Author:Wall Street CN

Key points

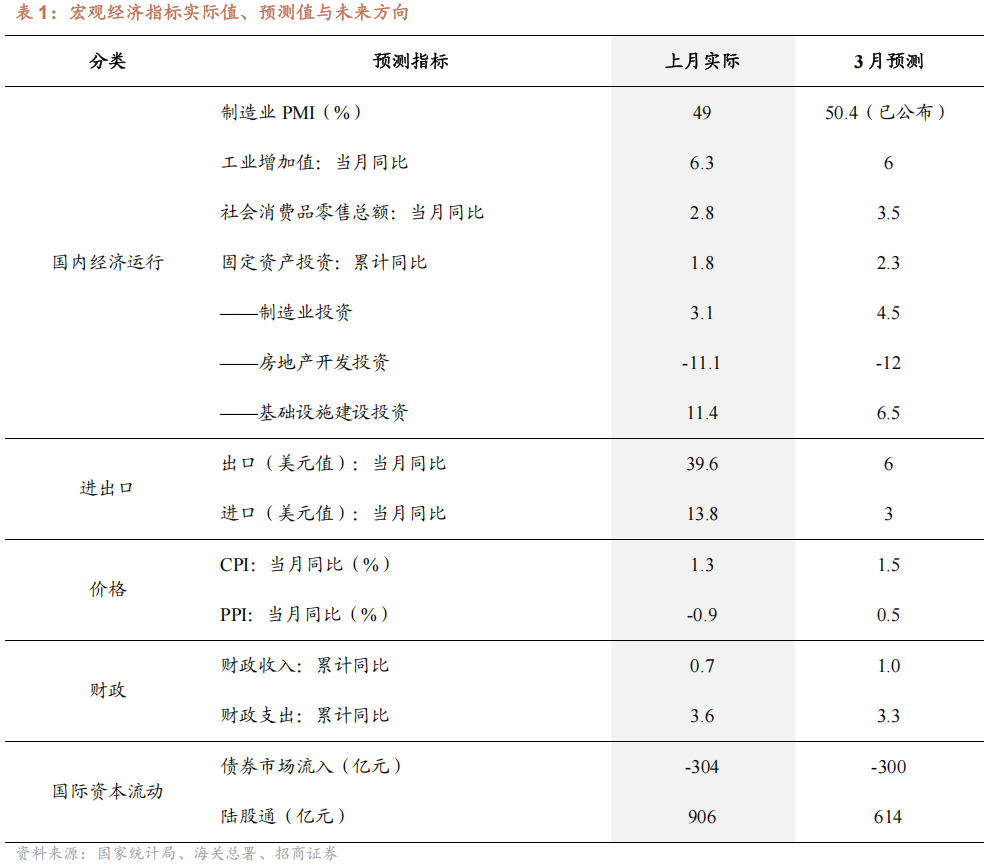

Production: Industrial production continued its relatively strong performance. Data released shows that the industrial recovery in January and February was primarily supported by equipment manufacturing, high-tech industries, and the export chain. Entering March, the manufacturing PMI rebounded to 50.4%, the production index rose to 51.4%, and the new orders index rose to 51.6%, indicating that after the Spring Festival disruption subsided, corporate production activities accelerated significantly, and improved orders also provided some support for production. The year-on-year growth rate of industrial added value above designated size in March is expected to be 6%. Structurally, automobiles, electronics, electrical equipment, aerospace, and some high-end manufacturing sectors will remain the core highlights of industrial production in March; while traditional real estate-related industries such as ferrous metals and building materials may see a weak marginal recovery, they are still struggling to escape the low-level operating pattern, showing more of a narrowing decline than a trend of recovery. The first-quarter growth rate is likely to be higher than the lower limit of the policy target of 4.5%, but before a stronger recovery in consumption and real estate, the probability of significantly exceeding the upper limit of the target is not high, and it may be recorded at around 5.0%.

