of global GDP is highly probable.

Summary

summary

1 Current market characteristics: When the flood comes

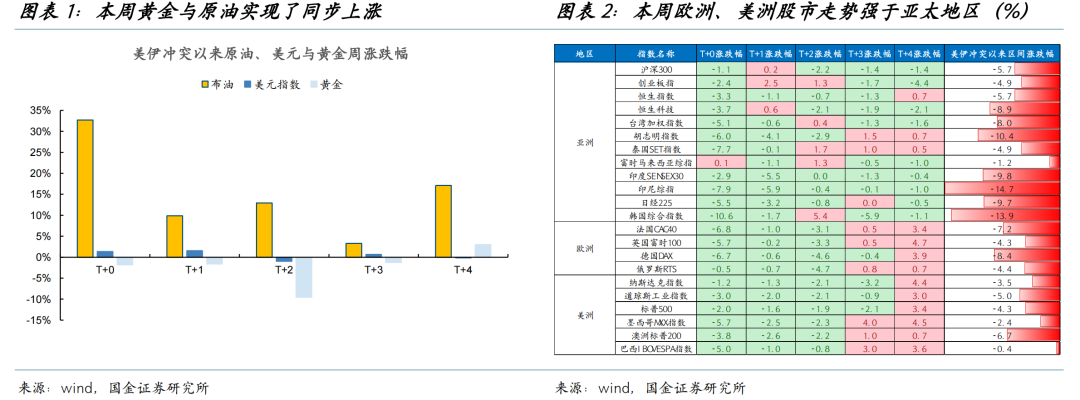

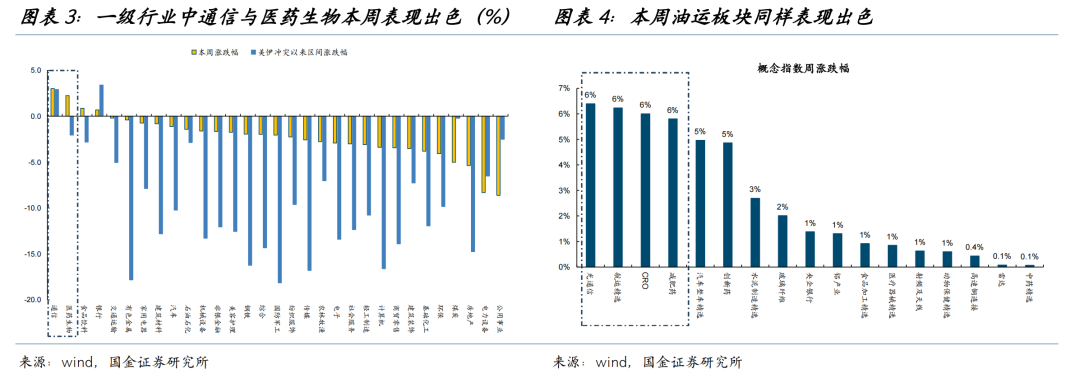

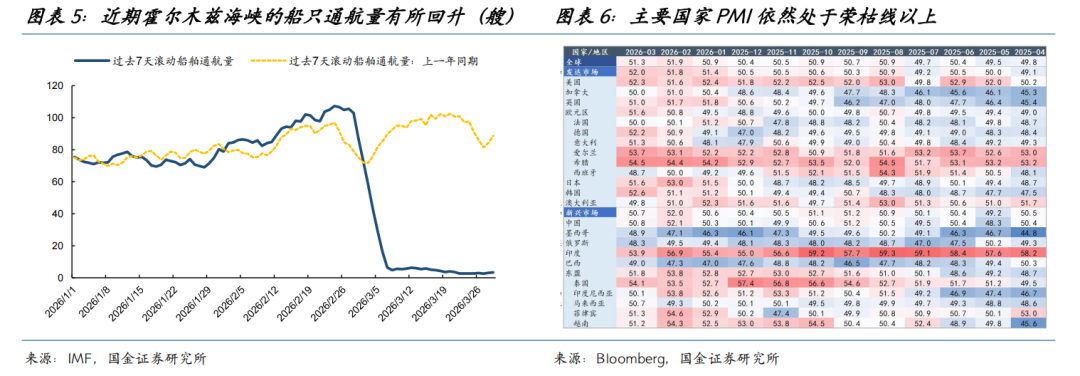

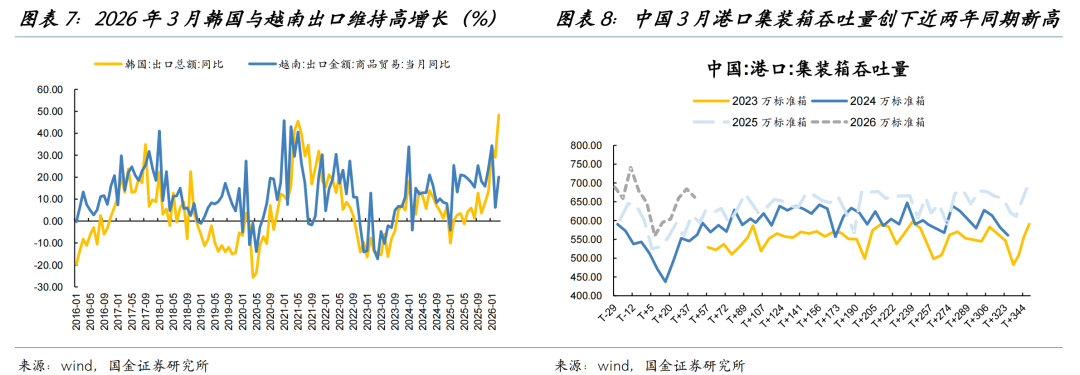

As of this week (March 30, 2026 to April 3, 2026, the same below), the US-Iran conflict has lasted for a month, yet it remains the core contradiction dominating the current trend of major asset classes. From the perspective of the evolution of the war: on the one hand, investors' attitudes toward the United States have changed, gradually shifting from being a safe haven and beneficiary of the war to whether the US can extricate itself smoothly; on the other hand, as negotiations have stalled, Trump's tough statements will intensify the short-term impact. However, even if the Strait remains closed, the US will end the war within two or three weeks, giving the market the expectation that the short-term problem will be resolved. But the prolonged closure of the Strait has begun to slowly impact some of the fundamental resilience. Under the above logic, the market as a whole exhibited several types of transactions: the US dollar fluctuated, while gold gradually stabilized despite rising oil prices; the US stock market was no longer the only safe haven for funds; stock markets in Europe and the Americas, which were less affected by the closure of the strait, began to strengthen; and the Asia-Pacific region, which was more significantly affected by the continued closure of the strait, was generally weak. Within the A-share market, investors chose to buy into sectors with independent growth prospects, such as AI computing power and innovative drugs. Of course, some relatively optimistic investors also anticipated that the strait would resume navigation after the US withdrawal (which could solve the problem of oil tankers having high prices but no market), and thus chose to buy oil shipping stocks.If we were to use an analogy for the above transactions, it would be like a flood coming, with some people choosing relatively high places and others believing that the flood will recede.

2 The resilience and fragility of fundamentals

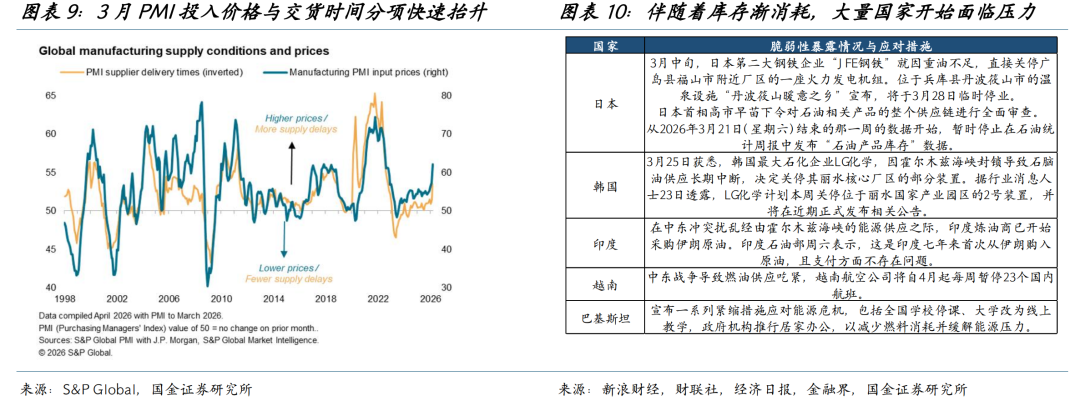

The reality is that the Strait of Hormuz remains effectively blocked, with only limited passage. Although March data suggests continued resilience in global manufacturing activity, underlying vulnerabilities are emerging: the March PMI input price and delivery time sub-indices hit their highest levels since 2023, indicating a sharp increase in global inflationary pressures; simultaneously, as existing inventories and the rush to fulfill orders gradually diminish, more and more countries are facing pressure. For example, due to a lack of mature crude oil processing capacity, Japan's fuel inventories are declining rapidly, and the industrial and service sectors are experiencing "localized oil shortages/supply reductions"; and South Korea is closing its chemical plants due to naphtha supply disruptions.As more and more countries approach the limits of their fundamental stress tests, the impact of whether the problems can be resolved smoothly in three weeks is growing daily.

