Author:Wall Street CN

Asian and European refiners are fiercely competing for alternatives to Middle Eastern crude supplies, pushing the premium for West Texas Intermediate (WTI) crude to a record high.

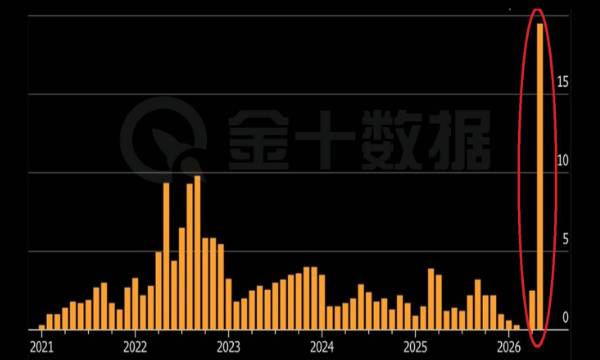

According to media reports on Tuesday, the Strait of Hormuz is effectively closed, severely disrupting the flow of oil from the Middle East.Against this backdrop, the spot premium for WTI crude oil delivery in July has jumped to the range of $30 to $40 per barrel, a significant increase from the premium of about $20 at the end of March.

In a report dated April 3, Rystad Energy's chief oil analyst, Paola Rodriguez-Masiu, noted that "Asian refiners, shut out of Middle Eastern supplies, are aggressively bidding for every barrel of available crude oil in the Atlantic Basin."

The sharp rise in premiums is significantly increasing the costs for refiners in Asia and Europe, causing their losses to continue to widen. Some US state-owned enterprises are under particularly severe pressure due to their government-mandated fuel supply obligations.One trader said, "There are new prices every day," while another said it might be more cost-effective for refiners to reduce crude oil processing and instead buy refined products—provided there are still people willing to sell in the market.

WTI premium hits record high, surpassing Brent in a rare occurrence.

According to media reports citing multiple traders, WTI crude oil for July delivery to North Asia is priced at a premium of approximately $34 per barrel to the Dubai benchmark and a premium of approximately $30 per barrel to the spot Brent crude, while the ICE Brent benchmark price for August delivery is approaching $40 per barrel.

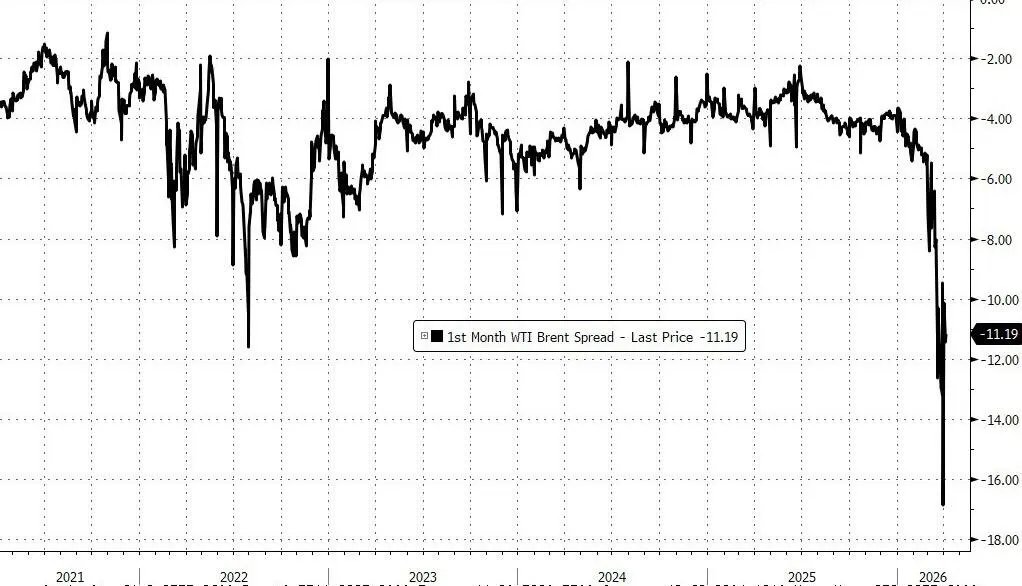

This premium level propelled WTI crude oil futures prices to surpass Brent crude oil futures prices over the weekend, a rare occurrence. Typically, Brent crude, as the pricing benchmark for seaborne crude, tends to lead the market during global supply shocks, while WTI has long traded at a discount.

It is worth noting that this price inversion is partly due to technical factors—the WTI near-month contract corresponds to May delivery, while Brent has rolled over to the June contract, causing a distortion in the apparent price difference.But the deeper driving force lies in the extreme tension in the spot market: the near-month and far-month spreads of WTI futures have risen to record highs, reflecting the market’s urgent need for safe barrels of crude oil that can be delivered immediately.

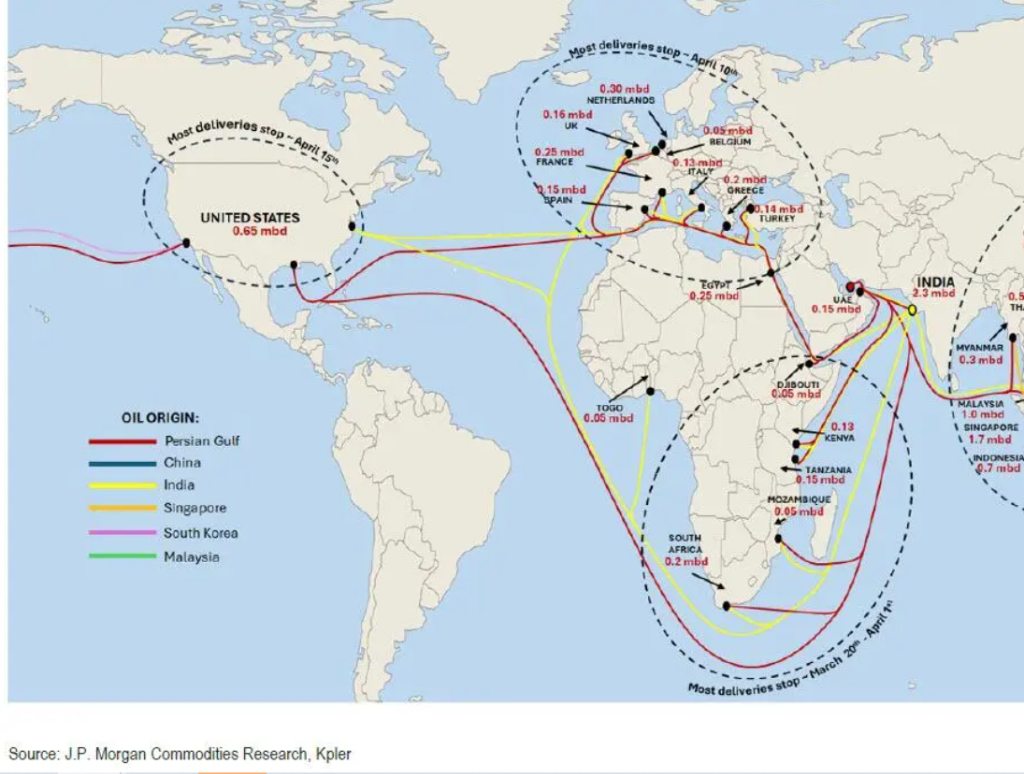

Supply disruptions in the Middle East have made Atlantic Basin crude oil a focal point of contention.

The de facto closure of the Strait of Hormuz has prevented the normal export of large quantities of crude oil from the Middle East, prompting Gulf oil-producing countries to correspondingly reduce upstream production, further tightening global supply. Europe is typically the largest importer of US crude oil, but the strong entry of Asian buyers has disrupted the existing supply and demand dynamics.

Asian refiners are now expanding their sourcing to the Americas, Africa, and even Europe in search of alternative supplies.Japanese refiner Taiyo Oil and other companies completed their WTI crude oil purchases at a premium of approximately $20 per barrel in late March and early April. The subsequent surge in the premium means that subsequent purchase costs will be significantly higher.

With increasing uncertainty surrounding global shipping routes, WTI crude oil has effectively acquired a "safety premium," and its traditional discount relative to Brent has not only narrowed significantly but has even reversed. Analysts point out that the current price inversion indicates a structural failure in the normal pricing signals linked to physical logistics.

Refiners are under pressure, with state-owned enterprises bearing the brunt.

Record-high crude oil premiums are eroding refining profits across the board. Media reports indicate that losses for refiners in both Asia and Europe are widening, with some companies facing severe operational pressure.

State-owned oil refineries are in a particularly difficult position—on the one hand, they must fulfill their government-mandated fuel supply obligations, while on the other hand, they have to bear the high cost of crude oil procurement. Some traders suggest that at the current premium level, reducing crude oil processing and instead purchasing refined oil products would be more economically reasonable, but the supply of refined oil products is also becoming increasingly tight.

The backwardation of WTI futures contracts for the near month has risen to a record high, further confirming the market's extreme thirst for readily deliverable crude oil. This signal means to investors that the tight supply situation in the crude oil spot market is unlikely to ease quickly in the short term, and the risk of price volatility will remain high.