Consumption: Retail sales are expected to improve moderately in March, but the recovery in household consumption remains slow. The year-on-year growth rate of total retail sales of consumer goods in March is projected to be around 3.5%. While the year-on-year growth rate of retail sales in January and February improved compared to the end of last year, it remains in a relatively low range, indicating that there is still considerable room for recovery in household consumption. Although the non-manufacturing sector saw a rebound in March, the service sector business activity index was only 50.2%, and the business activity indices for retail, accommodation, catering, and real estate sectors remained below the critical point, meaning that the consumption recovery still exhibits structural characteristics and has not yet achieved widespread expansion. On the policy front, trade-in programs and durable goods replacement policies will continue to provide some support for discretionary consumption such as home appliances, digital products, and automobiles. However, the slow recovery of household income expectations and balance sheets determines that a significant acceleration in consumption is unlikely. Overall, consumption in March will see marginal improvement compared to January and February, but the rate of improvement will remain limited, and weak domestic demand remains a significant constraint on current macroeconomic performance.

Fixed asset investment: Infrastructure continues to provide support, manufacturing maintains resilience, and real estate remains the main drag. The cumulative year-on-year growth rate of fixed asset investment for January-March is estimated at approximately 2.5%. Although the business activity index for the construction industry rebounded to 49.3% in March, it remains below the expansion/contraction threshold, indicating that the improvement in the construction and real estate chain is still limited. Looking ahead, infrastructure will remain a crucial tool for stabilizing growth, while manufacturing investment will continue to benefit from support in areas such as equipment upgrades, expansion of high-tech manufacturing, and digital transformation. However, real estate sales, land acquisition, construction starts, and the capital chain have not yet shown substantial recovery; therefore, the drag on investment from real estate is unlikely to ease significantly in the short term.

Exports: March exports remained resilient, but the growth rate is expected to decline compared to the previous two months. Year-on-year export growth is projected to remain positive in March, with a growth rate of approximately 6% in USD terms. The main drivers of current exports remain machinery and electronics, high-tech products, and manufacturing sectors with strong competitiveness. However, the high export growth in the first two months included factors such as the timing of the Spring Festival, a low base, and some orders being front-loaded. March's year-on-year growth is likely to return to a more normal range. In the March manufacturing PMI, the new export orders index rebounded to 49.1%, a significant improvement from February, but still not back into expansion territory, indicating that external demand is not universally strong, but rather exhibits characteristics of "resilience in total volume, but continued marginal pressure." Structurally, exports of machinery and electronics, high-tech products, and some intermediate goods are expected to remain the main drivers, while the recovery of traditional labor-intensive categories is relatively limited.

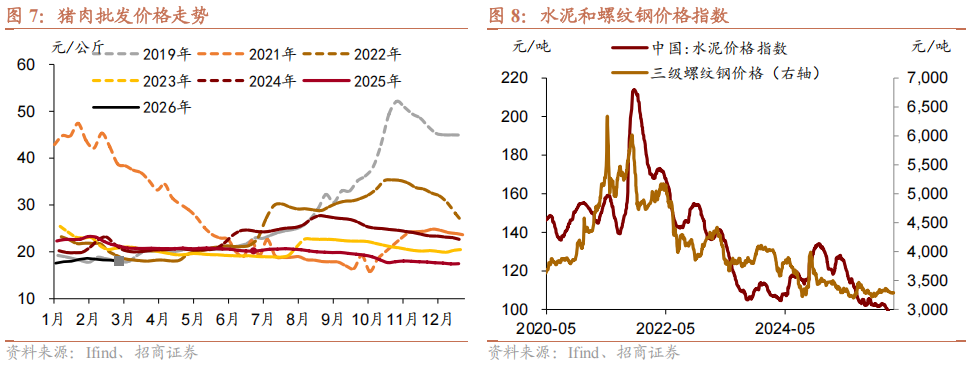

Inflation: CPI and PPI are expected to rebound to around 1.5% and 0.5% year-on-year, respectively. The CPI is expected to rebound to around 1.5% year-on-year, mainly because while food prices seasonally declined after the Spring Festival, particularly pork prices, the resilience of service consumption provided support for core CPI. Meanwhile, the US-Iran conflict in the Middle East pushed up international oil prices, leading to an increase in domestic refined oil prices, turning the energy component from a drag on CPI into a boost. The PPI is expected to rise to around 0.5% year-on-year, primarily due to the surge in international crude oil prices driving up prices in the petrochemical chain. This, coupled with the resumption of work and production after the Spring Festival, resilient external demand, proactive fiscal policies, and the commencement of some major projects, has driven a general rebound in prices of industrial products such as energy, chemicals, steel, and cement, resulting in a significantly faster recovery in industrial inflation.

