Author:Wall Street CN

Wall Street's consensus is once again severely out of sync with reality.

According to the latest channel research from Morgan Stanley, the demand and pricing of the hard disk drive (HDD) market are experiencing unprecedented strengthening, and the supply shortage is expected to continue into calendar year 2028 (CY28).

Based on this, Morgan Stanley reiterated its overweight rating on Seagate (STX) and Western Digital (WDC), and upgraded Seagate to "Top Pick," replacing Western Digital. Morgan Stanley significantly raised its price target for Seagate from $468 to $582 (up to $796 in a bullish scenario), and its price target for Western Digital from $369 to $380 (up to $519 in a bullish scenario).

The market currently significantly underestimates the leverage effect of the HDD duopoly in AI and cloud data center spending. Morgan Stanley points out that these two stocks are currently trading at only 13-14 times their projected 2027 calendar year (CY27) earnings per share (EPS), while Morgan Stanley's CY27/28 EPS forecasts are 25%-50% higher than the Wall Street consensus, and gross margin forecasts are 400-500 basis points (up to 700 basis points) higher than the consensus. With the accelerated cost reduction of high-capacity technologies such as HAMR and far-than-expected pricing power, Seagate and Western Digital are entering a golden window of opportunity to reach the mid-to-high 50% gross margin range. Tactically, given Seagate's current valuation discount and faster gross margin expansion, Morgan Stanley recommends investors switch their preferred stock to Seagate.

A “stronger, longer” HDD cycle: Supply and demand imbalance will continue until 2029.

