Author:Wall Street CN

March's US non-farm payroll data reversed the weakness of February, showing an improvement in both employment and the unemployment rate. The monthly non-farm payrolls figure reached its highest level since December 2024, exceeding the Wall Street Journal's ten-year historical forecast range for the indicator. Could it be that in just one month, the US economy has gone from recession to a period of rapid growth and a second takeoff? Will the narrative of the recession trade come to an end?

1. Unveiling the Reasons for the Explosive Non-Farm Payrolls Report in March

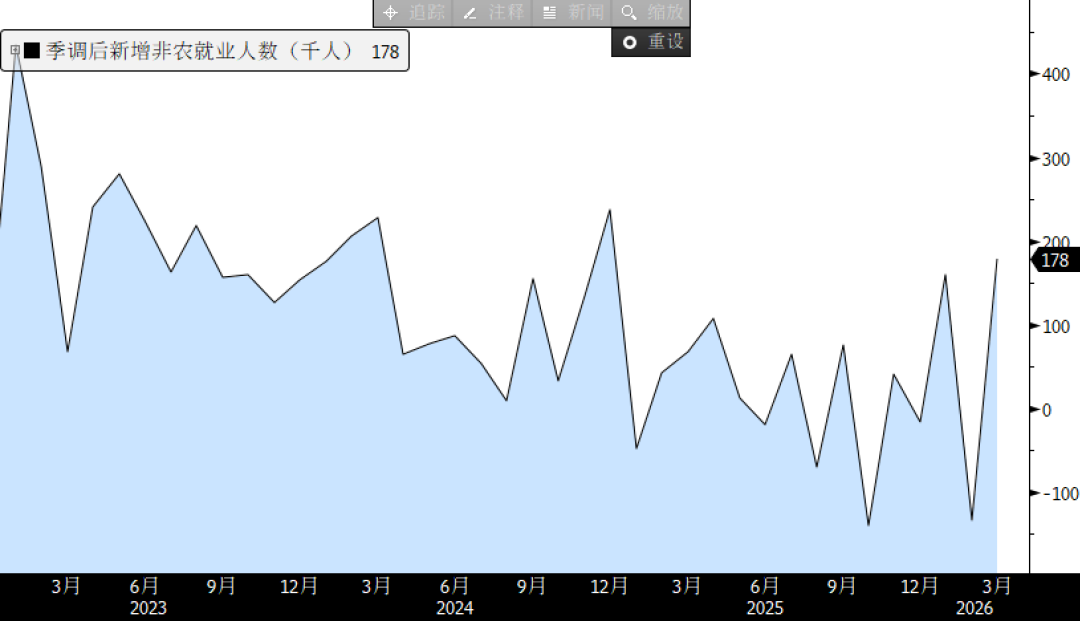

U.S. nonfarm payrolls rose 178,000 in March, far exceeding the expected 60,000; private sector nonfarm payrolls rose 186,000, also far exceeding the expected 70,000; the unemployment rate was 4.3%, a slight decrease from the previous value and the expected value of 4.40%.

What factors have created such a strong combination of employment data?

-

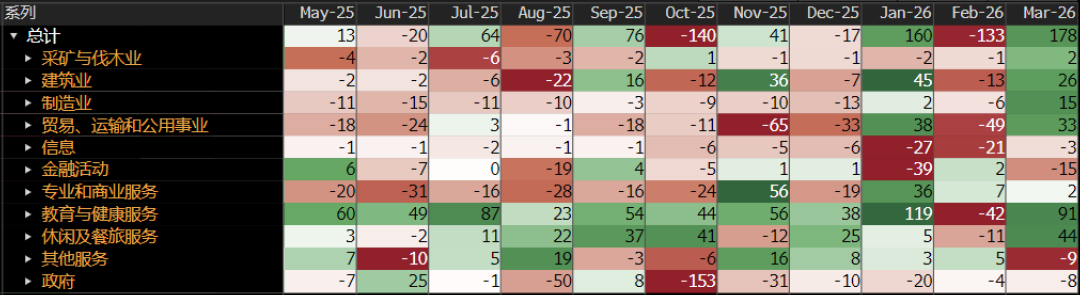

weather:The job losses due to climate change in February were a major reason for the downward revision of the previous figure, with the 41,000 jobs downgraded primarily from the "trade, transportation, and utilities" sector. These jobs were recovered in March, mainly reflected in a rebound in employment in the construction, transportation, and leisure and hospitality industries. Statistics show that the number of people unable to work normally due to climate change in March was 91,000, lower than the 140,000 figure for the same period over the past 10 years.

-

Strike and return to work:Healthcare employment data, which was hampered by the strike in February, rebounded significantly in March as strikers returned to their jobs.

-

Model Adjustment:This factor also played a role in the February data analysis. As the Labor Department began incorporating current sample information and reducing smoothing into its birth and death models, the volatility of non-farm payroll data increased starting in February. This means we may see non-farm payroll data frequently exhibiting a bungee jump-like trajectory in the future.

2. The US economy still faces significant risks.

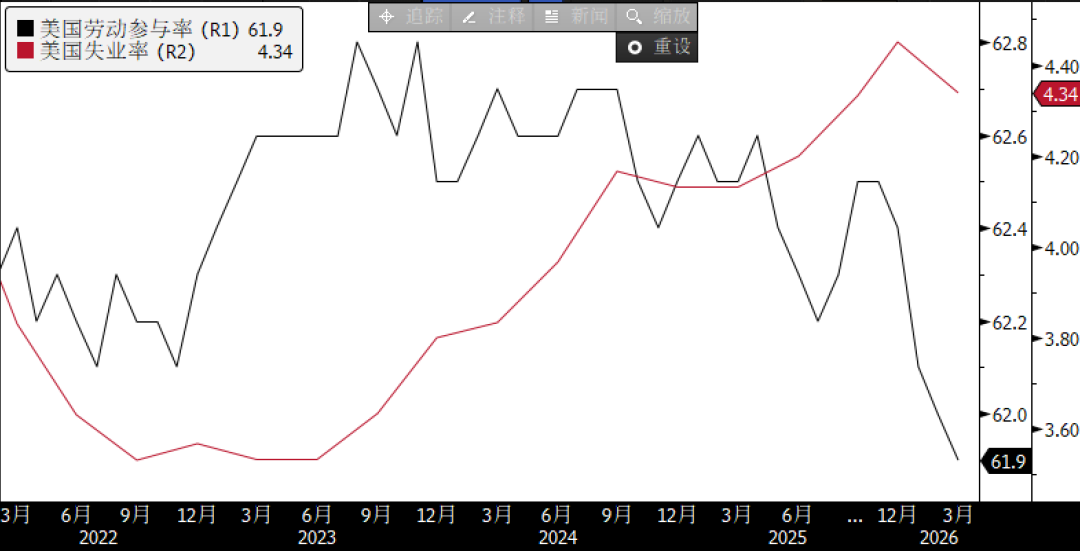

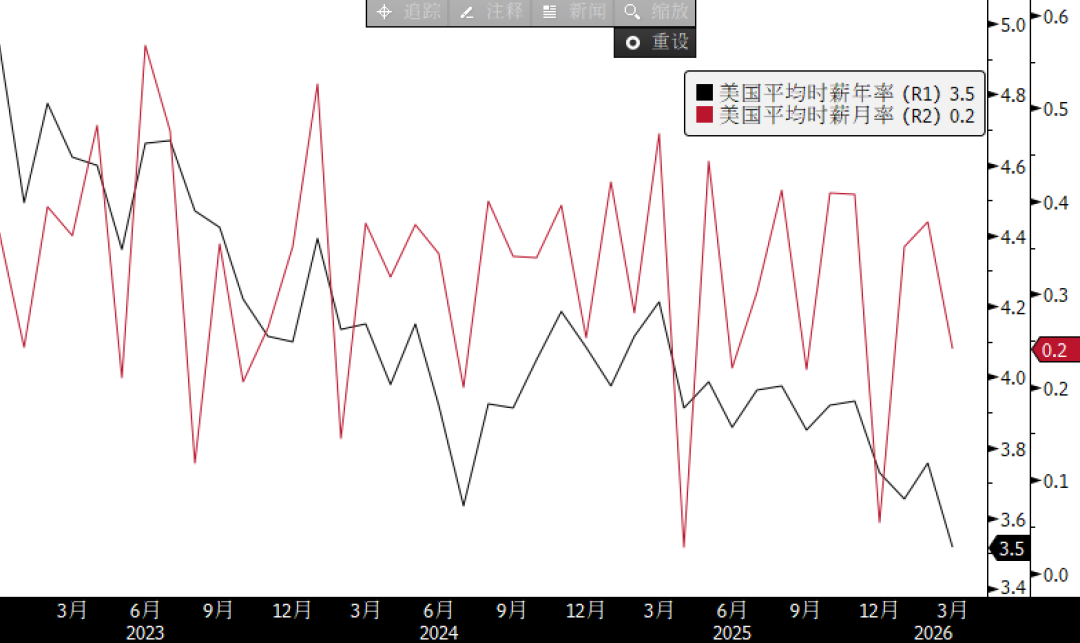

First, while the March employment data appears positive on the surface, the decline in the labor force participation rate and the continued slowdown in the growth rate of average hourly wages are significant risks that cannot be ignored. The annualized rate of average hourly wages has fallen to its lowest level since 2022, indicating that companies do not have a strong demand for labor. It is also worth noting that this data was collected shortly after the outbreak of the US-Iran conflict, meaning that companies may not have yet incorporated the conflict into their recruitment decisions.

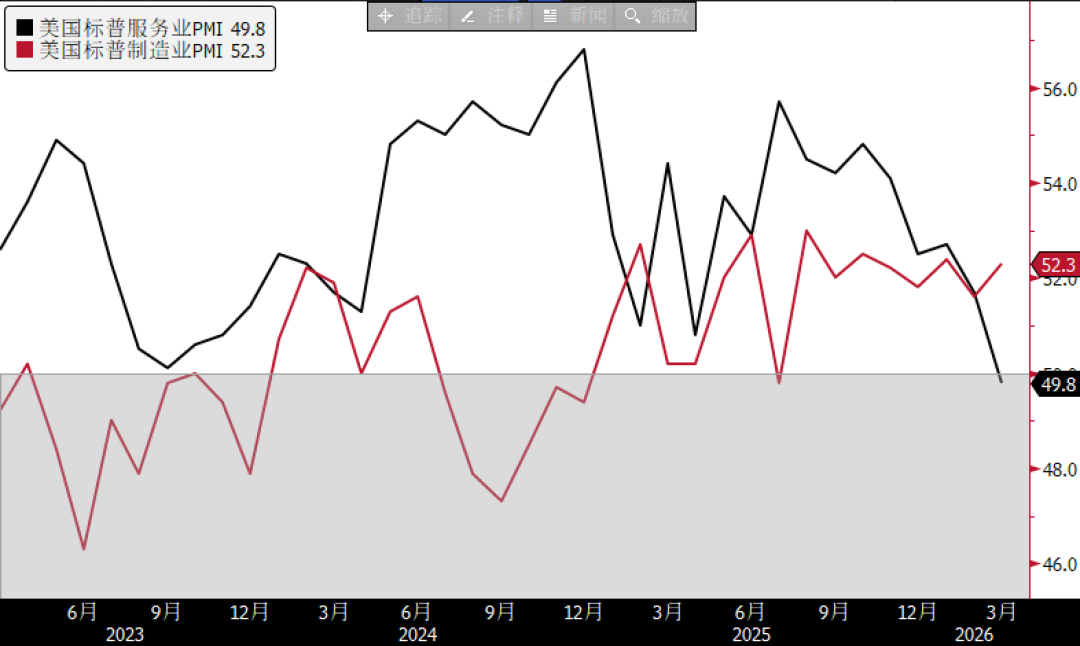

In addition, the US S&P services PMI in March hit a three-year low of 49.8, falling below the 50-point mark that separates expansion from contraction, in stark contrast to the increasingly recovering manufacturing sector, indicating a continued decline in the momentum of the US service sector.

3. Conclusion: Has the narrative of decline come to an end?

While the US economy doesn't currently appear to have a high probability of a hard landing, the underlying risks are equally thorny. As we mentioned in "How Far Away Are We from a Recession Trade?", we are still some distance from shifting to a recession narrative, and this non-farm payroll data has pushed that distance even further.

More worrying in the short term than a recession is how the confrontation between Trump, who is resorting to profanity, and Iran, which refuses to back down, will end, and how the return of international oil prices to 110 will affect global inflation. This Friday's US March CPI data is undoubtedly a crucial signal. After February's PPI significantly exceeded expectations, the March CPI annual rate is expected to be 3.4% (previous value 2.4%), and the monthly rate is expected to be as high as 1.0% (previous value 0.3%), seemingly adding fuel to the fire of a "protracted war on high interest rates." With expectations of a Fed rate cut this year at zero and the US dollar index hovering around the 100 mark, the CPI may become a key moment determining the direction of global financial markets.

This article is sourced from: