Author:Wall Street CN

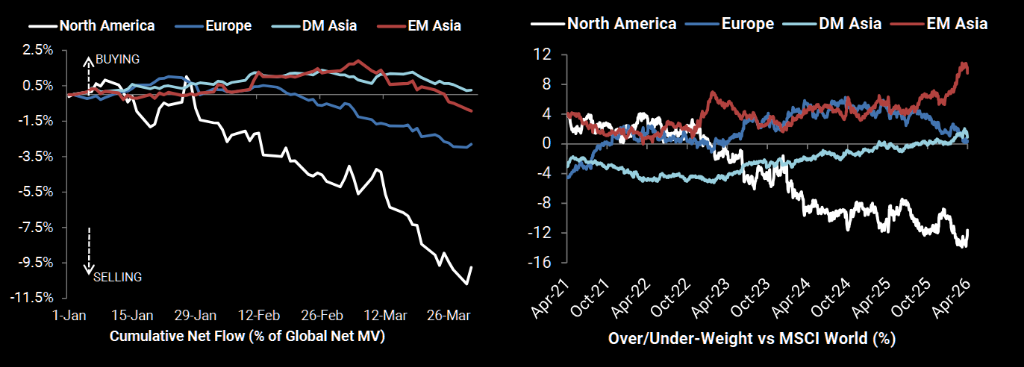

Multiple data sources indicate that European assets are experiencing one of the most severe sell-off waves in nearly a decade, with institutional investors reducing their European exposure at an extreme pace.

According to data from Goldman Sachs Prime Brokerage, net selling of European assets last month saw its largest monthly decline since March 2025, ranking as the third highest in the past decade, with short positions outnumbering long positions by a ratio of 2.2 to 1.

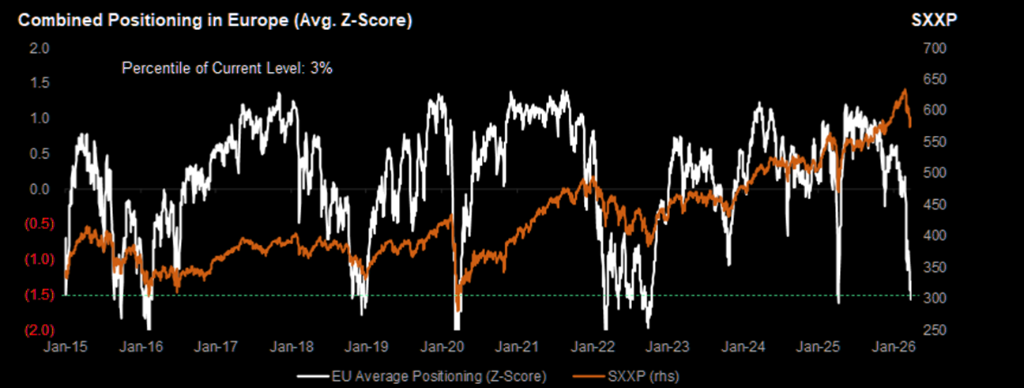

Meanwhile, data from JPMorgan Chase shows that the European composite positioning index has fallen to its third lowest level since 2015, with the standard deviation falling below -1.5 and the four-week position change falling below -2 standard deviations.

This figure means that the current net short pressure in European positions is an extreme case in the historical distribution over the past decade, with similar readings only seen after a few historical periods of market stress.

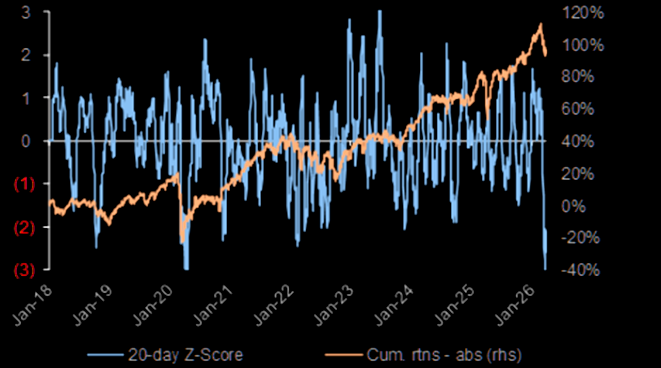

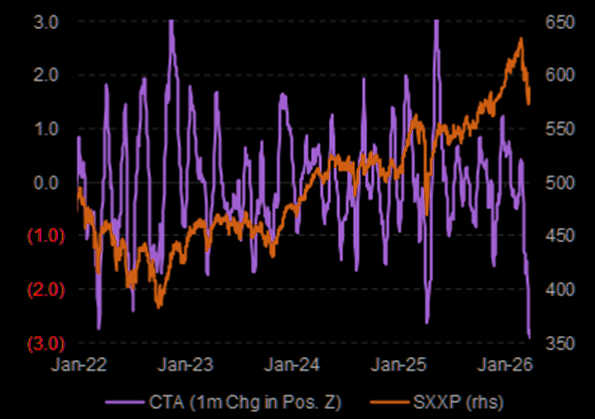

JPMorgan data further shows that, measured by the Z-score of changes in holdings over one month, the reduction in holdings of European assets by CTA groups has reached the most extreme level in the history of this data series.

As a representative of trend-following strategies, CTA's concentrated sell-offs often have a self-reinforcing effect, creating additional downward pressure on the market from a technical perspective.

JPMorgan's portfolio team points out that, considering hedge funds, CTAs (commodity trading advisors), and pure long-only funds, overall European portfolio holdings are at an "extremely low level."

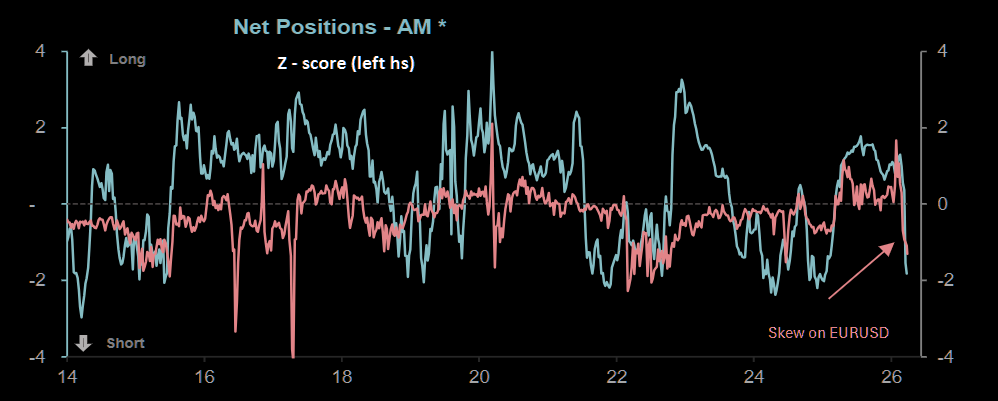

The signs of capital outflow are not only reflected in stock holdings, but also in the foreign exchange market, which confirms a systemic risk aversion trend.

The skew in the euro options market continues to decline, indicating that options market participants have generally shifted to betting on a decline in the euro.