Author:Wall Street CN

The Middle East conflict is evolving from theoretical discussions of geopolitical risks into tangible economic consequences. In its latest strategic research report, JPMorgan Chase warns that Iran is employing a "protracted war" rather than a "firepower showdown" as its core strategy, attempting to achieve its goal of survival by wearing down the will of the US and Israel. The impact of this conflict on global energy markets and the macroeconomy may be far more profound than currently anticipated by the market.

According to the Trends Trading Platform, in a report released by JPMorgan Chase on April 6, the Islamic Revolutionary Guard Corps (IRGC) continues to strengthen its position in the conflict, the possibility of regime change is almost zero, and Iran has also clearly rejected a unilateral ceasefire and put forward specific economic conditions for a ceasefire.

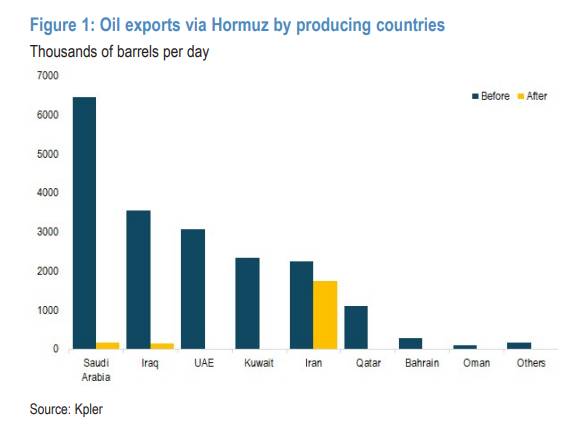

Meanwhile, the blockade of the Strait of Hormuz has caused daily crude oil flows to plummet from the normal level of 15 to 20 million barrels to less than 2 million barrels, and the supply gap is expected to reach 13 million barrels per day this month.

The shock is spreading westward along the supply chain. Asia is the first region to suffer from physical shortages, with refinery shutdowns, flight reductions, and state of emergency declarations already occurring in Bangladesh, Sri Lanka, Pakistan, Indonesia, and the Philippines. If OECD inventory releases remain confined to individual countries, demand losses in Southeast Asia could exceed 2 million barrels per day in May and approach 3 million barrels per day in June.

Iran's strategy: Survival is victory; a "protracted war" is superior to a "cold peace."

Iran views a protracted hot war as a more acceptable option than a "cold peace" that lingers under sanctions. For the IRGC, survival itself is tantamount to victory.

The report points out that the IRGC is well aware that its military strength is inferior to that of the US-Israel coalition, but believes that it can wear down its opponent through horizontal escalation—spreading the pain to the regional and global economy, depleting the opponent's interceptor munitions stockpile, and continuously exerting pressure through drones and the Strait of Hormuz.The US and Israel may win every exchange of fire, but they could still lose control of the course of the conflict.

The report also noted that the Iranian regime judged Trump to lack the political will for a protracted war, and Israel faced constraints due to limited ammunition supplies. Trump's national address on April 1 was described as a "continuation rather than an escalation," and the US-Israeli bombing campaign remained within the initially set window of four to six weeks. However, US military planners have nearly exhausted their target pool, and risks to the global energy market are rising.

If the United States decides to send ground troops to Iranian territory, it will significantly increase the motivation for all parties to escalate the conflict, including laying mines to block the strait, attacking regional infrastructure, and even activating the Houthi rebels to close the Bab el-Mandeb Strait.

With the IRGC gaining power and regime change becoming impossible, ceasefire negotiations have stalled.

The report explicitly refutes any expectations of regime change. The Supreme Leader is no longer at the top of the power structure; in fact, the IRGC has become increasingly powerful due to the conflict. There is no organized alternative political force within Iran, and forcibly pushing for regime change is more likely to lead to national failure than a stable transition.

The military strikes ignited strong Iranian nationalist sentiment, with nighttime protests chanting slogans such as "No surrender, no compromise, fight the US to the end." The IRGC's identity is rooted in defending revolutionary independence and refusing to be "conquered," a stance deeply shaped during the Iran-Iraq War of 1980-1988 and continuing to this day.

There are currently no ceasefire negotiations underway. Iran refuses to negotiate "at gunpoint," and any serious ceasefire efforts must cover deterrence, sanctions, sovereignty, and nuclear issues, and cannot be unilaterally led by the United States or Israel.