3 Future Scenario: Regardless of whether the war ends, the illusion of the US dollar may recede.

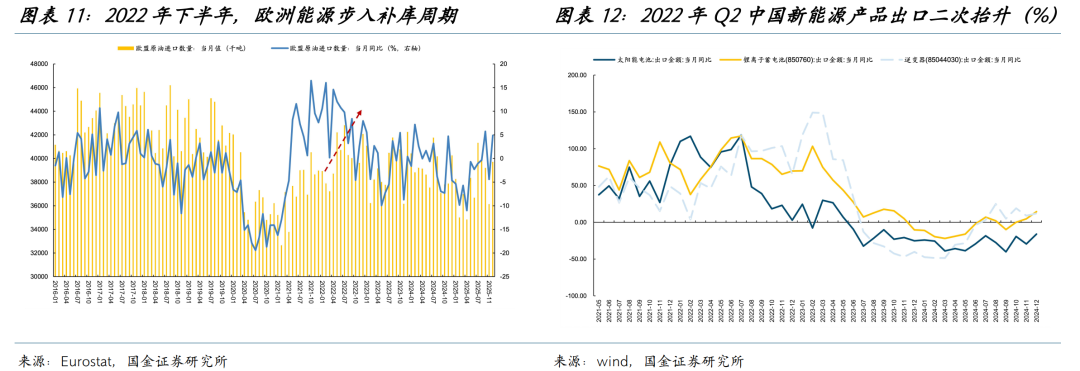

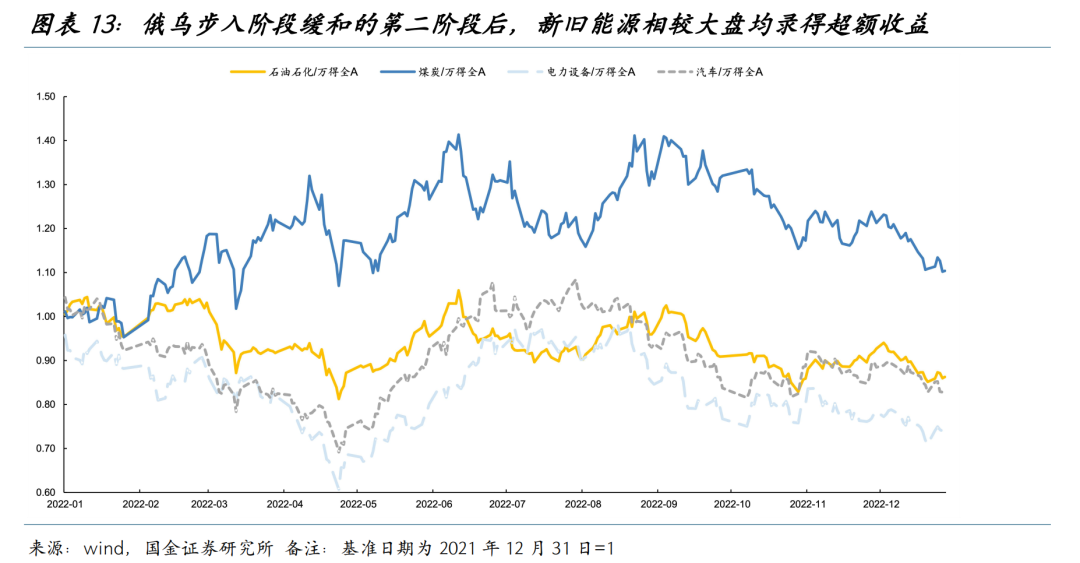

Currently, it seems highly unlikely that the Trump administration will achieve a "major victory" exit. The more probable scenarios are either: 1) As political costs rise, the administration declares "victory" upon reaching the promised deadline or achieving partial results, then hastily withdraws from the conflict; 2) Once the conflict devolves into a "ground war," it becomes protracted, forcing the US into a quagmire from which it cannot extricate itself. It's worth noting that in both scenarios, the support behind the dollar's strength weakens.Regarding the former,Whether the Strait of Hormuz can be "opened" in a new form is crucial. However, after the overall risks have eased, the problem of "high prices but no market" for energy in Asian countries may be addressed. Driven by the continued global recovery and restocking demand, the upward shift in the central energy price has been confirmed. Furthermore, driven by the demand for "energy security," a new round of new energy construction and traditional energy restocking is expected to begin, and the future market is likely to see a resonance between "new and old energy." Taking 2022 as an example, as Russia and Ukraine entered the second phase of the conflict (with both sides fighting and negotiating, and the supply chain disruptions caused by the sudden conflict being temporarily alleviated), Europe entered a phase of energy restocking and accelerated its energy transition, leading to a second surge in the export prosperity of China's new energy industry chain.New and old energy became the core theme of the market at that time.Meanwhile, driven by demand recovery and the trend of dollar weakening,Non-ferrous metals are also expected to see a recovery, with their industrial attributes increasing their elasticity in an overall rebound. As for the latter...The chances of the Strait of Hormuz opening are slim, and even the "safe haven assets" currently considered safe by the market are unlikely to remain unaffected. On one hand, rapidly rising energy prices exacerbate the risk of global stagflation, and the US's loss of control over the conflict and its own entanglement in it renders dollar assets no longer a safe haven. On the other hand, as a global manufacturing hub and a center for information and communication technology products, any damage to Asia's manufacturing capabilities will ultimately cause a complete disruption to the global supply chain. Even the construction of AI data centers will face supply disruptions, ultimately dragging down resilient technology assets worldwide.Funds will flow into more fundamental assets, with traditional energy chains potentially becoming a core safe haven.As the United States became mired in the "quagmire of war,"The dollar's strength will eventually subside, and the rebound in precious metals will continue.

4 The current market structure is not in a steady state.

