Author:Wall Street CN

Persistently high oil prices are pushing the global economy toward a troubling macroeconomic landscape: slowing growth and persistent inflation coexisting. Morgan Stanley warns that the real risk lies not in a single sharp shock to oil prices, but in the profound impact of prolonged high oil prices that fail to fall.

According to the TrendFocus trading platform, a research team led by Morgan Stanley's chief global economist Seth B. Carpenter pointed out in a recent report that even if the geopolitical tensions surrounding the Strait of Hormuz do not escalate further, they may continue to impose some restrictions on crude oil supply for a considerable period of time, causing oil prices to continue to bear a geopolitical premium.

In this scenario, the global economy will not face a short-term price shock, but a prolonged rise in energy costs—its macroeconomic impact will be far more complex than any oil price shock in history, and will exhibit clear characteristics of stagflation.

This round of shocks is stagflationary, leading to a significant divergence between monetary and fiscal policies and drastically different impacts on various economies. For investors, this means that expectations of interest rate cuts need to be repriced, and the differences in policy paths among countries will become a key variable in asset allocation.

Inflation risks are underestimated: the second-order effects are more persistent than in history.

Morgan Stanley points out that the fundamental difference between this round of oil price shocks and previous ones lies in the "sustainability" of prices rather than their "peak." In past oil price shocks, prices often fell rapidly after rising, thus naturally compressing the duration of inflation transmission.

However, if oil prices remain high for an extended period and fail to revert to the mean, companies will face a protracted cost shock. Their ability to absorb costs by compressing profit margins will gradually be exhausted, and they will eventually have to pass on the pressure to the price side.

This means that even if the year-on-year increase in energy prices mathematically narrows over time, the secondary effect—the transmission of energy costs to the prices of a wider range of goods and services—will be more persistent than historical experience has shown. Therefore, even if overall inflation data appears to have improved, the risks to inflation remain tilted to the upside.

At the same time, while growth is slowing, it will not collapse. Persistently high energy costs are equivalent to a hidden tax on consumption and corporate profit margins, dragging down economic activity in both developed and emerging markets. This drag will take time to fully materialize, but its impact cannot be ignored.This scenario would lead to a global recession, where the anti-inflationary shock from slowing growth would be insufficient to offset the upward force of secondary effects—thus forming a stagflation pattern.

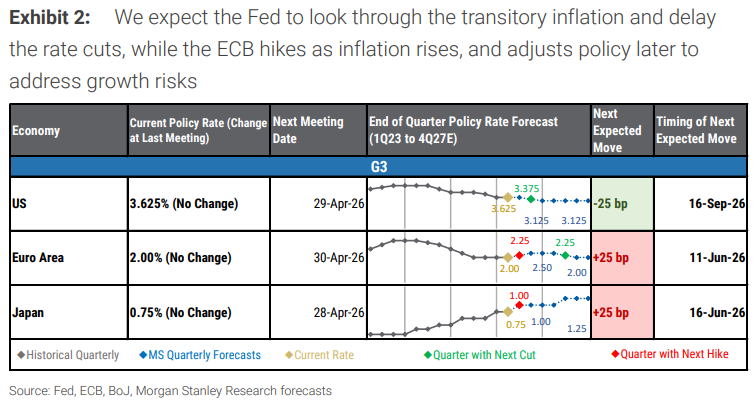

Central bank policies diverge: the Federal Reserve holds rates steady, while the European Central Bank leans towards raising rates.

Faced with stagflationary pressures, major central banks have shown significant divergence in their policy orientations, which will be a key variable affecting the global interest rate market.

Central banks that are more sensitive to inflation expectations—especially the European Central Bank and the Bank of England—are inclined to tighten policy further in the current environment.According to its latest forecast, the European Central Bank's next move is to raise interest rates by 25 basis points, with the timing expected in June 2026; the Bank of Japan also expects to raise interest rates by 25 basis points in June 2026.

In contrast, the Federal Reserve's situation is more complex. The Fed will choose to pause rather than cut interest rates, and this pause could last for a considerable period.Its baseline forecast indicates that the next 25-basis-point rate cut by the Federal Reserve will occur in September 2026, provided that inflation expectations do not shift significantly. If inflation expectations show signs of rising, the Fed may even maintain its restrictive policy stance until 2027.

Emerging market central banks' responses are more fragmented, highly dependent on each country's fiscal situation and external vulnerabilities, making it difficult to form a unified policy direction.

Fiscal Policy: Energy Subsidies – A Double-Edged Sword that Exacerbates Global Divergence

At the fiscal policy level, the responses of governments around the world will profoundly affect inflation trends and further exacerbate the divergence in the global macroeconomic landscape.

Many governments are inclined to adopt broad price-suppressing measures, including cutting fuel taxes, setting price caps, or implementing universal subsidies, shifting the cost burden from households to public or quasi-public balance sheets. While such measures may provide a short-term buffer, they can distort price signals, support demand, and potentially keep inflation high for extended periods—especially when these measures are constrained by fiscal space and difficult to sustain.

For energy-importing emerging markets with limited fiscal space, widespread subsidies could damage external account balances and policy credibility; while energy-exporting countries benefit from improved terms of trade, with some even gaining additional fiscal revenue. This divergence is the underlying reason for the highly differentiated and difficult-to-coordinate policies of emerging market central banks.

In contrast, countries that adopt more targeted support measures—focusing on vulnerable households or specific sectors while allowing for more full energy price transmission—face greater pressure on consumers in the short term, but at the cost of lower fiscal costs and more manageable inflationary shocks, at the expense of greater downside risks to growth. Given current high debt levels, rising financing costs, and renewed tightening of fiscal rules, the likelihood of large-scale fiscal intervention is limited unless the risk of recession increases significantly.

~~~~~~~~~~~~~~~~~~~~~~~~

The above exciting content comes from

For more detailed analysis, including real-time updates and firsthand research, please join [the group/group].