Iranian Foreign Minister Abbas Araghchi stated that 1,000 pounds of 60% enriched uranium remain "under the rubble" and their whereabouts are unknown, further pushing Iran to conclude that nuclear weapons are the only reliable shield.

Hormuz: A strategic bargaining chip rather than a tool for retaliation; the road to reopening is long.

The Strait of Hormuz is central to Iran's deterrence strategy. Under normal circumstances, approximately 15 to 20 million barrels of crude oil pass through the strait daily, accounting for about 20% of global oil supply and 38% of global seaborne crude oil trade. It is also a key passage for LNG, LPG, and petrochemical products.

The report points out that Iran's attack on Qatar's Ras Laffan liquefied natural gas facility damaged 17% of its production capacity, marking a shift in Iran's strike pattern from "symbolic retaliation" to "strategic sabotage."

Iran currently allows selective passage for tankers from some friendly countries, but this framework has not restored meaningful flow and effectively acknowledges Iran's substantial control over the world's core energy arteries.

Maintaining the strait's closure is far easier than fully restoring confidence in passage—even just one or two drone attacks per day would be enough to keep it closed. If the strait cannot reopen by early May, OECD business inventories could fall to their lowest operational levels.Even if a ceasefire is reached, shipping companies, insurers, port operators, and seafarers will need to rebuild confidence. The most optimistic estimate is that it will take two months to resume port operations and four months to fully restore oil production and flow.If the blockade lasts for more than six months, there is a risk of structural damage to reservoirs and oil fields.

The energy shock is comparable to COVID-19, and the upside risk to oil prices is underestimated.

This energy shock can be compared to the COVID-19 pandemic, and its non-linear impact on economic activity is considered far greater than the energy crisis triggered by the 2022 Russia-Ukraine conflict. Unlike 2022, a blockade of the Strait of Hormuz could lead to a physical shortage of physical energy supplies, as Asia imports more than 50% of its crude oil and over a third of its natural gas through the strait.

If energy prices remain around $100 per barrel until mid-year (and then fall back to $80 per barrel), it will push up consumer prices by about 0.8 percentage points and drag down global GDP by about 0.6 percentage points. However, if flow remains blocked until mid-May, the risk of oil prices being squeezed to the $120-$130 per barrel range is rising, and prices above $150 per barrel are not impossible.

Total production cuts this month are expected to reach 13 million barrels per day. With the Hormuz effectively closed, the Red Sea route has become a key alternative route for energy exports; if this route is also disrupted, logistical pressures will be further compounded.

Gulf states are suffering a double blow, Asia is in crisis, and the US faces the erosion of tax cuts due to rising oil prices.

For the Gulf Cooperation Council (GCC) countries, the conflict has caused both physical and economic damage, with an estimated 50 processing plants affected. The report forecasts Qatar's GDP will shrink by 9% in 2026, a 14 percentage point downward revision from its forecast about a month ago; Kuwait's GDP forecast has been revised down to -7.1%. The GCC region is expected to experience a significant contraction in the first half of 2026, with port data showing that trade activities in Qatar and Bahrain have been most severely impacted.

In Asia, Bangladesh, Sri Lanka, Pakistan, Indonesia, and the Philippines have already experienced physical shortages, refinery shutdowns, flight reductions, and declarations of emergency. Africa will begin to feel the impact in early April, and Europe is expected to be affected by mid-April, but Europe will primarily face rising costs and supply competition from Asia, rather than physical shortages.

The United States is at the end of the shock chain, and thanks to its longer shipping times and large domestic production, it is unlikely to experience a physical shortage in the short term. However, the impact will be transmitted through prices, especially in California's refined petroleum product market. Currently, U.S. retail gasoline prices are approaching $4 per gallon, and if the Strait of Hormuz remains effectively closed until mid-April, gasoline prices are expected to exceed $5 per gallon. If the recent increase in gasoline prices continues throughout the year, it will impact consumer purchasing power by approximately $100 billion, which could offset or even exceed the expected $150-160 billion in personal tax relief from this year's tax cuts.

~~~~~~~~~~~~~~~~~~~~~~~~

The above exciting content comes from

For more detailed analysis, including real-time updates and firsthand research, please join [the group/group].

![When copper prices rise, who is buying, who is pushing up prices, and who is buying on dips? [Peifengke Master Class 3.1]](http://img.528btc.com.cn/pro/2026-04-07/img/1775556730039cc9499b27xjjh6h6ba865524b31x86h8.jpg)