Specific related indicators are projected as follows: Industrial value added in March is expected to grow by approximately 6% year-on-year; retail sales are expected to grow by approximately 3.5% year-on-year; fixed asset investment from January to March is expected to grow by approximately 2.5% year-on-year; exports and imports are expected to grow by approximately 6% and 3% respectively; CPI and PPI are expected to grow by approximately 1.5% and 0.5% year-on-year respectively. General public budget revenue is expected to grow by approximately 1.0% year-on-year, and general public budget expenditure is expected to grow by approximately 3.3% year-on-year.

text

I. Economic Operation

1. Domestic Economy

Production: The year-on-year growth rate of industrial added value above designated size in March is expected to be 6%, and industrial production continues to operate with a relatively strong trend.

Based on the released data, the industrial recovery in January and February was mainly supported by equipment manufacturing, high technology, and the export chain. Entering March, the manufacturing PMI rebounded to 50.4%, the production index rose to 51.4%, and the new orders index rose to 51.6%, indicating that after the Spring Festival disruption subsided, corporate production activities accelerated significantly, and improved orders also provided some support for production. Structurally, automobiles, electronics, electrical equipment, aerospace, and some high-end manufacturing sectors will remain the core highlights of industrial production in March; while traditional real estate-related industries such as ferrous metals and building materials may see a weak marginal recovery, they are still struggling to escape their low-level operating pattern, showing more of a narrowing decline than a trend of recovery. The first-quarter growth rate is likely to be higher than the lower limit of the policy target of 4.5%, but without a stronger recovery in consumption and real estate, the probability of significantly exceeding the upper limit of the target is not high, and it may be recorded at around 5.0%.

Consumption: Retail sales are expected to improve moderately in March, but the recovery in household consumption remains slow.

March's total retail sales of consumer goods are expected to grow by around 3.5% year-on-year. While the year-on-year growth rate of retail sales in January and February improved compared to the end of last year, it remains in a relatively low growth range, indicating that there is still considerable room for recovery in consumer spending. Although the non-manufacturing sector saw a rebound in March, the service sector business activity index was only 50.2%, and the business activity indices for retail, accommodation, catering, and real estate sectors remained below the critical point, suggesting that the consumption recovery still exhibits structural characteristics and has not yet achieved widespread expansion. On the policy front, trade-in programs and durable goods replacement policies will continue to provide some support for discretionary consumption such as home appliances, digital products, and automobiles. However, the slow recovery of residents' income expectations and balance sheets determines that a significant acceleration in consumption is unlikely. Overall, March consumption is expected to show marginal improvement compared to January and February, but the rate of improvement will remain limited, and weak domestic demand remains a significant constraint on current macroeconomic performance.

Fixed asset investment: Infrastructure investment continues to provide support, manufacturing maintains resilience, and real estate remains the main drag.

Fixed asset investment is projected to grow by approximately 2.5% year-on-year in the first quarter. While the business activity index for the construction industry rebounded to 49.3% in March, it remained below the expansion/contraction threshold, indicating limited improvement in the construction and real estate supply chain. Looking ahead, infrastructure investment will remain a crucial driver of stable growth, while manufacturing investment will continue to benefit from support in areas such as equipment upgrades, expansion of high-tech manufacturing, and digital transformation. However, real estate sales, land acquisition, construction starts, and the capital chain have not yet seen substantial recovery; therefore, the drag on investment from the real estate sector is unlikely to ease significantly in the short term.

Exports: Exports remained resilient in March, but the growth rate is expected to decline compared to the previous two months.