The current market structure is not in a steady state. If the conflict escalates, the so-called resilient assets will also face a correction; if the situation eases, it may not be the optimal solution.In fact, when the biggest source of shock is energy, then resolving the energy contradiction is the real resilient asset, and it is highly likely that the share of energy in global GDP will increase.Based on current information, considering the combined expected values of both scenarios, and with an increased optimistic outlook for the market, we make the following recommendations: I. As the world enters a period of energy replenishment, both old and new energy sources are expected to resonate with each other.Oil, oil transportation, coal, lithium batteries, wind and solar power, energy storageSecond, as the illusion of the US dollar gradually fades, the financial attributes of commodities are shifting back, coupled with a recovery in demand.Copper, aluminum, goldIII. Reassessment of China's Manufacturing Industry:Machinery and equipment, chemicalsAs "Made in China" becomes a global cornerstone, continued better-than-expected exports and capital repatriation will also provide new impetus for long-dormant domestic demand, seeking structural opportunities amidst the reversal of suppressing factors.Tourism and scenic spots, condiments and fermented products, beer and other alcoholic beverages, pharmaceutical commerce, and medical aesthetics.wait.

Risk Warning:Geopolitical conflicts intensify; overseas economies experience a sharp downturn.

Report text

1. Logical consistency and real-world contradictions at the market transaction level

However, potential vulnerabilities are being exposed: the March PMI input price and delivery time sub-indices hit a new high since 2023, indicating a sharp increase in global inflationary pressures; at the same time, as existing inventories and the rush to complete orders gradually diminish, more and more countries are beginning to face pressure. For example, due to a lack of mature crude oil processing capacity, Japan's fuel inventories are declining rapidly, and the industrial and service sectors have experienced "localized oil shortages/supply reductions"; South Korea is also closing its chemical plants due to naphtha supply disruptions; and India is turning to increasing imports of Russian crude oil and natural gas.

2. Future Scenario: Regardless of whether the war ends, the illusion of the US dollar may recede.

Scenario 2: The war continues, and the United States is bogged down: funds flow into the most basic assets, and traditional energy may be the only safe haven.

In this scenario, the chances of Iran opening the Strait of Hormuz, its core countermeasure, are slim. It's even possible that Iran will further disrupt navigation in the Bab el-Mandeb Strait as a means of countermeasures, exacerbating global supply chain disruptions. Reflecting on this in the capital markets, even assets currently considered "safe" are unlikely to remain unaffected.