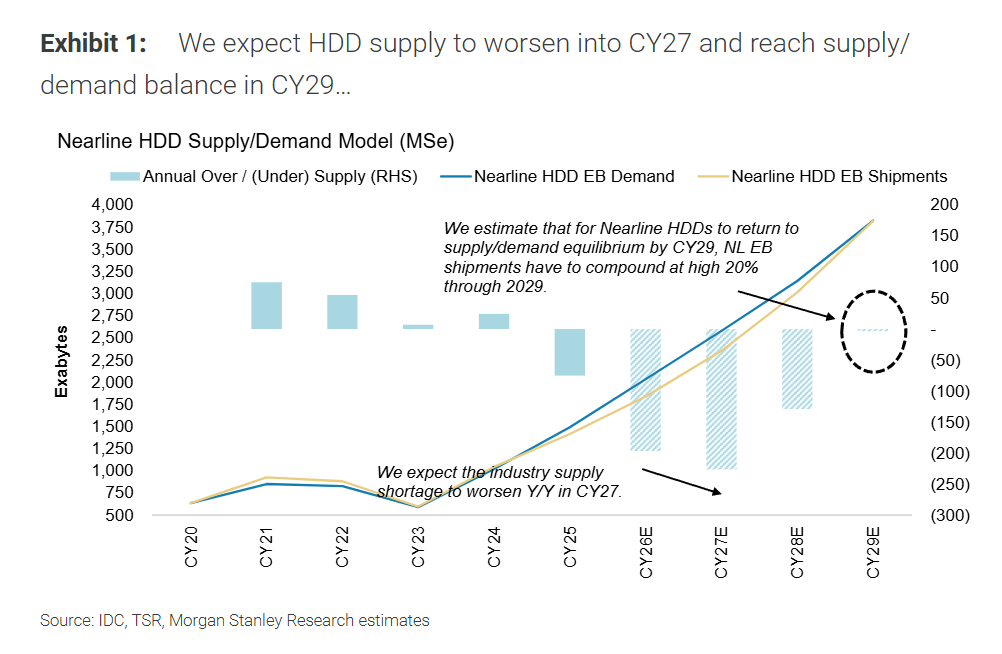

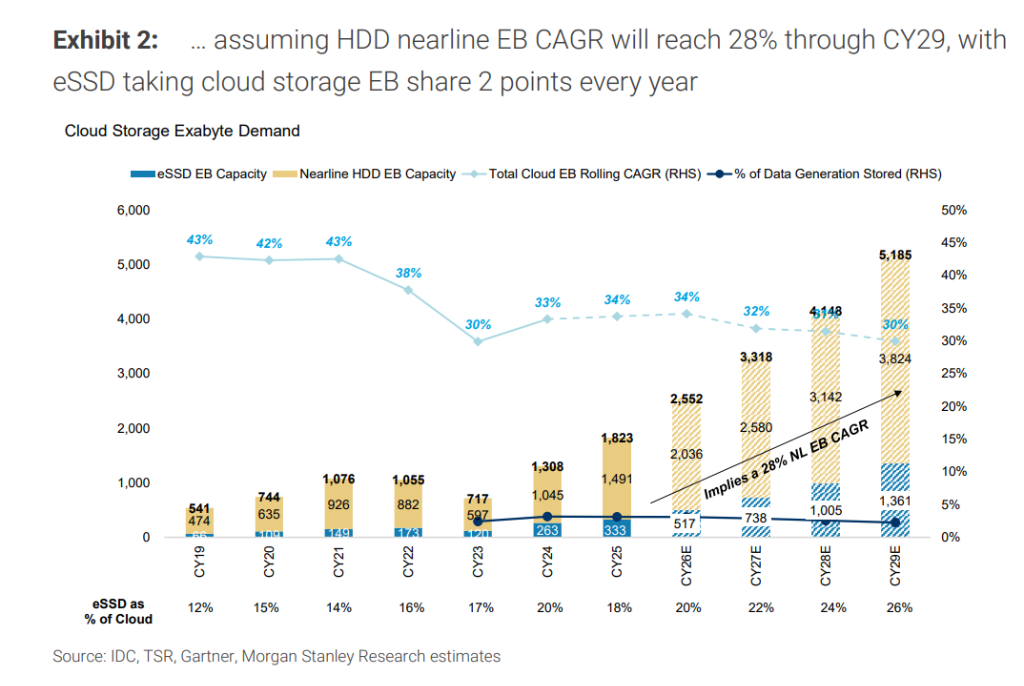

Morgan Stanley's "Stronger for Longer" logic has not only remained unchanged, but is actually being strengthened. Research shows that although the HDD industry's unit output will see an unexpectedly low to mid-single-digit (LSD-MSD%) growth, the industry's exabyte (EB) shortage will still reach 200 EB (accounting for 10% of the market) in CY26 and will approach 250 EB in CY27.

This strong demand stems from the continued migration of workloads to the cloud and the widespread adoption of AI (which has accelerated data generation).

Currently, HDDs still store approximately 80% of global cloud data. Under conservative assumptions (30% annual growth in cloud EB demand, eSSDs capturing 2 percentage points of market share annually, and HDD suppliers refraining from adding any new greenfield capacity), Morgan Stanley predicts that HDD supply and demand will not reach equilibrium until calendar year 2029 (CY29), which is 12 months later than previously expected.

Pricing power and cost reduction go hand in hand: Gross margin will far exceed Wall Street expectations

This is the most disruptive finding in Morgan Stanley's model: HDD vendors are negotiating purchase orders with major hyperscale cloud customers for 2027/2028 at prices close to $20/TB (or $0.02/GB). This price is more than 30% higher than Morgan Stanley's current benchmark assumption of $13-15/TB, and even nearly 20% higher than its bullish pricing assumption.

On the cost side, as both suppliers begin shifting to 40TB+ high-capacity drives in C2H26, the cost per EB will accelerate its decline over the next six quarters. This widening gap between price and cost per GB will drive Seagate and Western Digital's gross margins to the mid-to-high 50% range by the start of CY27. Morgan Stanley's latest gross margin forecast is 400-500 basis points higher than the Wall Street consensus ahead of CY27.

Tactical portfolio adjustment: Why switch the top pick from Western Digital to Seagate?

While Morgan Stanley remains extremely bullish on Western Digital, it has shifted its recent relative preference and "top pick" to Seagate for the following four key reasons:

-

Catalyst fulfillmentThe key catalysts that previously made us optimistic about Western Digital (narrowing the valuation gap with Seagate and deleveraging by using SNDK shares) were realized last quarter.

-

Valuation discountSeagate's current price-to-earnings ratio (P/E) is more than half that of Western Digital, while Morgan Stanley believes that the two should be valued at the same level.

-

Gross margin expansion is fasterBottom-up cost per TB analysis suggests that Seagate's gross margin should expand slightly faster than Western Digital's (about 50 basis points faster) over the next 12 months, thanks to a strong HAMR product portfolio transition.

-

EPS and target price have greater upside potential.Morgan Stanley sees greater upside potential in its EPS forecasts and target price for Seagate over the next 12 months. Furthermore, Seagate is expected to repay its convertible bonds earlier, thereby reducing equity dilution.

The severely undervalued core assets of AI data centers

Morgan Stanley believes this is an extended cycle (meaning 2027 is not the peak), and therefore maintains its base target P/E ratio of 18x for Seagate and Western Digital.

Among the Russell 3000 index companies (with a market capitalization greater than $5 billion), only about 20 companies are projected to have an annual EPS growth rate exceeding 40% and a gross margin exceeding 45% by 2028, with Seagate and Western Digital among them. If we further filter out companies with a free cash flow (FCF) margin exceeding 30% and returning more than 75% of their FCF to shareholders, only Seagate and Western Digital remain.

Compared to the memory market, the HDD market has a more favorable structure: only three players (the top two control 90% of the market), no Chinese competitors, data center revenue exposure exceeding 80%, and no new greenfield capacity. In 2026, Seagate and Western Digital's total capital expenditure (Capex) is close to approximately $1 billion, far lower than the over $90 billion expenditure of the world's top five memory players.

~~~~~~~~~~~~~~~~~~~~~~~~

The above exciting content comes from

For more detailed analysis, including real-time updates and firsthand research, please join [the group/group].