Exports are expected to maintain positive year-on-year growth in March, with a growth rate of approximately 6% in US dollar terms. The main drivers of current exports remain machinery and electronics, high-tech products, and manufacturing sectors with strong competitiveness. However, the high export growth in the first two months included factors such as the timing of the Spring Festival, a low base, and some orders being placed ahead of schedule. Therefore, the year-on-year growth rate in March is likely to return to a more normal range. In the March manufacturing PMI, the new export orders index rebounded to 49.1%, a significant improvement from February, but still not back into expansion territory. This indicates that external demand is not strengthening across the board, but rather exhibits characteristics of "resilience in total volume, but continued marginal pressure." Structurally, exports of machinery and electronics, high-tech products, and some intermediate goods are expected to remain the main drivers, while the recovery of traditional labor-intensive categories is relatively limited.

Inflation: CPI and PPI are expected to rebound to around 1.5% and 0.5% year-on-year, respectively.

The CPI is expected to rebound to around 1.5% year-on-year, mainly because although food prices seasonally declined after the Spring Festival, especially with the decline in pork prices dragging down the overall CPI, service consumption remained resilient, and service prices supported the core CPI. Meanwhile, the conflict between the US and Iran in the Middle East pushed up international oil prices, leading to an increase in domestic refined oil prices, turning the energy component from a drag on the CPI into a boost. The PPI is expected to rise to around 0.5% year-on-year, primarily due to the surge in international crude oil prices driving up prices in the petrochemical chain. This, coupled with the resumption of work and production after the Spring Festival, resilient external demand, proactive fiscal policies, and the commencement of some major projects, has driven a general rebound in prices of industrial products such as energy, chemicals, steel, and cement, resulting in a significantly faster recovery in industrial inflation.

Specific related indicators are expected to be as follows: industrial added value in March is expected to grow by about 6% year-on-year, retail sales are expected to grow by about 3.5% year-on-year, fixed asset investment from January to March is expected to grow by about 2.5% year-on-year, exports and imports are expected to grow by about 6% and 3% respectively, and CPI and PPI are expected to grow by about 1.5% and 0.5% year-on-year respectively.

2. Import and export

Exports: Exports remained resilient in March, but the growth rate is expected to decline compared to the previous two months.

Exports are expected to maintain positive year-on-year growth in March, with a growth rate of approximately 6% in US dollar terms. The main drivers of current exports remain machinery and electronics, high-tech products, and manufacturing sectors with strong competitiveness. However, the high export growth in the first two months included factors such as the timing of the Spring Festival, a low base, and some orders being placed ahead of schedule. Therefore, the year-on-year growth rate in March is likely to return to a more normal range. In the March manufacturing PMI, the new export orders index rebounded to 49.1%, a significant improvement from February, but still not back into expansion territory. This indicates that external demand is not strengthening across the board, but rather exhibits characteristics of "resilience in total volume, but continued marginal pressure." Structurally, exports of machinery and electronics, high-tech products, and some intermediate goods are expected to remain the main drivers, while the recovery of traditional labor-intensive categories is relatively limited.

Imports: March imports are expected to see a marginal recovery, but domestic demand remains insufficient.

Imports in March are projected to grow by approximately 3% year-on-year. While imports in the first two months appeared to grow rapidly, this was also influenced by a low base and temporary restocking. Looking at leading indicators for March, the import index in the manufacturing PMI has rebounded to 49.8%, a significant improvement from February, reflecting a recovery in demand for raw materials and intermediate goods. Meanwhile, profits of large-scale industrial enterprises increased by 15.2% year-on-year in January and February, with manufacturing profits growing by 18.9%, providing some support for upstream raw material and intermediate input demand. However, current demand from the real estate sector and the household sector remains weak, indicating that the improvement in imports is more a recovery in production-oriented and technology-oriented imports than a strong rebound driven by a comprehensive recovery in domestic demand. Overall, imports in March are expected to recover somewhat, but the strength of this recovery should not be overestimated.

II. Commodity Prices

The CPI is expected to rise to around 1.5% year-on-year in March.

First, after the Spring Festival, consumer demand enters a period of low activity, and prices of major food items such as pork, fresh vegetables, fresh fruit, and eggs generally decline. This seasonal drop in food prices pulls down the CPI. In particular, pork prices have fallen below the cost line, making them the biggest drag on the CPI, while the decline in other food items is relatively controllable.

Second, service consumption remained resilient, providing strong support for core CPI. Despite the fading effect of the Spring Festival, the service sector PMI continued its expansionary trend in March. Coupled with the price rigidity of some service items, the year-on-year increase in service prices is expected to remain around 0.8%, continuing to be a key force in the CPI.

Third, influenced by the geopolitical conflict between the US and Iran in the Middle East, international crude oil prices continued to rise in March, and this has already been transmitted to the domestic market through the refined oil price adjustment mechanism. The latest data from the National Development and Reform Commission shows that the average price of refined oil (gasoline) in March, after two increases, reached 9,300 yuan/ton, a month-on-month increase of 17.2% and a year-on-year increase of 10.2%. This is expected to push up the CPI by 0.25 percentage points month-on-month and 0.15 percentage points year-on-year, respectively, which will reverse the previous drag on the CPI from oil prices. In summary, the carryover effect on the CPI rose from 0.2% in the previous month to 0.6% in March. The CPI is expected to be around -0.2% month-on-month in March, corresponding to a new price increase factor of around 0.9%, and the CPI is projected to rebound to 1.5% year-on-year in March.

The PPI is expected to turn positive year-on-year in March, with an increase of around 0.5%.

First, geopolitical conflicts in the Middle East have driven up international crude oil prices, which in turn have boosted prices in the domestic oil, gas, and chemical industry chains. Specifically, the central price of international Brent crude oil rose by 40% month-on-month, while the central prices of domestic Nanhua Energy and Chemical and industrial product indices rose by 23.84% and 13.30% month-on-month, respectively, with the PPI-driven effect gradually becoming apparent.

Second, in March after the holiday, industrial enterprises gradually resumed work and production. Coupled with the resilience of external demand, the front-loading of domestic fiscal expenditures, and the commencement of some major projects under the "15th Five-Year Plan", the prices of energy and chemical products, rebar, cement and other products priced in the domestic market rebounded. In addition, the price of lithium carbonate, which represents the emerging economy, also continued to be strong, with the year-on-year increase further expanding.

Third, the latest March manufacturing PMI raw material purchase price index jumped sharply from 54.8% to 63.9%, driving the ex-factory price index up from 50.6% to 55.4%. Based on the relationship between the PMI ex-factory price index and the PPI month-on-month, the PPI month-on-month increase in March is expected to be around 1.0%, corresponding to an increase of 1.5% in the adjusted PPI due to new price increases. The PPI year-on-year increase in March is expected to reach around 0.5%, which will completely end the 41-month consecutive negative growth of PPI year-on-year.

III. Fiscal Policy

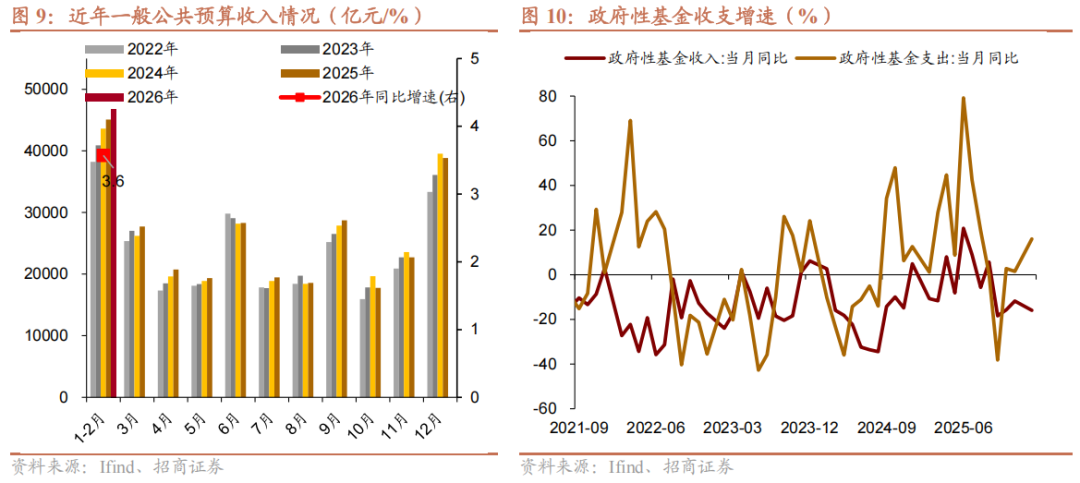

General public budget revenue is projected to grow by 1.0% year-on-year in March. The growth rate is expected to continue improving, reflecting a sustained recovery in economic fundamentals. Industrial value-added, consumption, and foreign trade all rebounded more strongly than expected in January and February, and March PMI data indicates that production and service sector activities remained robust. Furthermore, a significant recovery in industrial enterprise profits is expected to reverse the weak growth trend in corporate income tax.

General public budget expenditures in March are projected to grow by 3.3% year-on-year. Despite external risks, fiscal spending still needs to maintain a proactive expansionary trend to support the domestic economy. However, the pressure of maturing local government debt will gradually increase starting in March, which is expected to have a certain squeezing effect on the growth rate of short-term local government fiscal expenditures. Central government spending may accelerate to maintain the strength of general public budget expenditures.

Regarding government funds, revenue growth is expected to fluctuate at a low level in March, while expenditure growth is expected to decline. On the revenue side, although real estate investment growth rebounded somewhat in January and February due to base effect, the overall real estate cycle remains weak. Land transfer revenue is expected to continue its pattern of "total volume shrinking, structural differentiation, and weak recovery," making it difficult to change the low-level trend. On the expenditure side, affected by the pressure of maturing local government debt, the pace of new special-purpose bond issuance slowed down in March, and expenditure growth is also expected to decline.

IV. International Capital Flows

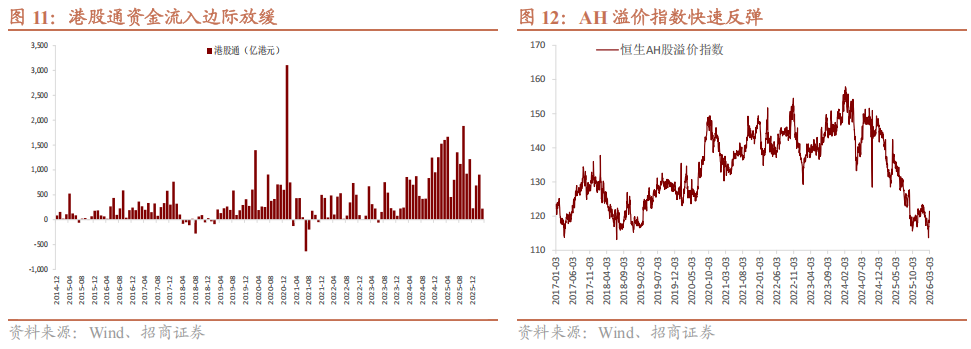

Looking back at February, net inflows of funds into Hong Kong stocks continued, while outflows from the bond market narrowed significantly. The RMB continued to appreciate in February, rapidly rising from around 6.95 at the beginning of the month to around 6.85 at the end. With the central bank maintaining reasonably ample liquidity, institutional funds drove the yield on my country's 10-year government bonds down rapidly to 1.78% by the end of February. The rapid appreciation of the RMB combined with the decline in government bond yields significantly narrowed the outflow of foreign capital from the bond market. Mixed US economic data, a weak US dollar index fluctuating around 97, and a positive domestic economic policy stance all contributed to net inflows into Hong Kong stocks.

Looking ahead to March, geopolitical and oil price shocks overseas have delayed expectations of a Federal Reserve rate cut. Under external pressure, capital inflows into Hong Kong stocks are expected to narrow, while the bond market is expected to continue experiencing net outflows. Due to the sharp rise in international crude oil prices and the unexpectedly slow pace of US non-farm payroll data, the Federal Reserve faces a dilemma. Overseas markets are postponing expectations for a Fed rate cut until the end of the year, or even only one rate cut window in Q4. The US Treasury yield curve is rising, driving the US dollar index higher than 99. The RMB exchange rate has slightly retreated to fluctuate around 6.89. Factors such as imported inflation expectations have driven the 10-year Treasury yield to rise from a low of 1.78% at the beginning of the month to around 1.82%. Under the disturbance of overseas pressure, capital inflows into Hong Kong stocks are expected to slow marginally to HK$61.4 billion, while the bond market is expected to maintain net outflows.

This article is sourced from:China Merchants Bank Macroeconomic Reflections