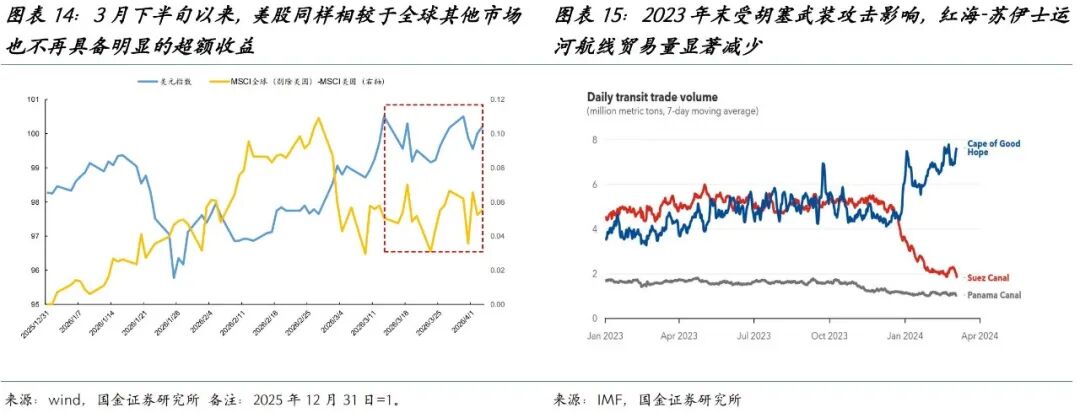

On the one hand, the rapid rise in energy prices has exacerbated the risk of global stagflation. On the other hand, the loss of control of the war situation by the United States has made dollar assets no longer a safe haven. In fact, since the second half of March, after the dollar has been fluctuating, US stocks have also lost their significant excess returns compared to other global markets. And referring to the experience of 2023, if the navigation of the Bab el-Mandeb Strait is disrupted again, Europe will also face certain supply pressures.

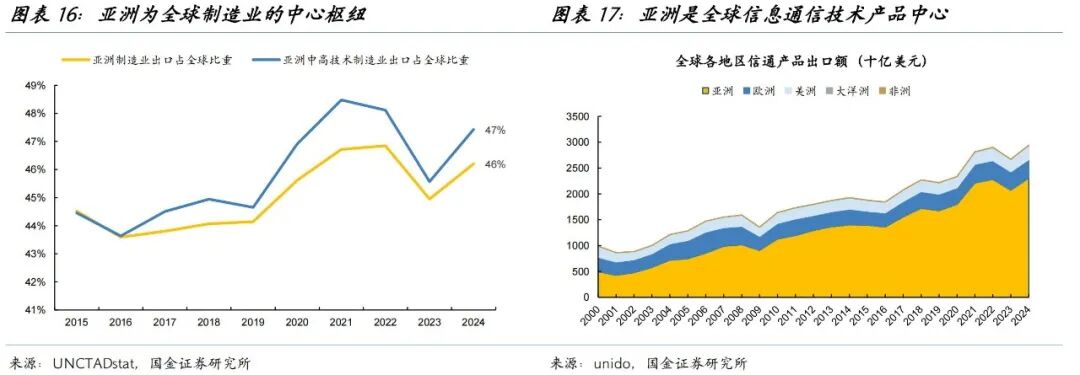

On the other hand, as the central hub of global manufacturing, Asia accounts for 47% of global manufacturing exports. Systemic damage to its manufacturing capacity will eventually affect global supply. It is worth mentioning that high-tech manufactured products also account for 46%. Especially for the AI industry, Asia is the global center for information and communication technology products, accounting for nearly 80% of global exports in 2024. This also means that once Asian production activities are damaged, the construction of AI data centers will also face the dilemma of supply disruption, which will ultimately drag down global technology resilient assets.

3. The current market structure is not in a steady state.

The current market structure is not in a steady state. If the conflict escalates, even so-called resilient assets will face a correction; if the situation eases, it may not be the optimal solution. In fact, since the biggest source of shock is energy, resolving energy-related issues is the true key to resilient assets, and an increase in energy's share of global GDP is highly probable.

Based on the current information, considering the combined expected value of both scenarios, and with an added optimistic outlook for the market, we make the following recommendations:

This article is sourced from: